Your home is likely your largest financial investment, and protecting it should be a top priority. At Central Ohio Insurance Services, Inc., we understand that Pickerington homeowners insurance isn’t just about following lender requirements-it’s about safeguarding your property and your family’s financial future.

The right coverage can mean the difference between recovering quickly from damage and facing significant out-of-pocket costs. This guide walks you through what you need to know to make informed decisions about your home’s protection.

Why Homeowners Insurance Protects Your Pickerington Investment

Weather and Water Threats in Pickerington

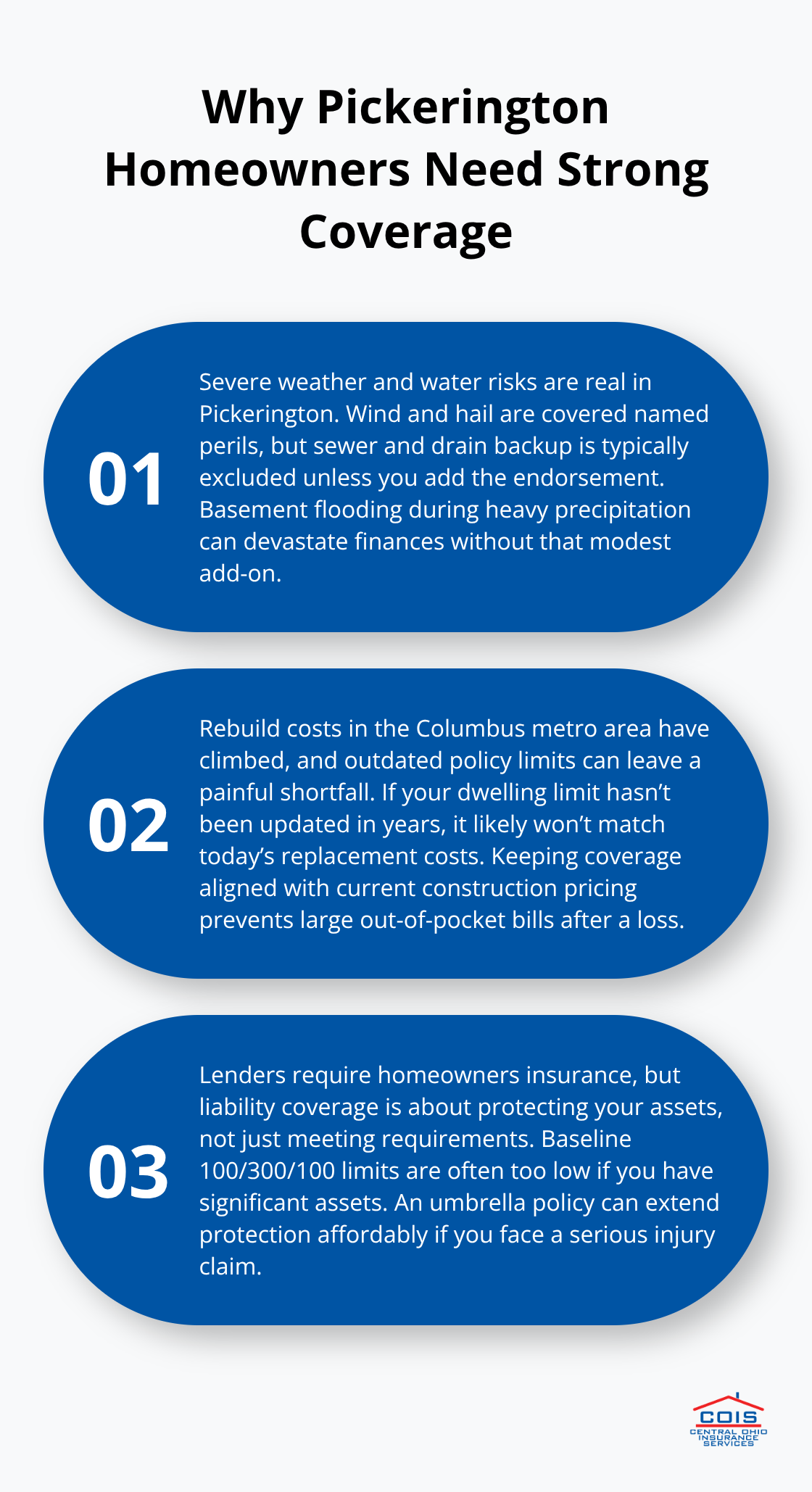

Pickerington experiences the full range of Ohio weather patterns, and that reality shapes your insurance needs. Wind and hail strike the area regularly, and water damage remains a significant homeowner concern according to the Insurance Information Institute. Basement flooding poses a genuine threat during heavy precipitation. A standard homeowners policy covers wind and hail as named perils, but water backup from sewers and drains typically gets excluded-you need to add that endorsement separately. The cost is minimal compared to the financial devastation of a basement flood, which is why we at Central Ohio Insurance Services, Inc. recommend this addition for nearly every Pickerington client.

The Rising Cost of Rebuilding Your Home

Your home represents your largest financial asset, and in the Columbus metro area including Pickerington, dwelling values and rebuild costs have trended upward according to the National Association of Insurance Commissioners. If your policy limits haven’t been updated in several years, they almost certainly fall short of current replacement costs. Construction expenses have risen significantly-a home that cost $250,000 to rebuild five years ago might cost $285,000 today. This gap between your coverage limit and actual rebuild costs leaves you exposed to substantial out-of-pocket expenses after a loss.

Lender Requirements and Liability Protection

Your mortgage lender mandates homeowners insurance, and they take this requirement seriously. Lenders require minimum coverage amounts for the dwelling and liability protection, and failing to maintain adequate coverage can trigger a lender-placed policy that costs substantially more than a policy you shop for yourself. Beyond the legal requirement, liability coverage protects your personal assets in a lawsuit.

The standard starting point of 100/300/100 liability coverage is inadequate if you own significant assets or have high-value property on your lot.

Umbrella Policies Extend Your Protection

An umbrella policy extends liability limits beyond your homeowners policy at a reasonable cost (typically $150 to $300 annually for $1 million in additional coverage). This protection becomes essential if someone is injured on your property and pursues a claim. The difference between being underinsured and properly protected often comes down to one conversation with a local agent who understands Pickerington’s specific risks and can walk through your actual exposure. Understanding what coverage options actually exist for your situation requires a closer look at the types of protection available to you.

What Coverage Actually Protects Your Pickerington Home

Dwelling Coverage Reflects Today’s Rebuild Costs

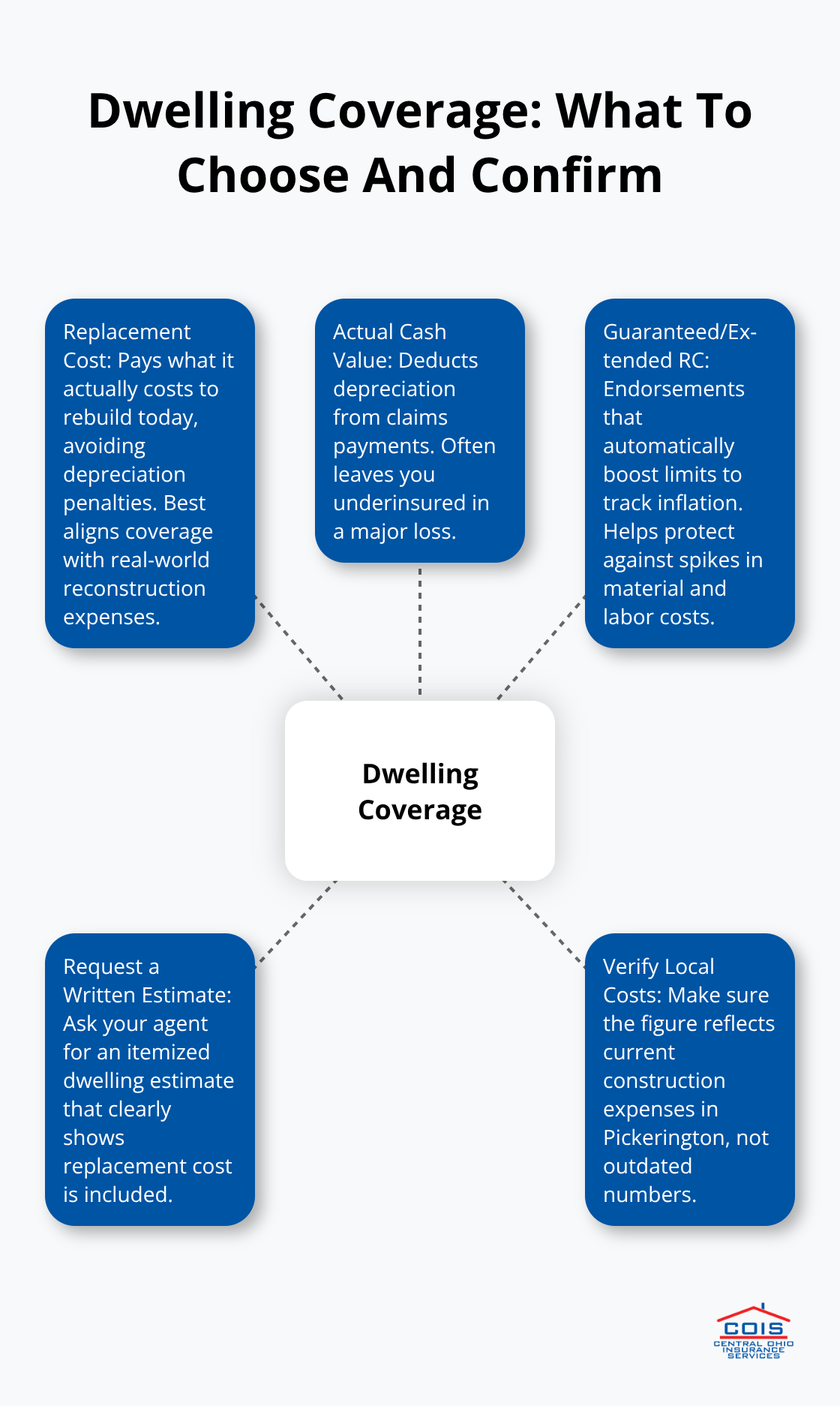

Dwelling coverage forms the foundation of your homeowners policy, and it must reflect what your home would cost to rebuild today, not what you paid for it years ago. Construction costs in the Columbus metro area have risen significantly, with prices remaining 25–40% above 2019 levels depending on the project type. You have two choices: replacement cost coverage, which pays what it actually costs to rebuild, or actual cash value, which deducts depreciation and leaves you severely underinsured. Replacement cost coverage works far better than actual cash value in a real loss scenario because it covers the full expense of reconstruction without penalty.

Many insurers offer guaranteed replacement cost or extended replacement cost endorsements that automatically increase your dwelling limit by a percentage each year, which tracks inflation without requiring you to manually adjust coverage annually. When you request a quote, ask your agent for a detailed written estimate that itemizes dwelling coverage and shows whether it includes replacement cost, and verify the number reflects current construction expenses in Pickerington, not an outdated estimate.

Personal Property and Valuable Items Need Specific Protection

Personal property coverage protects your belongings at replacement cost if you select that option, but standard policies impose sublimits on high-value items like jewelry, art, and collectibles. The Insurance Information Institute recommends scheduling valuable possessions with a personal floater to remove these sublimits and ensure full coverage at current market value. This step takes minimal effort but prevents significant financial loss if theft or damage affects your most prized possessions.

Liability Coverage Requires an Honest Assessment

Liability coverage starting at 100/300/100 protects you from third-party injury claims, but this limit is dangerously low if you own substantial assets. An umbrella policy extends liability protection beyond your homeowners limits for roughly $150 to $300 annually per $1 million in additional coverage, and this genuinely affordable protection shields your home and savings from a lawsuit. Most Pickerington homeowners with significant net worth should carry at least $1 million in umbrella coverage to match their actual financial exposure.

Water Damage Requires Two Separate Protections

Flood insurance deserves special attention because standard homeowners policies exclude flood damage entirely, and the National Flood Insurance Program through FEMA is your primary option in most Pickerington areas. Water backup from sewers and drains is also excluded from standard coverage, so add a backup endorsement immediately-this coverage typically costs under $200 annually and protects against the most common water-related loss homeowners face. These two water-related gaps in standard policies represent the biggest exposure most Pickerington homeowners overlook, yet both are inexpensive to address. Understanding your actual coverage limits and endorsement options sets the stage for the next critical step: comparing quotes from multiple carriers to find the right policy at the right price.

Choosing the Right Homeowners Policy

Start with your home’s actual replacement cost, not its market value or purchase price. The National Association of Insurance Commissioners emphasizes that dwelling coverage must reflect what it costs to rebuild your specific home today using local construction methods and materials. Contact three local contractors in Pickerington and request rough rebuild estimates for your home’s square footage, age, and construction type. These conversations take 15 minutes each and provide concrete numbers rather than relying on outdated estimates from your mortgage paperwork. Once you have contractor estimates, add 10–15% to account for code upgrades and permitting costs that arise during reconstruction. This number becomes your target dwelling coverage limit. Many homeowners undershoot by 20–30% because they anchor to their home’s purchase price rather than current replacement costs, which leaves them dangerously exposed if a total loss occurs.

Getting Quotes from Multiple Carriers Reveals Real Price Differences

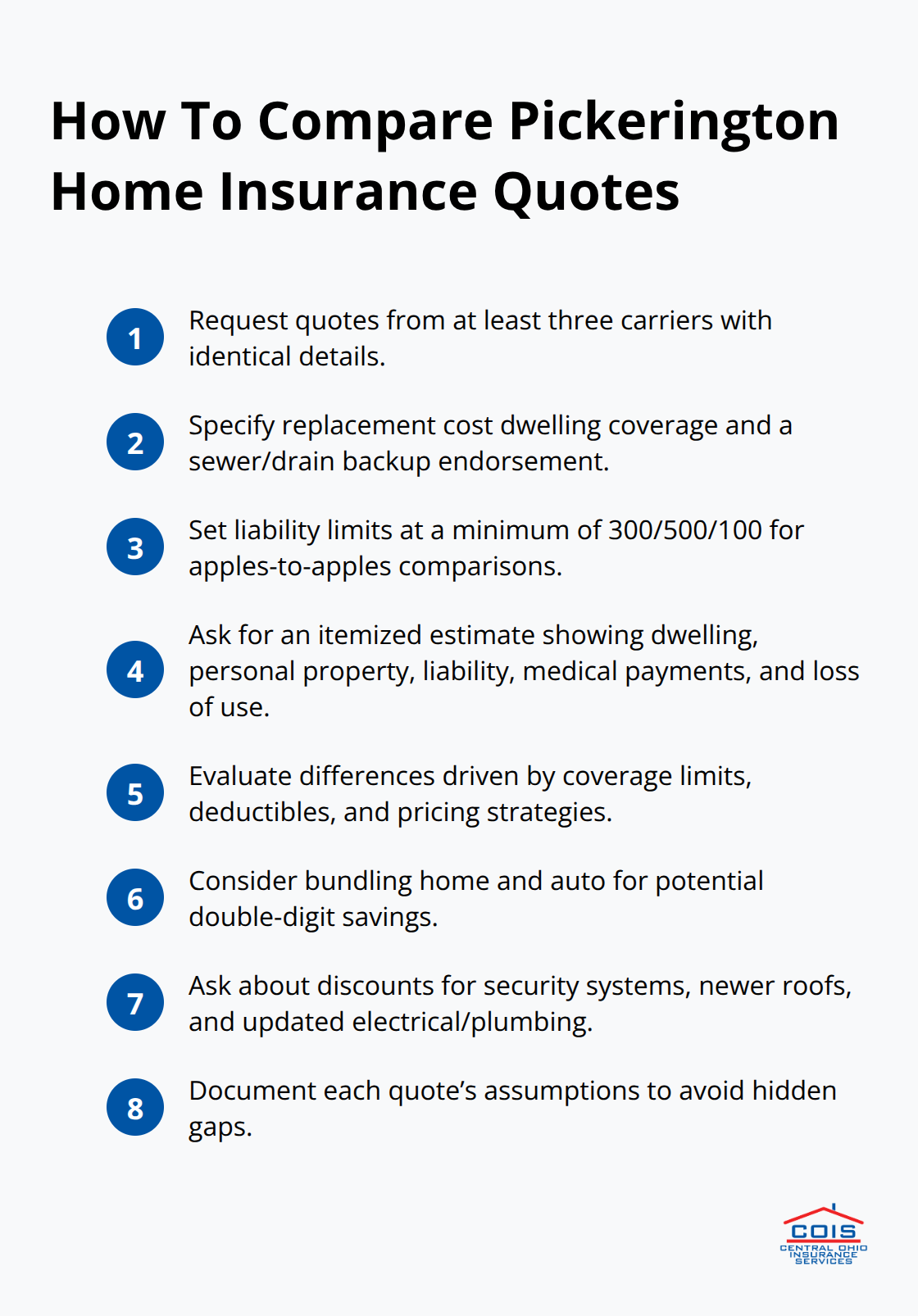

Request quotes from at least three carriers before making a decision, and provide identical information to each insurer so you can compare apples to apples. The variation in premium pricing is substantial-identical coverage on the same Pickerington home can range from $1,200 to $1,800 annually depending on the carrier’s underwriting practices and risk assessment. When you gather quotes, specify that you want replacement cost dwelling coverage, sewer backup endorsement, and liability limits of at least 300/500/100. Ask each insurer for a detailed written estimate that itemizes dwelling, personal property, liability, medical payments, and loss of use rather than accepting a single line-item quote.

This breakdown shows whether the premium difference stems from lower coverage limits, higher deductibles, or simply different pricing strategies. Bundling homeowners with auto insurance through the same carrier typically yields 10–25% savings according to industry practice, so factor this into your comparison. Some insurers offer discounts for security systems, newer roofs, or homes with updated electrical and plumbing-ask about available discounts before finalizing your choice.

Local Agents Understand Pickerington’s Specific Risks and Lender Requirements

An independent local agent in Pickerington has seen claims from wind damage, basement flooding, and hail impact in your specific neighborhood, which shapes smarter coverage recommendations than a national call center representative can provide. A local independent agency shops multiple carriers to find competitively priced solutions tailored to your actual exposure. A local agent also understands which Pickerington lenders require specific coverage language or minimum limits, preventing delays at closing or unexpected lender-placed policies that cost far more than self-selected coverage. After a loss occurs, a local agent advocates on your behalf with the insurance company, expedites inspections, and guides you through the claims process-this support proves invaluable when you’re stressed and making decisions about temporary housing or contractor selection. Schedule a no-obligation conversation with a Pickerington agent to review your home’s specifics and get recommendations before accepting any quote.

Final Thoughts

Protecting your Pickerington home requires three concrete actions: verify your dwelling coverage matches current rebuild costs, add water backup and flood endorsements to close coverage gaps, and carry adequate liability protection through homeowners and umbrella policies. Most homeowners discover their coverage falls short only after a loss occurs, which is why reviewing your policy now prevents financial devastation later. The difference between underinsurance and proper protection often amounts to a single conversation with someone who understands your neighborhood’s specific risks.

A local independent agency shops multiple carriers to find competitively priced solutions rather than steering you toward a single company’s products. This approach saves you money while ensuring your Pickerington homeowners insurance coverage actually matches your exposure. After a loss, a local agent advocates on your behalf with the insurance company, expedites inspections, and guides you through claims decisions when you’re stressed and overwhelmed.

Contact Central Ohio Insurance Services, Inc. for a no-obligation conversation about your home’s protection. Our licensed team will review your current coverage, identify gaps, and provide detailed quotes from multiple carriers so you can compare options side by side. We’ll explain what replacement cost coverage actually means for your situation and recommend appropriate liability limits based on your assets.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.