Condo living in Columbus offers urban convenience, but it comes with unique insurance challenges that many owners overlook. Standard homeowners policies won’t cut it-you need Ohio condo insurance in Columbus specifically designed for your situation.

At Central Ohio Insurance Services, Inc., we’ve helped countless condo owners discover the gaps in their coverage before disaster strikes. Let’s walk through what you actually need to protect your investment.

Why Your Standard Policy Falls Short in Columbus

The Coverage Gap That Catches Most Condo Owners Off Guard

Condo owners in Columbus face a critical protection gap that most don’t realize until disaster strikes. Standard homeowners insurance is designed for single-family homes where you own the entire structure-walls, roof, foundation, everything. When you own a condo, the building itself is covered by your association’s master policy, which means your individual homeowners policy becomes almost useless for structural damage. According to Ohio Revised Code 5311.16, condo associations must carry liability insurance and fire coverage on the building, but that master policy protects only the common elements and the building shell. Your interior walls, custom fixtures, and personal belongings remain your responsibility alone.

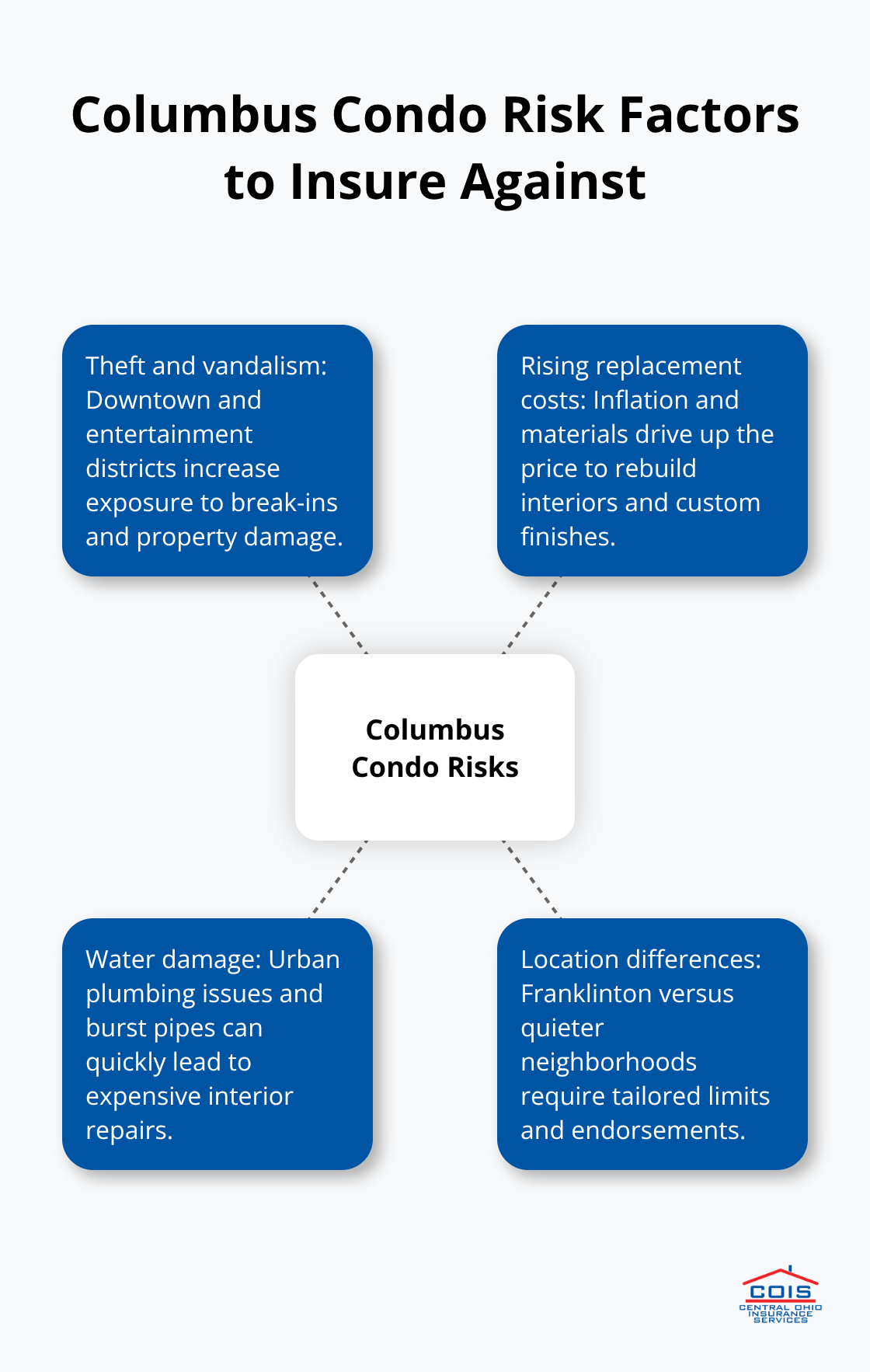

Most condo owners discover this gap when water damage from a burst pipe in their unit occurs, only to find their standard policy won’t pay because they assumed the association’s coverage would handle it. That assumption costs them thousands. The association’s policy covers damage to the building structure itself, not your unit’s interior improvements or contents. You need a condo-specific policy that covers your interior walls, flooring, cabinetry, and appliances-items that aren’t technically part of the common building but are part of your investment.

Rising Replacement Costs in Columbus’s Growing Market

Columbus’s condo market has experienced steady growth over the past five years, with downtown and urban neighborhoods like Franklinton seeing increased property values and development activity. This growth matters for your insurance because replacement costs are rising. If you purchased your condo three years ago, the replacement cost of your interior has likely increased due to inflation and material costs. Many condo owners keep the same coverage limits they had at purchase, which means they’re increasingly underinsured.

Location-Specific Risks in Urban Columbus

Additionally, Columbus condos near downtown or popular neighborhoods carry higher theft and vandalism risk than suburban homes. The proximity to entertainment districts, transit hubs, and visitor traffic means your unit faces greater exposure to break-ins and property damage. A condo-specific policy addresses this by allowing you to set appropriate personal property limits based on your actual contents and current replacement costs, not some generic formula.

Your location in Columbus directly influences what coverage you actually need. A unit in Franklinton near the Short North Arts District faces different risks than one in a quieter neighborhood. The right policy reflects these differences and protects you accordingly.

What Your Condo Insurance Actually Protects

Dwelling Coverage: Your Interior Investments

Your condo insurance policy in Ohio covers three distinct areas that your association’s master policy leaves exposed. Dwelling coverage protects your interior walls, flooring, cabinetry, countertops, and built-in appliances-everything from drywall inward that you’ve invested in or improved. This is the layer most condo owners misunderstand. When a pipe bursts and floods your unit, your association’s policy covers structural damage to the building shell, but your dwelling coverage pays to replace your hardwood floors, kitchen upgrades, and bathroom fixtures.

Personal Property and Contents Protection

Personal property coverage protects your movable belongings-furniture, electronics, clothing, kitchenware-at replacement cost. In Columbus, where condo values have climbed steadily, many owners carry coverage limits set years ago that no longer reflect what they actually own. A three-bedroom unit in Franklinton might contain $50,000 to $80,000 worth of furnishings and electronics, yet owners often keep $25,000 limits from their original policy.

Liability and Additional Living Expenses

Liability coverage protects you if someone is injured in your unit or if you accidentally damage another unit. Ohio law requires associations to carry liability insurance per ORC 5311.16, but that covers common areas only-your unit’s liability exposure falls entirely on you. Additional living expenses coverage reimburses hotel, food, and other costs if your unit becomes uninhabitable after a covered loss, which matters in Columbus where temporary housing can run $150 to $250 nightly.

Calculating Your Actual Coverage Needs

Most Columbus condo owners underinsure their dwelling and personal property coverage. You need to walk through your unit and calculate what it would cost to replace everything you own plus rebuild your interior to current market standards. Don’t rely on purchase price or rough estimates. Contractors’ quotes for kitchen and bathroom replacement, flooring, and painting reveal the true costs-these expenses have risen sharply in Columbus over the past three years due to material inflation. Add 20 percent as a cushion to your total.

Your liability limit should reflect your unit’s size and guest exposure. A one-bedroom unit might justify $300,000 in liability coverage, but a three-bedroom near downtown where you host frequent visitors should carry $500,000 or higher. Many carriers offer discounts for bundling condo insurance with auto or umbrella policies, which can offset higher dwelling limits.

Staying Current With Your Coverage

You should review your policy annually and after any significant home improvements, because every upgrade you make increases what needs protecting. Your kitchen renovation, new flooring, or bathroom remodel all add value that your original coverage limits no longer protect. The right policy matches your coverage to your actual situation, not whatever limits came with your original policy. As you assess your specific needs, understanding how to compare quotes from multiple carriers becomes your next critical step.

Picking the Right Policy for Your Columbus Condo

Review Your HOA’s Master Policy First

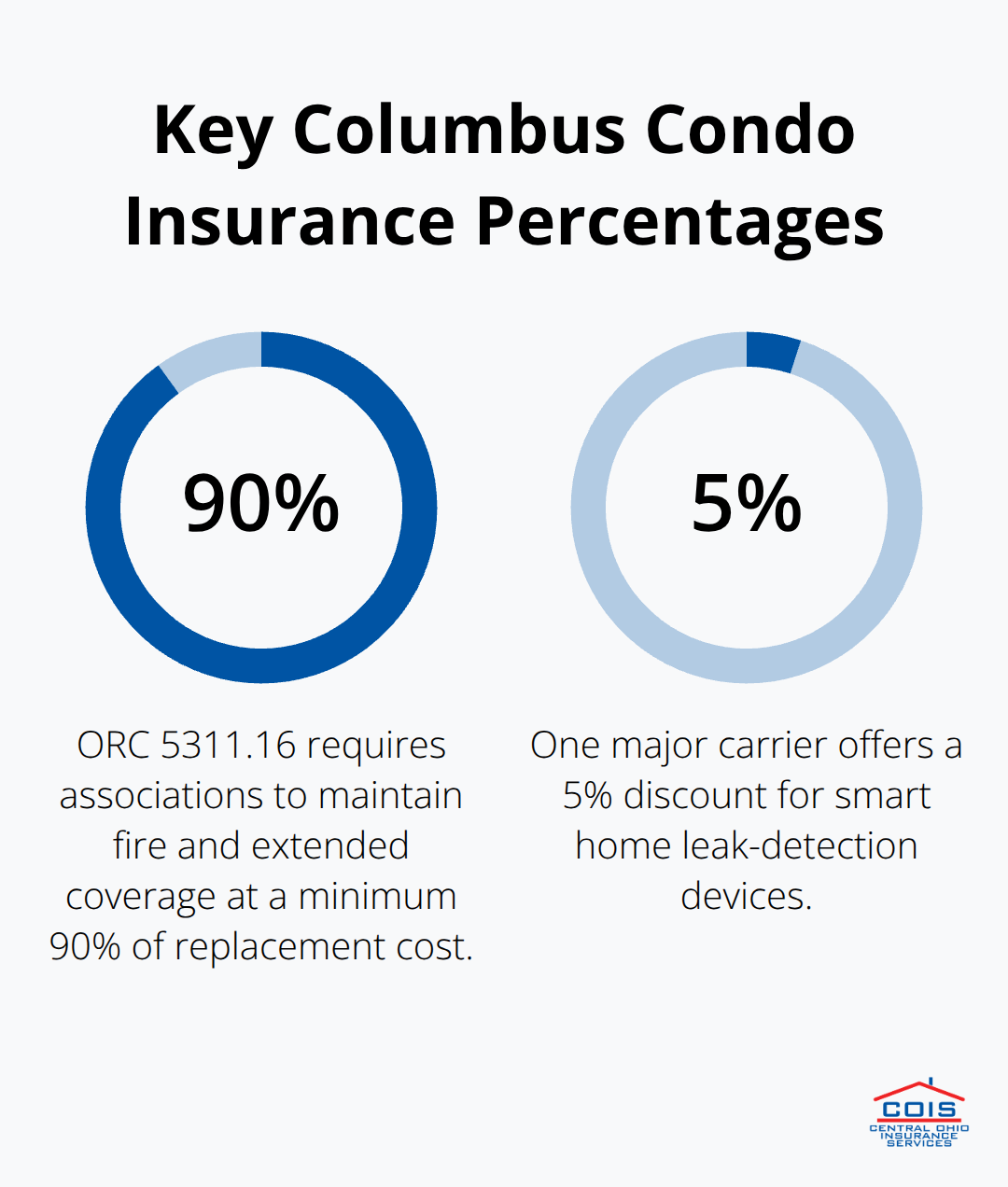

Start with your HOA’s master policy document-not the summary, the actual policy. Most Columbus condo owners never read it, which means they don’t know what their association actually covers or what deductibles apply. Call your property manager and request the full master policy, then look for three specific details: the dwelling coverage limit (stated as a percentage of replacement cost, typically 80-90%), the liability limit (usually $1-2 million), and the deductible amount. Ohio Revised Code 5311.16 requires associations to maintain fire and extended coverage at minimum 90% of replacement cost, but your association might carry more. If your master policy has a $25,000 deductible and your unit suffers water damage, you pay that full amount before coverage kicks in-this is why your individual condo policy must address what the master policy leaves uncovered. Once you understand what the association covers, you know exactly what gaps your personal policy must fill.

Calculate Your Dwelling and Personal Property Limits

Your dwelling coverage should start at a minimum of $50,000 for a one-bedroom unit in Columbus, rising to $80,000-$120,000 for larger units with upgraded finishes. Get three contractor quotes for interior replacement costs in your specific neighborhood-Franklinton and Short North properties command different pricing than suburban areas. This approach gives you actual numbers, not insurance company estimates. Your personal property limit should equal the total replacement cost of everything you own, calculated item-by-item. Most carriers let you add scheduled coverage for high-value items like electronics or jewelry at modest additional cost, which proves smarter than raising your overall personal property limit.

Compare Quotes Across Multiple Carriers

Comparing quotes from multiple carriers reveals massive pricing differences-identical coverage costs $400 more annually with one carrier versus another in Columbus. Request quotes from at least three insurers, but make sure each quote covers the exact same dwelling limit, personal property amount, and liability coverage. Don’t just look at the premium; examine what each policy excludes and what endorsements cost. Some carriers charge $50-$100 extra to add water backup coverage, while others include it. In Columbus, where urban plumbing issues and sump pump failures occur regularly, water backup coverage isn’t optional-it’s essential. Ask each carrier about discounts for bundling (typically 10-15% savings), paying annually instead of monthly, or installing security systems. One major carrier offers a 5% discount for smart home devices that monitor for water leaks, which directly addresses Columbus condo risks.

Work With an Agent Who Knows Your Neighborhood

When you receive quotes, call the agent and ask specifically about their experience with condo claims in your neighborhood. An agent who handles dozens of Franklinton condos understands the local risks and can spot gaps in coverage that a national carrier’s algorithm might miss. A local independent agency shops multiple carriers for every client because no single insurer offers the best rates and coverage for every situation-your specific unit, location, and risk profile determine which carrier actually makes sense.

Identify Coverage Exclusions and Special Protections

After comparing quotes, work with an agent to review what each policy excludes. Standard condo policies exclude earthquake, flood, and certain water damage scenarios. Columbus isn’t in a high-earthquake zone, but flooding is a legitimate risk near the Scioto River or in low-lying areas. If your unit is within a flood zone, you’ll need a separate flood policy, which the National Flood Insurance Program administers-don’t assume your condo policy covers it. An agent should also identify whether your policy covers loss assessment, which protects you if the HOA needs special assessments from owners after a major loss. This coverage costs $30-$50 annually but can save you thousands if your association faces an uninsured claim in common areas.

Final Thoughts

Protecting your Columbus condo requires more than a standard homeowners policy-you need Ohio condo insurance specifically designed for the gaps that master policies leave uncovered. Your interior walls, personal belongings, and unit-specific liability exposure all fall on you, not your association. Review your HOA’s master policy to understand what it covers, calculate your dwelling and personal property limits based on real replacement costs in your neighborhood, and compare quotes from multiple carriers to find coverage that matches your actual risk profile.

Your location in Columbus directly influences what coverage you need. A unit in Franklinton near downtown faces different theft and water damage risks than one in a quieter area, and your policy should reflect those differences. Rising property values in Columbus mean replacement costs have climbed since you purchased your condo-coverage limits set years ago no longer protect your investment, so annual policy reviews catch these gaps before they cost you thousands out of pocket.

Local expertise makes the difference between adequate coverage and discovering gaps when disaster strikes. An agent who understands Columbus condo claims knows which carriers offer the best rates for your specific situation and which endorsements actually matter for urban properties. Contact us at Central Ohio Insurance Services, Inc. to review your coverage and ensure your urban oasis is properly protected.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.