SUVs dominate Columbus roads, but most drivers don’t realize their vehicles need different insurance protection than sedans. Repair costs run higher, liability exposure increases, and Central Ohio’s weather patterns create unique risks that standard policies often miss.

At Central Ohio Insurance Services, Inc., we’ve helped hundreds of local SUV owners find coverage that actually matches their driving needs. This guide shows you exactly what Columbus SUV auto insurance should include and how to avoid paying for protection you don’t need.

Why SUVs Cost More to Insure

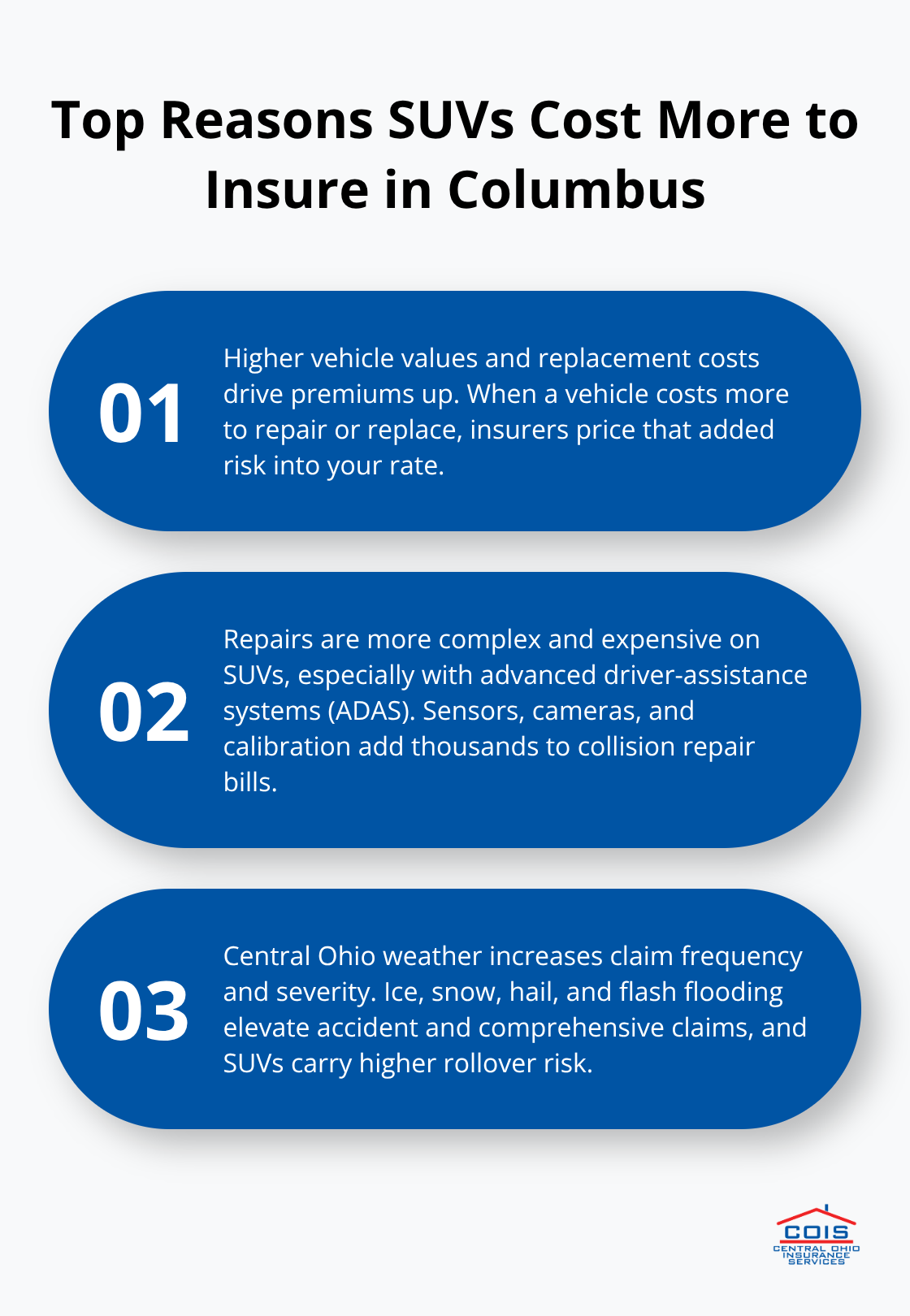

Vehicle Price and Replacement Costs

SUVs carry higher price tags than sedans, and that difference matters directly to your insurance costs. A BMW 330i costs about $2,337 annually for full coverage in Ohio, while a Ford F-150 runs roughly $1,816-but larger or luxury SUVs push those numbers significantly higher. When your vehicle costs more to replace or repair, insurers charge more in premiums because their financial risk increases. Columbus SUV owners frequently overlook this reality until they shop for quotes and discover their three-row Yukon or premium Enclave commands substantially steeper rates than comparable sedans.

Repair Complexity and Advanced Systems

Repair expenses amplify this gap even further. SUVs require specialized parts, longer labor hours for complex repairs, and technician expertise that doesn’t come cheap. A collision that dents a sedan’s bumper might total an SUV’s integrated sensor system or advanced driver-assistance camera array-features like the camera systems in GMC Pro Safety and Buick Driver Confidence packages add thousands to repair bills. Additionally, SUVs tow heavier loads and navigate rougher terrain than sedans, which means collision risk increases in real-world driving patterns around Columbus and Central Ohio. An accident involving towing equipment or off-road use creates liability exposure that standard sedan policies simply don’t account for. Insurers calculate higher premiums because SUV owners statistically file larger claims.

Central Ohio Weather and Road Hazards

Weather compounds these risks dramatically. Central Ohio winters bring ice, snow, and variable road conditions that test vehicle stability and braking performance. SUVs, while offering better traction through AWD and 4WD systems, also carry higher centers of gravity that increase rollover risk during emergency maneuvers on I-270 or I-71. Summer storms and flash flooding present another hazard-comprehensive coverage becomes essential when your vehicle faces hail, wind damage, or water intrusion. Standard policies that work fine for urban sedan commuters leave SUV owners exposed because those policies assume lower weather-related claim frequency than Central Ohio actually experiences.

Understanding these cost drivers helps you recognize why your SUV insurance quote differs from your neighbor’s sedan rate. The next section breaks down which coverage types actually protect your investment and address the specific risks SUV owners face on Central Ohio roads.

What Coverage Do Columbus SUV Owners Actually Need

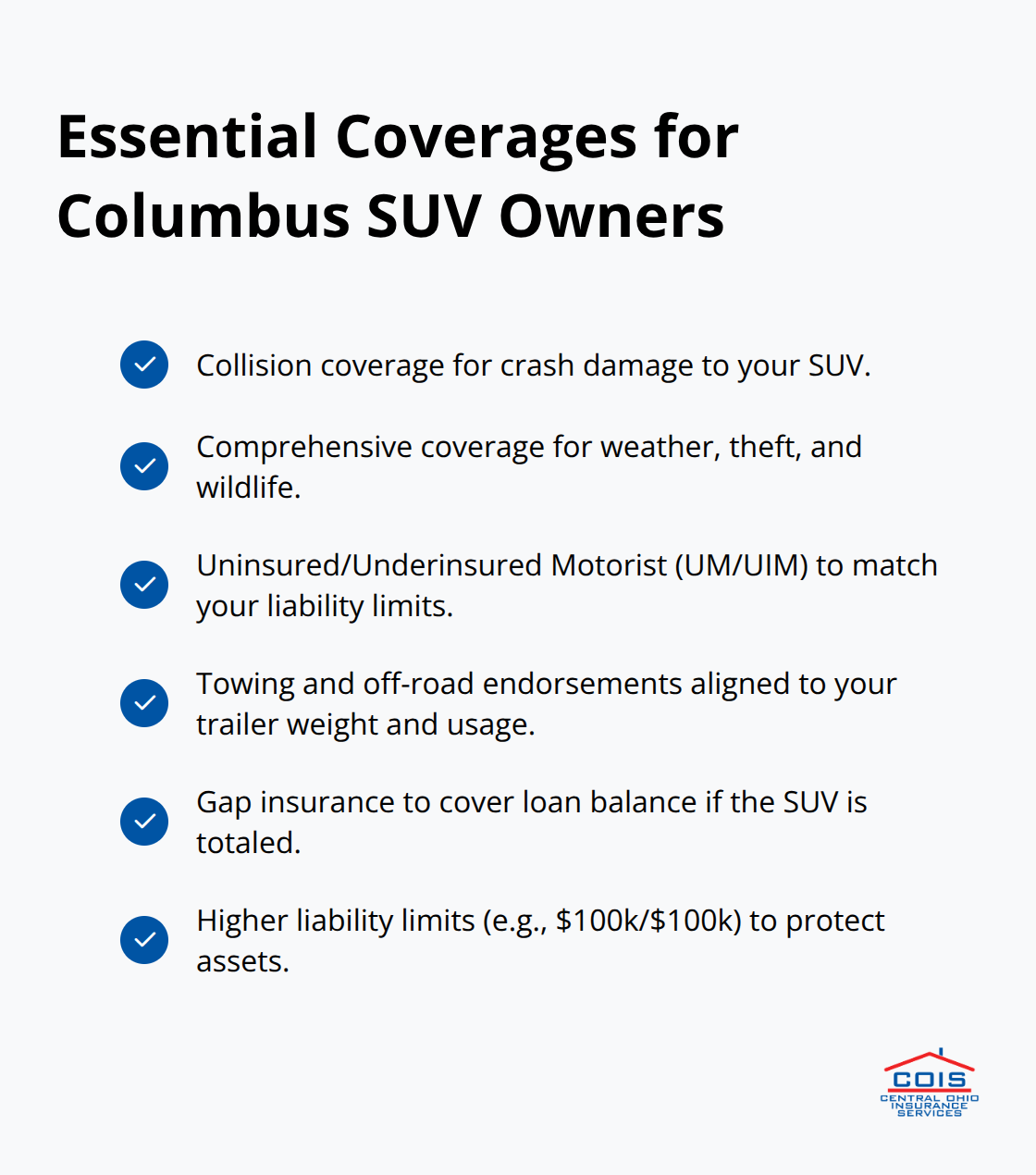

Collision and Comprehensive Protection

Collision and comprehensive coverage form the foundation of any SUV insurance strategy in Columbus, and skipping either one leaves your vehicle dangerously exposed. Collision pays for damage when your SUV hits another vehicle or object-a fender-bender on I-270 or a parking lot accident-while comprehensive covers weather, theft, vandalism, and wildlife strikes. For SUV owners, comprehensive matters more than most drivers realize because Central Ohio’s hail season and winter conditions generate frequent claims. If your SUV is financed, your lender requires both coverages, but even if you own your vehicle outright, the math favors protection. A full-coverage policy in Columbus costs about $2,092 annually according to Bankrate data from November 2025, which breaks down to roughly $174 per month-far less than a single major repair on an SUV with advanced safety systems.

Your deductible choice directly affects your premium, so selecting a $1,000 deductible instead of $500 can cut costs meaningfully, but only if you can actually afford that out-of-pocket amount when a claim happens. Most Columbus SUV owners should stick with $500 or $750 deductibles because the premium savings rarely justify the financial strain of a larger deductible.

Uninsured and Underinsured Motorist Coverage

Uninsured and underinsured motorist coverage deserves serious attention because Ohio’s minimum liability limits-$25,000 per person and $50,000 per accident-fall far short of real-world crash costs. If an uninsured driver hits your SUV and causes $40,000 in injuries, you pay thousands from your own pocket unless you carry UM/UIM coverage. This protection is optional in Ohio, but the reality of SUV ownership makes it essential because your vehicle’s higher value and weight create larger claims when accidents occur. Choose UM/UIM limits that match or exceed your liability coverage-if you carry $100,000 in liability, your UM/UIM should reach $100,000 as well.

Specialized Coverage for Towing and Off-Road Use

For SUV owners who tow trailers, haul equipment, or regularly drive on unpaved roads around Central Ohio, specialized coverage becomes essential. Standard policies often exclude or limit coverage for off-road use, towing accidents, or cargo damage, which means a rollover while towing a boat or trailer leaves you underinsured. Discuss towing limits with your agent before purchasing coverage because a policy that covers 5,000 pounds of towing won’t protect you if you’re pulling an 8,000-pound trailer. Gap insurance also matters for financed SUVs because if your vehicle is totaled, the insurance payout might fall short of what you owe on the loan-gap coverage bridges that difference and prevents you from owing money on a vehicle you no longer own.

Once you understand what coverage types protect your SUV, the next step involves finding the right carrier and quote that actually matches your Columbus driving patterns and vehicle use.

Getting the Right SUV Quote in Columbus

Compare Quotes Across Multiple Carriers

Shopping for SUV insurance in Columbus requires comparing actual quotes across multiple carriers rather than relying on online calculators or assumptions about rates. Start with at least three major insurers-not because you’ll switch companies three times, but because rate differences for the same coverage can exceed $400 annually depending on how each carrier prices SUV risk. One driver’s $2,092 annual full-coverage cost in Columbus might drop to $1,680 with a different insurer using the same vehicle and driving record, according to Bankrate data from November 2025. Request quotes with identical coverage limits and deductibles so you’re comparing apples to apples.

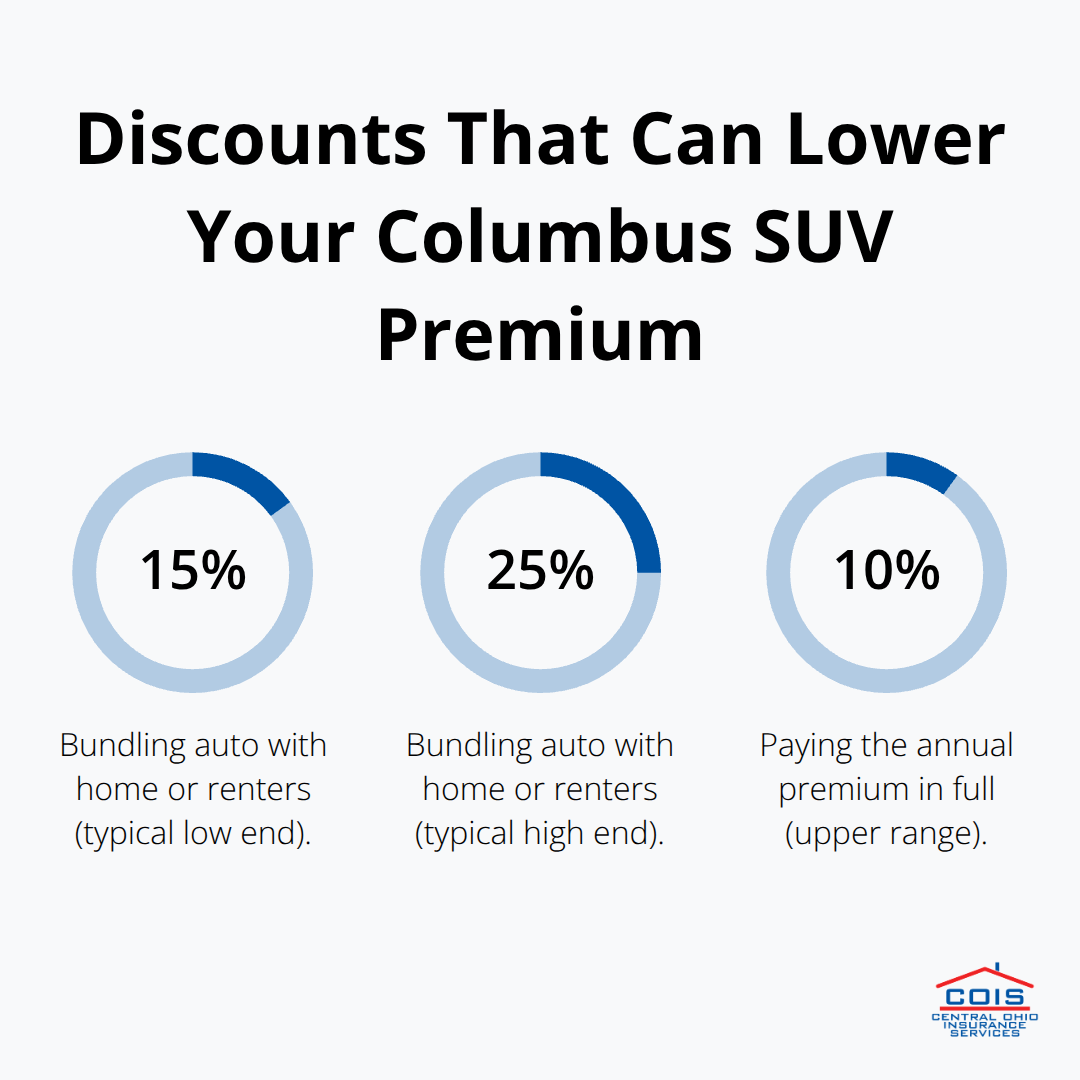

Most insurers offer online quote tools that take 10 minutes, but phone quotes often reveal discounts the website doesn’t mention-things like bundling your auto policy with home or renters coverage, which typically saves 15–25 percent on your premium. Ask specifically about low-mileage discounts if you drive fewer than 10,000 miles annually, safety-feature discounts for your SUV’s advanced driver-assistance systems, and good-driver discounts for accident-free records. Paying your annual premium in full rather than monthly installments often yields 5–10 percent savings that compounds over time.

Select the Right Deductible for Your Situation

Deductible selection directly impacts your monthly cost, and Columbus SUV owners often choose the wrong amount because they don’t understand the tradeoff. A $1,000 deductible might cost $30 less per month than a $500 deductible, but that $360 annual savings evaporates the moment you file a claim and face a larger out-of-pocket expense. Choose a deductible you can actually afford without financial stress-for most Columbus families, that’s $500 or $750.

Determine Adequate Coverage Limits

Coverage limits matter equally because Ohio’s minimum liability of $25,000 per person and $50,000 per accident leaves you dangerously exposed if your SUV causes serious injury. We recommend carrying at least $100,000 in bodily injury coverage and $100,000 in property damage coverage, which typically costs only $15–20 more monthly than state minimums but protects your assets if a lawsuit follows a major accident.

Work with an Independent Agent

An independent agent shopping multiple carriers-rather than a captive agent representing one company-can identify which insurers offer the best rates for your specific SUV model, driving patterns, and Columbus ZIP code. Local independent agencies access carrier networks that direct online shopping can’t replicate, meaning an agent might find a rate you’d never discover alone. Central Ohio Insurance Services, Inc., a local independent agency in Pickerington, shops multiple carriers to deliver competitively priced solutions with fast quotes and clear guidance on coverage options tailored to your SUV and driving needs.

Final Thoughts

Columbus SUV auto insurance that actually protects your investment requires honest assessment of your vehicle’s value, how you use it, and what financial protection you need. If you tow equipment or drive off-road, specialized coverage becomes non-negotiable, and if you finance your vehicle, your lender requires collision and comprehensive anyway. The real question isn’t whether to carry these coverages but how to structure them affordably while addressing Central Ohio’s specific weather risks and repair costs.

Working with a local independent agent transforms this process from frustrating to straightforward because they shop multiple carriers on your behalf and identify discounts you’d miss alone. They understand Columbus ZIP codes, local weather patterns, and how different insurers price SUV risk differently, plus they handle claims support when accidents occur. Central Ohio Insurance Services, Inc. brings this local expertise to your door with fast quotes and clear guidance on coverage tailored to your SUV and driving needs.

Your next step is straightforward: request quotes from at least three carriers or contact a local independent agent who can do that shopping for you. Compare coverage limits and deductibles side by side, ask about bundling discounts, and verify that your chosen policy actually protects your investment. Columbus SUV owners who take this approach typically save money while gaining coverage that actually works when they need it.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.