Your fleet is one of your biggest business assets, and protecting it requires the right insurance strategy. Commercial auto insurance in Columbus isn’t just a legal requirement-it’s your financial safeguard against accidents, liability claims, and unexpected vehicle damage.

At Central Ohio Insurance Services, Inc., we’ve helped countless Columbus businesses identify coverage gaps that leave them exposed. This guide walks you through the essential protections your fleet needs and the common mistakes that cost businesses thousands in uncovered losses.

Why Commercial Auto Insurance Protects Your Bottom Line

One accident exposes your finances

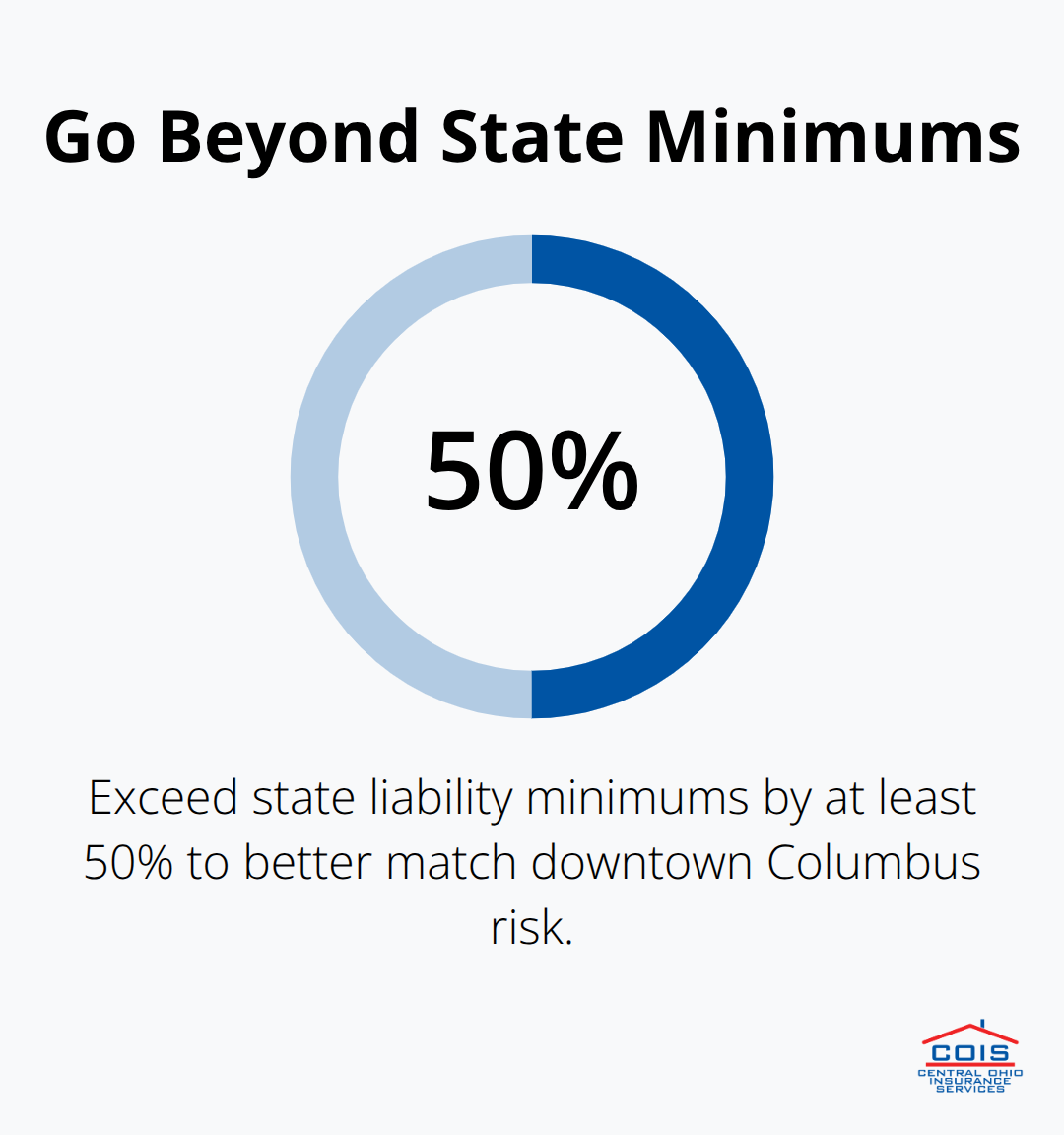

One accident involving a fleet vehicle in Columbus can drain your business finances faster than you’d expect. A single liability claim for bodily injury can easily exceed $100,000, and if your policy limits are too low, your company absorbs the rest. Ohio’s minimum liability requirement is 25/50/25, meaning $25,000 per person for bodily injury, $50,000 per accident for bodily injury, and $25,000 for property damage. That sounds adequate until a serious collision happens and medical bills, lost wages, and legal fees pile up. Progressive, the No. 1 commercial auto insurer according to SNL Financial in Q3 2025, reports that many Columbus businesses operate with state minimums alone-a risky choice that leaves significant exposure. If your fleet carries tools, equipment, or hazardous materials, your actual liability risk is far higher. Exceeding state minimums by at least 50% makes sense, particularly if your vehicles operate in downtown Columbus where traffic density drives up settlement costs.

Vehicle damage and theft hit harder than you think

Fleet vehicles face constant threats on Columbus roads and job sites. A single collision repair for a commercial van runs $8,000 to $15,000, and if you lack collision coverage, that’s an out-of-pocket loss. Theft and weather damage compound the problem-winter storms and urban break-ins are routine in Central Ohio. Collision coverage handles accidents with other vehicles or objects, while comprehensive coverage protects against non-collision losses. Many Columbus contractors skip comprehensive to cut premiums, then lose vehicles to theft or hail damage that costs more than a year of premiums saved. Your fleet’s downtime after a loss directly impacts your ability to serve clients and maintain revenue.

Uninsured drivers create a hidden risk

Uninsured motorist protection is equally critical; an estimated 18.5% of Ohio drivers were uninsured in 2023, meaning your vehicles face collision risk with drivers who cannot pay damages. This coverage protects your vehicles and your medical costs when hit by an uninsured driver-a scenario that happens regularly on I-270 and local routes throughout Columbus. Without this protection, you absorb the full cost of repairs and injuries even though another driver caused the accident. The coverage gap widens when you consider that uninsured drivers often lack assets to recover damages through lawsuits. Your commercial auto policy fills this gap and keeps your operation moving forward after a collision with an uninsured motorist.

Understanding these three layers of risk-liability exposure, physical damage, and uninsured motorist scenarios-shows why commercial auto insurance demands more than state minimums. The next section examines the specific coverage types that address each risk and how to structure them for your fleet’s actual operations.

Types of Commercial Auto Coverage Every Fleet Needs

Liability coverage protects your business from catastrophic claims

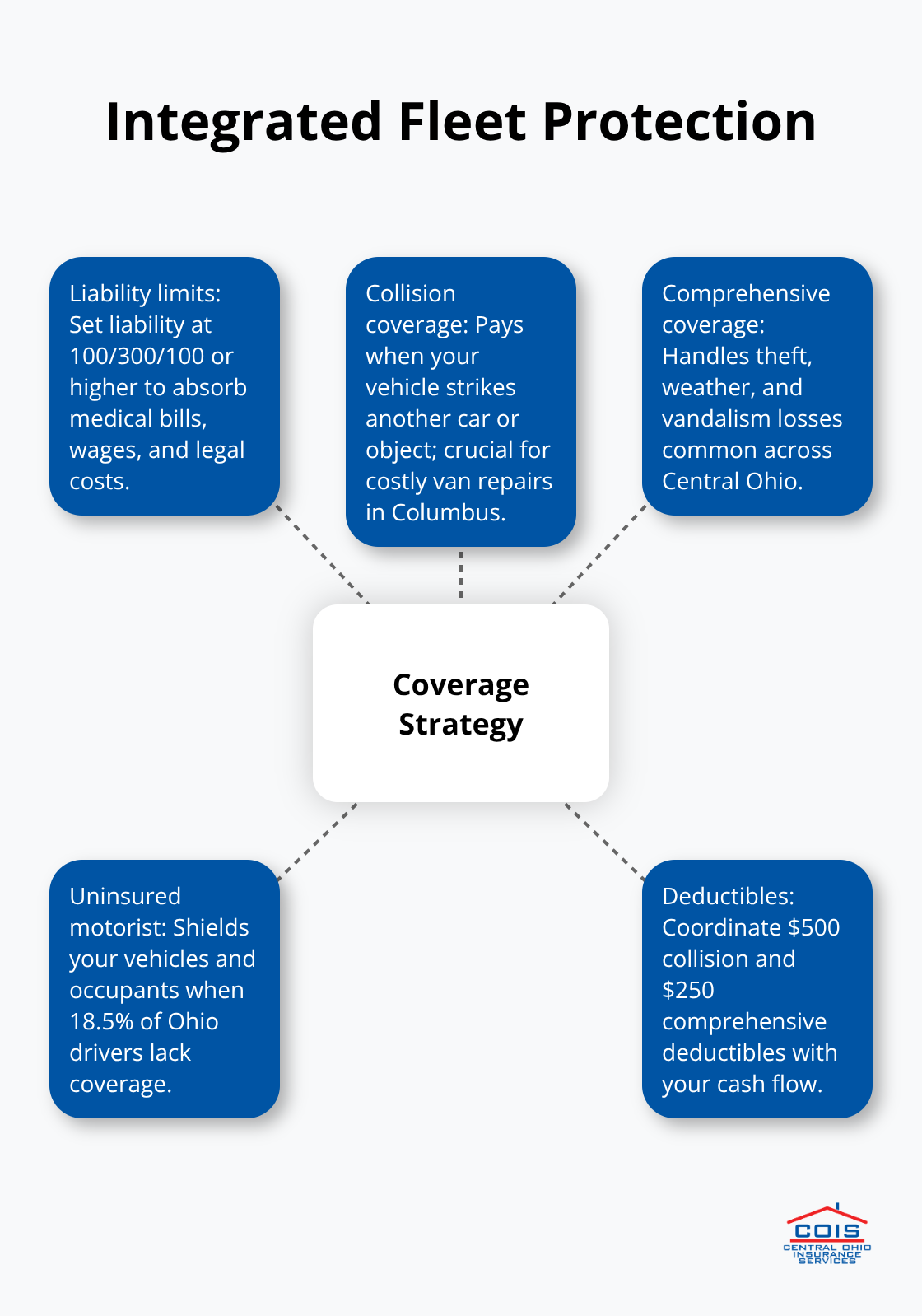

Liability coverage forms the foundation of any commercial auto policy, and it’s where most Columbus businesses get the math wrong. Ohio requires $25,000 for injury/death of one person, $50,000 for injury/death of two or more people, and $25,000 for property damage minimums, but that baseline leaves you exposed the moment a serious accident happens. When one of your drivers hits a pedestrian or another vehicle, your liability coverage pays for their medical bills, lost wages, and property damage up to your policy limit. A single bodily injury claim in Columbus easily reaches $150,000 to $250,000 when you factor in emergency care, ongoing treatment, and legal settlements. Progressive data shows that many Columbus fleets operate with state minimums alone, which means a moderate accident quickly exhausts your coverage and your company absorbs the excess.

We recommend carrying at least $100,000 per person and $300,000 per accident in bodily injury liability, plus $100,000 in property damage coverage. This higher limit costs roughly 15 to 20% more in annual premiums but eliminates the financial cliff that destroys undercapitalized businesses. If your fleet carries tools, equipment, or serves high-density routes downtown, exceed these recommendations further. Your liability exposure grows with vehicle size, driver count, and the nature of your work, so tailor limits to match your actual risk profile rather than settling for the legal minimum.

Collision and comprehensive coverage stop operational downtime

Collision coverage pays for damage when your fleet vehicle hits another vehicle or object, while comprehensive handles non-collision losses like theft, weather damage, and vandalism. A commercial van collision repair runs $8,000 to $15,000 in Columbus, and winter storms routinely damage vehicles across Central Ohio, making comprehensive coverage essential rather than optional. Many contractors skip comprehensive to save $50 to $100 monthly, then lose $12,000 to hail damage or $20,000 to theft, negating years of premium savings.

Your fleet’s downtime after a loss directly impacts your ability to serve clients and maintain revenue. Collision and comprehensive coverage work together to keep your vehicles operational and your business moving forward after physical damage occurs.

Uninsured motorist protection covers gaps liability cannot

Uninsured and underinsured motorist coverage rounds out your protection by covering your vehicles and occupants when hit by drivers who lack adequate insurance or carry no insurance at all. With 18.5% of Ohio drivers uninsured as of 2023, this scenario happens regularly on I-270, Route 23, and local Columbus streets. Without this coverage, you pay for repairs and medical costs out of pocket even though another driver caused the accident. This protection also covers hit-and-run incidents where the at-fault driver vanishes, leaving you with total loss and no recovery path.

Structure these three coverage types together rather than as separate decisions-your liability limits inform the physical damage limits you need, and uninsured motorist protection fills the gaps that liability alone cannot cover. A fleet manager who carries 100/300/100 liability, collision with a $500 deductible, comprehensive with a $250 deductible, and uninsured motorist at 100/300 creates a cohesive defense against the major losses that threaten business continuity. However, even the strongest policy structure fails when coverage gaps go unnoticed, and that’s where many Columbus fleets stumble.

Common Gaps in Commercial Auto Policies and How to Avoid Them

Liability limits don’t match your actual risk

Most Columbus fleet managers discover their coverage gaps only after an accident exposes them, and by then the financial damage is already done. The problem isn’t that your policy is missing coverage entirely-it’s that your liability limits don’t match your actual risk, and you’re carrying vehicles under your policy that shouldn’t be there, or worse, you’re not covering vehicles that should be. A fleet operating with $50,000 per accident liability coverage looks fine until a two-vehicle collision with injuries happens downtown, medical bills reach $180,000, and your company writes a check for $130,000 out of pocket.

Your liability limits should reflect real exposure, including accident severity, driving patterns, contracts, and business assets-not just the average accident. If you operate in downtown Columbus with multiple daily stops, carry tools or equipment worth $5,000 or more per vehicle, or transport clients, your actual liability exposure is far higher than state minimums suggest.

A contractor pickup truck hauling equipment and making frequent stops faces different exposure than a local delivery van, yet many Columbus businesses apply the same liability limits across their entire fleet. Try reviewing your limits against your industry risk profile and your vehicle’s usage patterns to identify where you’re underprotected.

Non-owned and hired vehicles create silent exposure

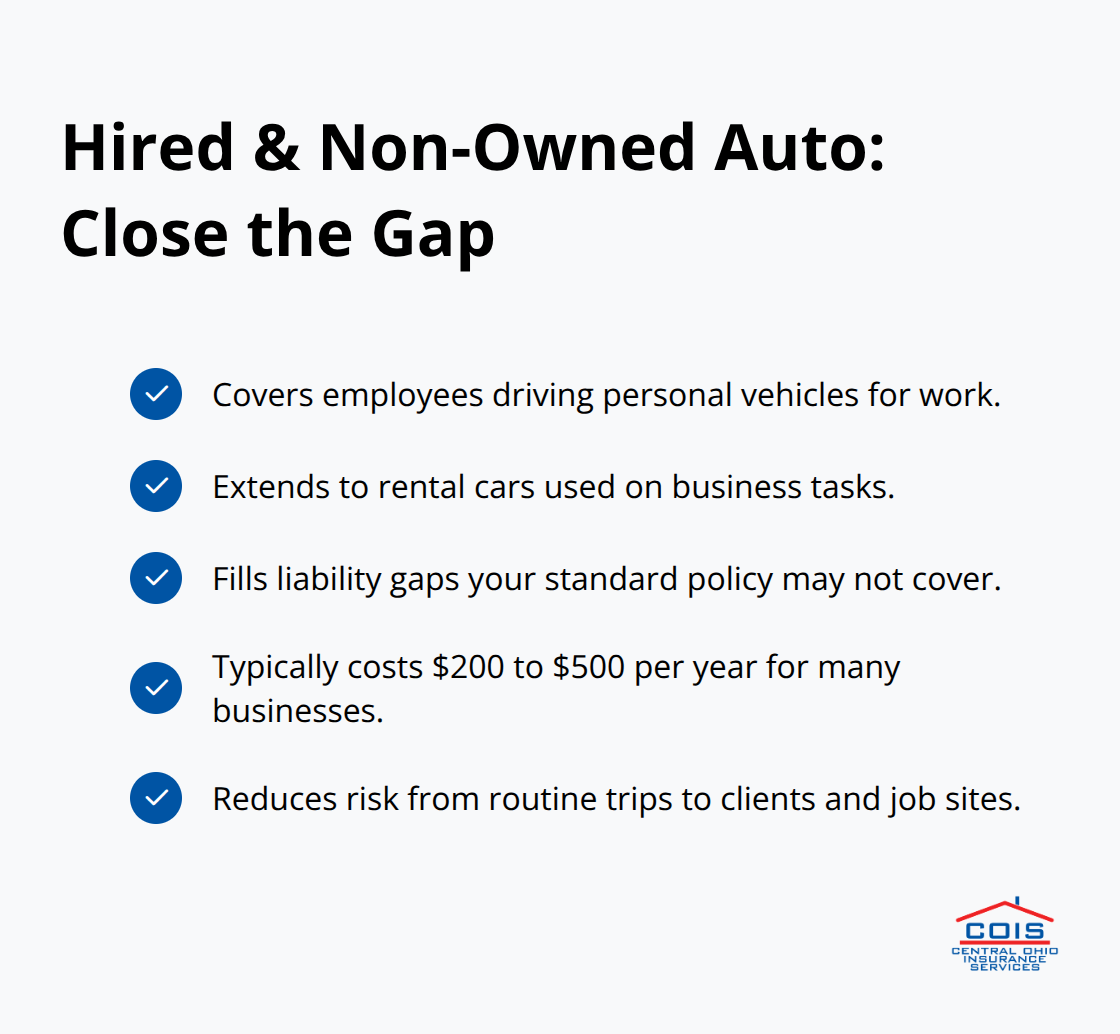

The second major gap appears when you fail to cover non-owned and hired vehicles, which creates a silent exposure that catches most fleet managers off guard. If your employees occasionally rent a vehicle for work tasks or use their personal cars for business purposes, your commercial auto policy likely doesn’t cover those vehicles unless you’ve specifically added Hired and Non-Owned Auto (HNOA) coverage.

A salesman using his personal vehicle to visit a client, an employee renting a truck to haul equipment, or a team member borrowing a company vehicle for a delivery-each scenario creates liability your standard policy may not cover. HNOA coverage typically costs $200 to $500 annually and protects your business when employees use rental cars or personal vehicles for work-related tasks, filling a gap that destroys unprepared businesses.

Without it, a claim involving a personal vehicle used for work can be denied entirely, leaving your company liable for the full damages. Columbus businesses often overlook this coverage because they assume their commercial auto policy automatically covers all work-related driving, but that assumption costs them tens of thousands in uncovered losses. Adding this coverage takes minutes during your policy review and prevents catastrophic exposure that grows every time an employee uses a personal vehicle for work.

Final Thoughts

Your fleet’s protection starts with honest conversations about what your business actually faces on Columbus roads and job sites. The gaps we’ve covered-insufficient liability limits, missing HNOA coverage, and underestimated physical damage exposure-aren’t theoretical problems. They’re financial disasters that happen to Columbus businesses every year, often because coverage decisions were made quickly without matching limits to real operational risk. Pull your current commercial auto insurance Columbus policy and compare your liability limits against your vehicle types, driver count, and daily operating patterns.

If you’re carrying state minimums alone, you’re gambling with your business. Confirm whether your policy covers non-owned and hired vehicles through HNOA coverage, since this gap will cost you far more than the $200 to $500 annual premium if your employees ever use personal vehicles or rentals for work. Review your collision and comprehensive deductibles to ensure they align with your cash flow and risk tolerance-a $1,000 deductible might save premiums but create operational strain after a loss.

At Central Ohio Insurance Services, Inc., we shop multiple carriers to find coverage that matches your fleet’s actual exposure rather than settling for generic policies built around state minimums. Our team reviews your vehicles, drivers, routes, and business operations to identify gaps before they become claims. Contact us today for a free quote and let’s build a commercial auto insurance strategy that guards your operation against the real risks you face.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.