Most Columbus homeowners overpay for insurance because they don’t shop around or they compare quotes incorrectly. We at Central Ohio Insurance Services, Inc. help homeowners find real savings by getting multiple Columbus homeowners insurance quotes and understanding what actually drives your rate.

The difference between a quote that saves you money and one that doesn’t often comes down to knowing what to ask for and what to avoid. This guide walks you through the process.

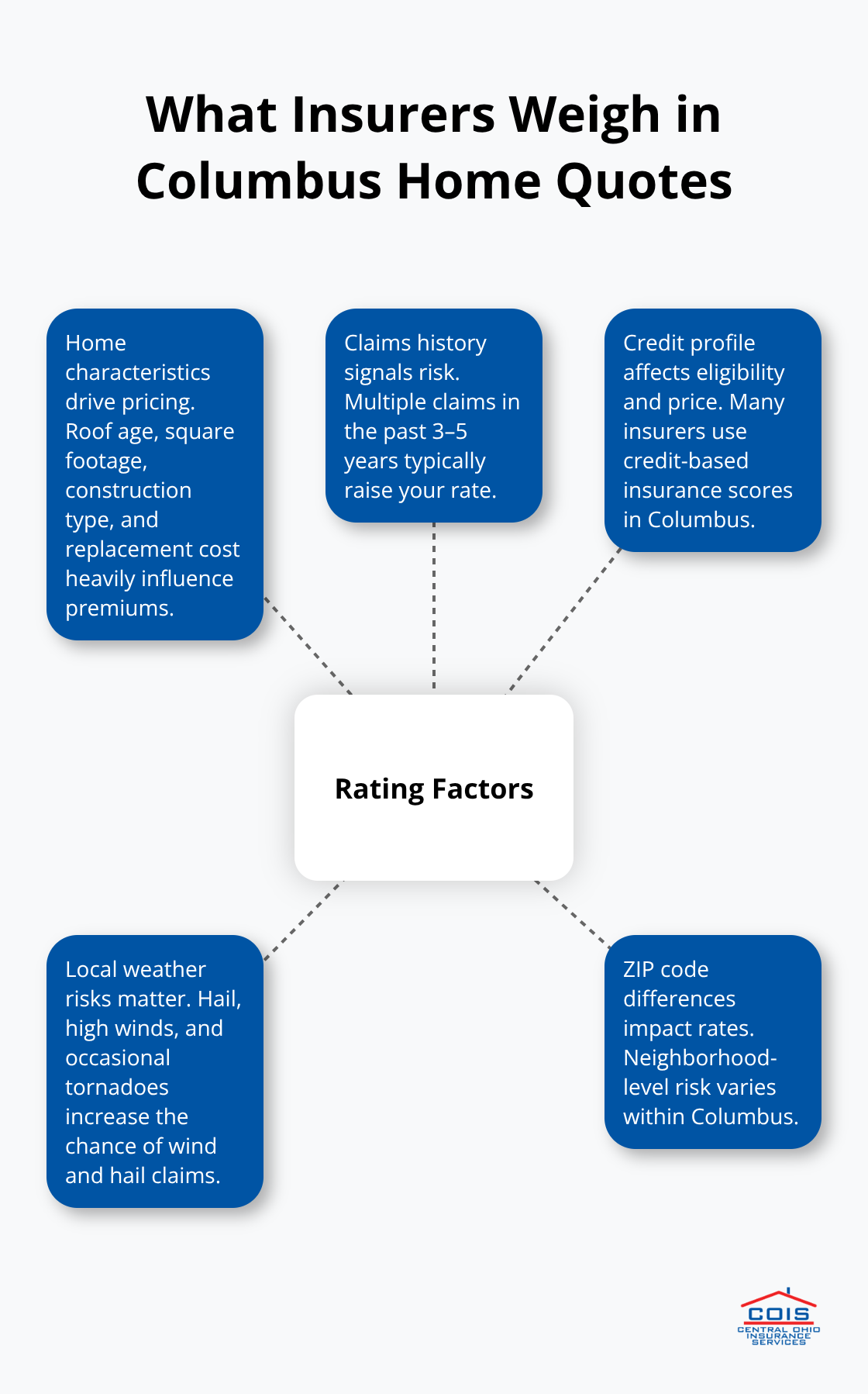

What Insurers Actually Look At When Quoting You

The Home Details That Drive Your Rate

Insurance companies calculate rates based on specific details about your home and history, not guesswork. When you request a Columbus homeowners insurance quote, the insurer evaluates your dwelling’s characteristics, your claims history, your credit profile, and local risk factors to arrive at a price. The home itself matters most: the age of your roof, square footage, construction type, and replacement cost all heavily influence what you’ll pay. A Columbus home built in 1960 with an original roof will cost significantly more to insure than an identical home with a new roof installed last year, because the older roof presents a higher risk of weather damage.

How Your History and Credit Affect Your Quote

Insurers examine your claims history over the past three to five years-filing multiple claims signals higher risk and raises your premium accordingly. Your ZIP code within Columbus matters too: the 43235 area and 43214 area each carry different risk profiles that affect pricing. Local weather exposure-hail, high winds, occasional tornadoes-affects pricing across Central Ohio, making wind and hail damage claims especially common in our region.

Why One Quote Tells You Almost Nothing

A single quote reveals almost nothing about whether you’re paying a fair price. When you compare three to five quotes from different carriers, you’ll see dramatic differences in pricing for the same coverage. The variation exists because each insurer weights risk factors differently and uses different underwriting models.

The Deductible and Bundle Effect on Your Price

Your deductible choice shifts the quote dramatically: raising it from $500 to $2,000 can save you money on your Columbus premium. Bundling your home and auto policies cuts costs depending on the carrier, which means a quote for homeowners insurance alone doesn’t reflect your actual savings potential.

Comparing Apples to Apples Reveals True Value

Before accepting any quote, verify you’re comparing identical coverage levels: the same dwelling limit, same deductible, same liability coverage, and the same add-ons like water backup or replacement-cost endorsements. Comparing apples to apples reveals which carrier genuinely offers better value rather than just a lower number on a different product. This accuracy in comparison sets you up to spot the mistakes most Columbus homeowners make when they request quotes.

Common Mistakes Columbus Homeowners Make When Getting Quotes

Providing Inaccurate Home Details Sabotages Your Quote

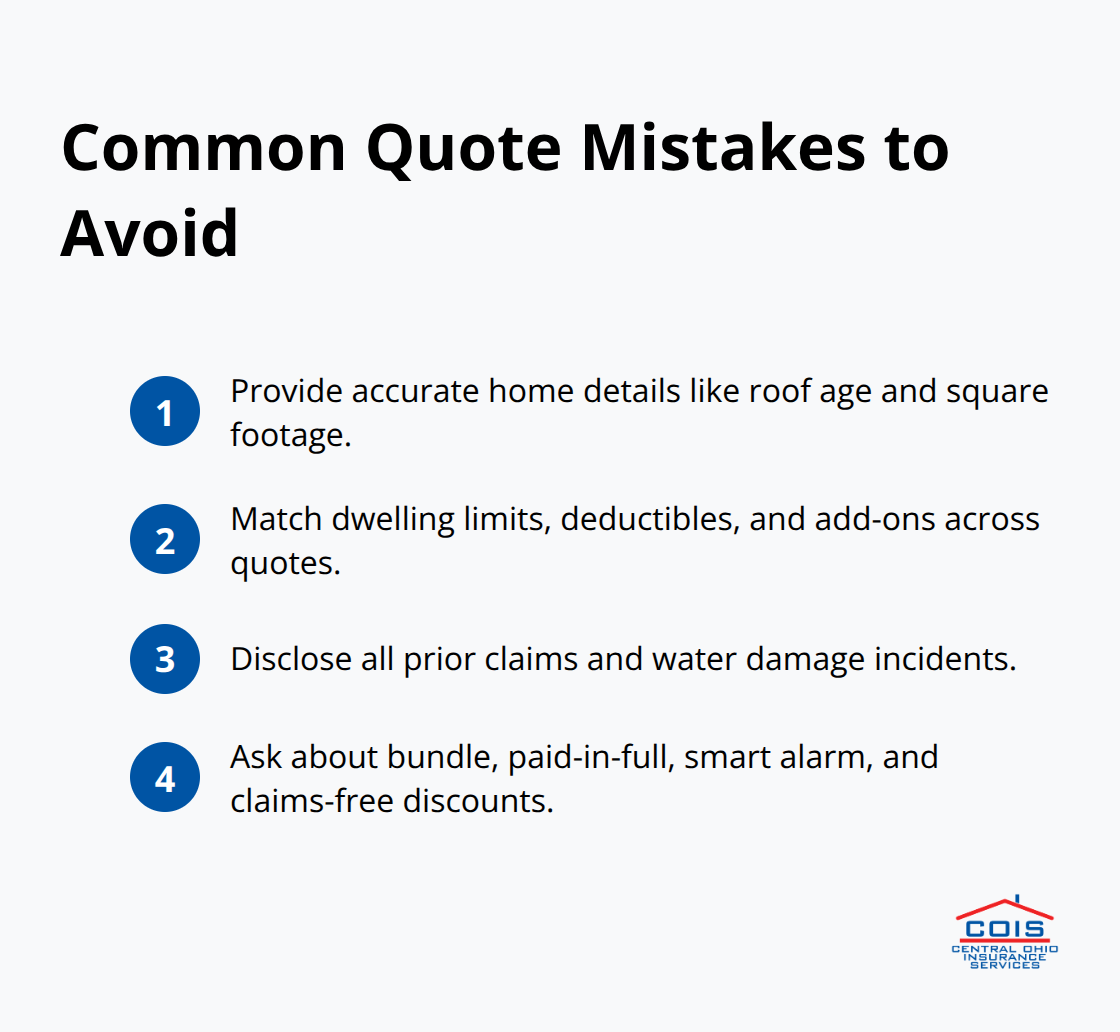

Most Columbus homeowners sabotage their own quote comparisons without realizing it. The first major mistake is providing incomplete or inaccurate home details when requesting quotes. When you tell an insurer your roof is ten years old but it’s actually fifteen, or you mention your home is 2,000 square feet when it’s really 2,400, the quote you receive won’t match your actual risk profile. Insurers will adjust your premium dramatically once they verify the real details during underwriting, which means you’ll face a higher bill than expected after you’ve already committed to a policy.

The same applies to misrepresenting your claims history or omitting previous water damage incidents. Accuracy matters because insurers like Cincinnati Insurance, Erie, and State Farm all base their pricing models on verified home characteristics. If your details are fuzzy during the quote stage, you’re essentially getting a quote for someone else’s house.

Comparing Different Coverage Levels Masks True Costs

The second critical error is comparing coverage that doesn’t match across quotes. Columbus homeowners often receive quotes with different dwelling limits, deductibles, or add-ons, then pick the lowest number without noticing the actual protection differs. A quote for $1,200 per year with a $2,000 deductible and $300,000 dwelling coverage is fundamentally different from a $1,400 quote with a $500 deductible and $350,000 coverage.

NerdWallet’s 2026 analysis shows homeowners insurance costs vary significantly based on credit and other factors, but that figure only matters if you’re comparing identical policies. When evaluating quotes, verify the same liability limits, the same water backup endorsement status, and whether both include replacement-cost or actual cash value coverage. This apples-to-apples comparison reveals which carrier genuinely offers better value rather than just a lower number on a different product.

Failing to Request Available Discounts Costs You Thousands

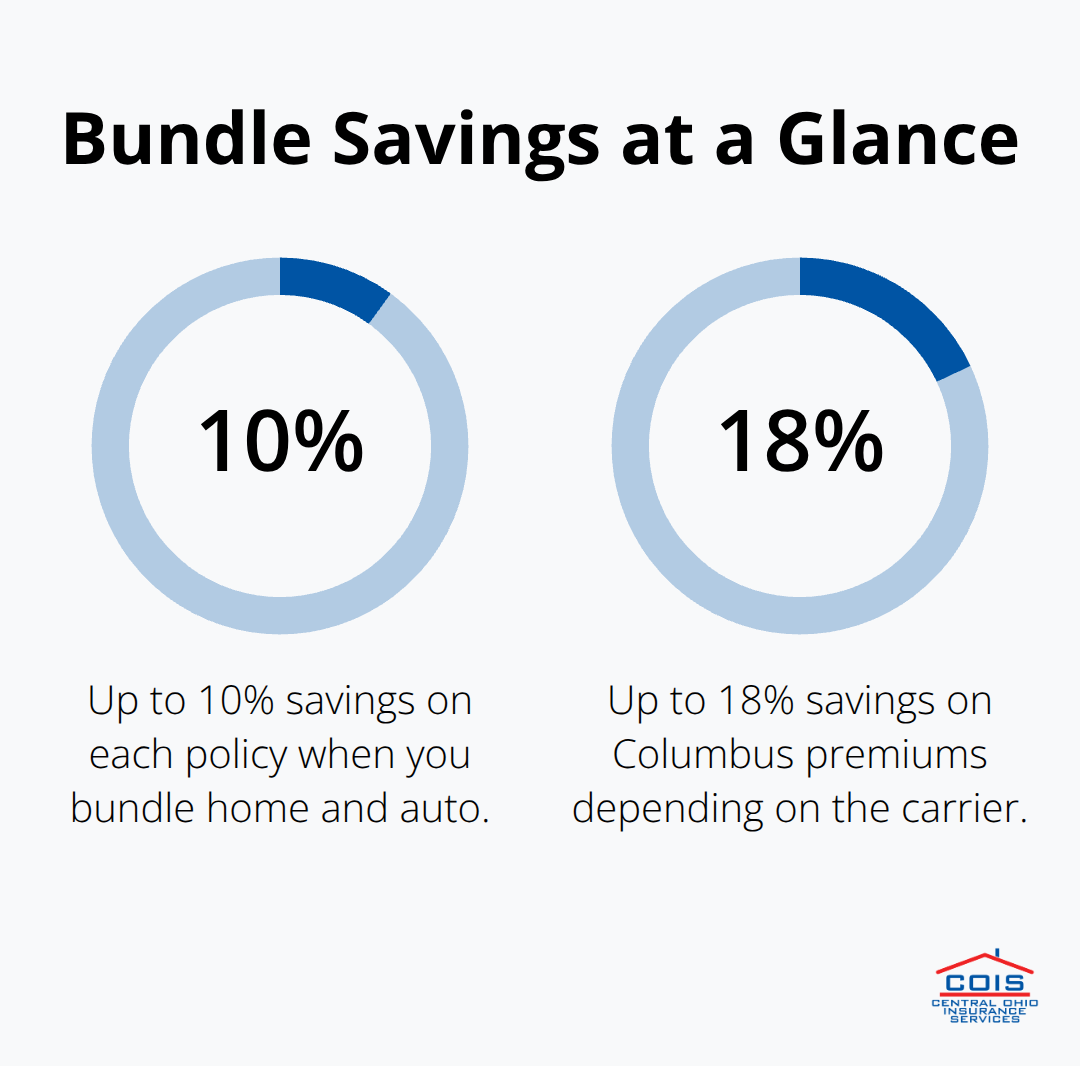

Many Columbus homeowners miss discounts entirely because they never ask about them. Bundling home and auto policies saves up to 18 percent on Columbus premiums depending on your carrier, yet homeowners shopping for homeowners quotes alone never discover this savings. Similarly, paid-in-full discounts, smart alarm discounts, and claims-free discounts exist but require you to explicitly request them during the quote process. If you don’t mention your security system, your perfect claims history, or your willingness to pay annually instead of monthly, the insurer won’t factor those savings into your initial quote.

This is where working with an independent agency like Central Ohio Insurance Services, Inc. makes a real difference-we shop multiple carriers and actively uncover discounts you’d otherwise miss on your own.

How to Cut Your Columbus Premium Without Sacrificing Coverage

Bundle Your Home and Auto Policies for Immediate Savings

Combining your home and auto policies stands as the single most effective way to lower your Columbus homeowners insurance cost, and the math is straightforward. Bundling your home and auto policies saves up to 10% on each policy according to recent market data, which translates to real money in your pocket every month. If your current homeowners quote sits at $1,300 annually, a bundle discount cuts that to roughly $1,170 per year. Insurers reward bundling because they’d rather keep your entire business than risk losing you to a competitor. When you request quotes, ask carriers specifically what their bundle discount is and whether they apply it automatically or require you to mention it.

Some carriers like Grange emphasize their multi-policy discounts prominently, while others bury the savings unless you ask directly.

Raise Your Deductible If You Have Emergency Savings

Your deductible choice delivers the second-largest premium reduction available to you, and the numbers prove it’s worth considering a higher amount if you can afford it. According to NerdWallet, raising your deductible from $500 to $2,000 on a Columbus home reduces the annual premium from approximately $1,812 to $1,464, saving about $348 per year. That $348 annual savings compounds over five years to $1,740 in reduced premiums, which covers most deductible increases many times over. The critical question is whether you have liquid savings to handle a $2,000 out-of-pocket expense if a claim occurs. If you maintain an emergency fund of $3,000 or more, a $2,000 deductible makes financial sense. If your savings sit below $2,000, stick with a $500 or $1,000 deductible because the premium savings won’t help if you can’t pay the deductible when you need coverage.

Claim Every Home Safety and Security Discount

Home safety features and security systems round out your discount opportunities, though these savings vary more than bundling and deductible adjustments. Paid-in-full discounts reward annual payments instead of monthly installments, smart home alarms can reduce premiums, and a claims-free history signals lower risk to insurers. When you request quotes, explicitly mention any central station burglar alarm, fire alarm system, or smart home devices you own because carriers won’t assume you have them. The combination of bundling, strategic deductible selection, and claiming every applicable discount can easily reduce your Columbus homeowners insurance by 25 to 35 percent compared to a baseline quote with no optimization. Central Ohio Insurance Services, Inc. shops multiple carriers to help you uncover these discounts and apply them correctly across your policies.

Final Thoughts

Getting Columbus homeowners insurance quotes is only the beginning of your savings journey. The real work happens when you compare those quotes accurately, ask about discounts, and adjust your coverage to match your actual needs and financial situation. Most homeowners stop after receiving one or two quotes and accept the first offer, which leaves hundreds of dollars on the table every year.

An independent agency eliminates the guesswork and ensures you don’t miss discounts or coverage options that apply to your specific situation. When you contact Central Ohio Insurance Services, Inc., you gain access to multiple carriers at once rather than requesting quotes individually from each company. We shop several carriers simultaneously, then present you with apples-to-apples comparisons that reveal genuine savings opportunities.

Your policy isn’t static after you purchase it-annual reviews catch rate increases before they compound and identify new discounts you may now qualify for. Life changes like completing a home renovation, installing a security system, or improving your credit score can lower your premium when you shop again. Contact us today to request updated Columbus homeowners insurance quotes from multiple carriers and find the savings you deserve.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.