Pickerington auto insurance rates swing wildly depending on who you are and what you drive. We at Central Ohio Insurance Services, Inc. help drivers cut through the confusion by showing you exactly what affects your premiums and how to pay less.

This guide walks you through the real factors that shape your costs, introduces you to local options that actually compete for your business, and reveals practical ways to lower what you pay each month.

What Drives Pickerington Insurance Premiums Up and Down

Your driving record carries the heaviest weight in Pickerington rate calculations. A single speeding ticket raises your premium roughly 23.9% above the state average. An at-fault accident pushes costs up about 45%, while a DUI hits even harder at approximately 96% higher than baseline rates. These increases stick around for 3 to 5 years, so a mistake today shapes what you pay for years. If you’ve maintained a clean record for the past five years, you hold a strong negotiating position when shopping quotes.

Age Determines Your Starting Point

Pickerington rates climb steeply for younger drivers. An 18-year-old pays roughly $4,893 to $5,630 annually for full coverage, compared to about $2,218 to $2,384 for a 25-year-old and around $1,626 to $1,660 for a healthy 60-year-old, per Bankrate data. Teen drivers pay the highest rates in Pickerington specifically, making this a critical factor for families. If you add a teen to your policy, bundling them on a parent’s plan costs significantly less than a separate policy. A 25-year-old with full coverage in Pickerington sits close to the Ohio average of roughly $154 per month, while teenagers can expect double or triple that amount.

Your Vehicle Choice Shapes Monthly Costs

The car you drive directly affects what insurers charge. A BMW 330i runs about $2,337 annually for full coverage, while a Ford F-150 costs around $1,816 and a Toyota Camry approximately $1,842, according to Bankrate’s data. Repair costs, parts availability, and theft risk all factor into these premiums. If you’re shopping for a new vehicle, check insurance quotes before purchase to prevent surprises. A practical move: obtain quotes on two or three vehicles you’re considering, then factor that into your buying decision. Pickerington’s full-coverage average of roughly $1,791 per year means your actual cost depends heavily on what sits in your driveway.

Credit History Creates Dramatic Rate Swings

Credit history plays an outsized role that most drivers overlook. Excellent credit can net you approximately $1,492 annually for full coverage, while poor credit can balloon costs to $3,293 per year for the same coverage. That’s a $1,801 annual swing based entirely on your credit score. If your credit has improved recently, fresh quotes make sense because your rate might drop substantially without you realizing it. Local independent agencies like Central Ohio Insurance Services, Inc. shop multiple carriers to find the best rates for your specific profile, which matters especially when credit history or driving records complicate your situation.

Where to Find the Best Pickerington Rates

National carriers dominate advertising, but they rarely offer the best prices for Pickerington drivers. Geico averages roughly $131 per month for full coverage in Ohio according to MarketWatch data, while Erie Insurance undercuts nearly everyone on minimum coverage at about $25 to $26 monthly. These companies operate at massive scale, which means their algorithms price based on broad regional patterns rather than your specific local situation. A Pickerington driver with excellent credit and a clean record might qualify for better rates than their standard quote suggests, but you’d never know it without asking the right questions.

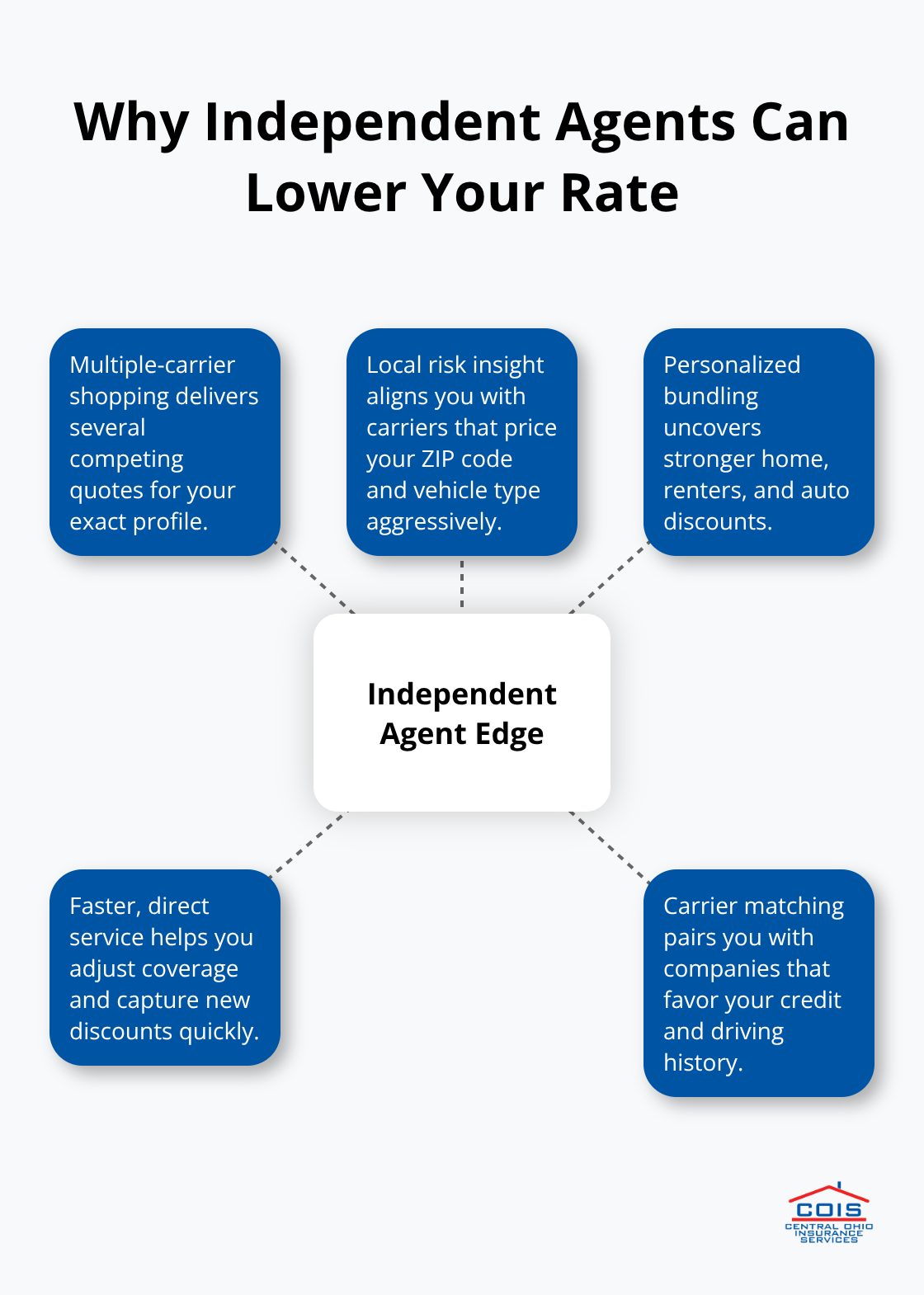

Independent Agents Shop Multiple Carriers

Independent insurance agencies operate under a fundamentally different business model than national carriers. Instead of steering you toward one company’s products, independent agents shop multiple carriers simultaneously to find competitive pricing for your specific situation. When you call a national carrier’s 1-800 number, you receive one quote. When you work with a local independent agency, you obtain multiple quotes from carriers that actually compete for your business. An independent agent brings these options to the table automatically.

The practical difference shows up in your monthly payment. A Pickerington driver might save $30, $50, or even $100 monthly simply because someone local knows which carriers offer the best rates for their age, vehicle, and driving history rather than accepting whatever a website calculator produces.

Local Knowledge Identifies Hidden Savings

Pickerington’s insurance costs reflect specific local risk factors that generic quotes miss. The city experiences higher auto theft rates than rural Ohio areas, which pushes premiums up across the board. Neighborhood crime patterns within Pickerington vary by ZIP code, affecting rates even among drivers living just blocks apart. A local agency understands these nuances because it serves this community daily and knows which carriers price aggressively in your specific ZIP code and which ones don’t.

Ohio’s at-fault insurance system and minimum liability requirements of 25/50/25 shape what coverage actually makes sense for Pickerington drivers. When you bundle auto insurance with home or renters coverage through one carrier, savings typically range from 10% to 25% depending on the insurer. A local independent agency identifies which carriers offer the strongest bundling discounts in Pickerington, then structures your policies to maximize those savings. Working locally also means faster service-you contact someone who knows your file immediately rather than navigating phone trees or waiting for callbacks from distant offices.

What Happens When You Compare Multiple Quotes

Shopping multiple carriers reveals dramatic price differences that most drivers miss. One carrier might price aggressively for your age and vehicle type while another charges a premium for the same profile. These variations exist because each insurer weights factors differently-some prioritize credit history heavily, others focus more on vehicle type or ZIP code risk. You only discover your best option by obtaining quotes from multiple carriers. The time investment often yields significant annual savings, making it one of the highest-return tasks a driver can complete.

How to Cut Your Pickerington Premiums Without Sacrificing Protection

Stack Discounts Through Policy Bundling

Combining home and auto policies remains one of the fastest ways to reduce what you pay each month. When you merge auto insurance with homeowners or renters coverage through a single carrier, most insurers discount your total premium by 10% to 25%, depending on which company you choose. On a Pickerington driver paying roughly $1,791 annually for full-coverage auto insurance, a 15% bundling discount saves approximately $269 per year. The math strengthens further if you add renters insurance or an umbrella policy to the mix. Some carriers weight bundling discounts more heavily than others, which means shopping around matters tremendously. Geico and Erie both offer substantial bundling incentives in Ohio, but comparing multiple carriers identifies which one offers the strongest discount for your specific situation rather than forcing you to call multiple companies yourself.

Leverage Vehicle Safety Features for Lower Rates

Vehicles equipped with anti-theft devices, collision-avoidance systems, or automatic emergency braking typically qualify for discounts ranging from 5% to 15% depending on the insurer. If you’re purchasing a new vehicle, obtaining quotes on models with advanced safety ratings before you buy ensures you factor insurance savings into your total cost of ownership. These features lower claim frequency, which directly reduces insurance costs. Defensive driving courses completed within the past three years can lower premiums by approximately 5% to 10% with most Ohio carriers, though you must take an approved course and provide proof to your insurer.

Adjust Deductibles to Match Your Financial Situation

Increasing your deductible from $500 to $1,000 cuts collision and comprehensive coverage costs by roughly 15% to 30%, but only pursue this strategy if you maintain an emergency fund capable of covering that amount out of pocket. This approach works well for drivers with stable finances and clean driving records who rarely file claims. Lower deductibles protect you if accidents happen frequently, while higher deductibles suit drivers confident in their ability to avoid incidents. The right choice depends entirely on your personal circumstances and risk tolerance.

Review Coverage Annually to Eliminate Waste

Annual policy reviews catch outdated coverage that no longer matches your needs, particularly if you’ve paid off your vehicle or moved to a lower-risk ZIP code within Pickerington. A driver who financed a car three years ago may still carry collision coverage on a vehicle worth far less than the deductible, effectively wasting money on protection they’ll never use. Reviewing coverage annually with your agent identifies these inefficiencies and redirects premium dollars toward the protection that actually matters for your situation. Life changes-vehicle payoffs, relocations, or improved driving records-shift what coverage makes financial sense.

Final Thoughts

Pickerington auto insurance rates reflect your unique situation, not some one-size-fits-all formula that national carriers apply to everyone. Finding the right balance between adequate protection and affordable premiums requires understanding what actually drives your costs, then taking action to reduce them without leaving yourself exposed to financial disaster. The drivers who pay the least aren’t necessarily the safest or youngest-they’re the ones who shop strategically, bundle policies, and work with someone who knows their local market.

Local expertise matters in Pickerington because your ZIP code, neighborhood crime patterns, and vehicle type interact in ways that generic online calculators simply cannot capture. A carrier that prices aggressively for your age and driving history might charge a premium for your vehicle type, while another company does the opposite. An independent agency like Central Ohio Insurance Services, Inc. shops multiple carriers simultaneously, identifying which ones compete hardest for your specific profile rather than forcing you to call five different companies yourself.

Obtain quotes from multiple carriers before your current policy renews and request bundling discounts if you carry home or renters insurance. Ask about safety feature discounts if your vehicle qualifies, and review your deductibles to confirm they match your financial situation. Central Ohio Insurance Services, Inc. handles this process for you as a local independent agency in Pickerington, shopping multiple carriers to deliver competitively priced solutions with fast quotes and clear guidance.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.