Your vehicle is one of your biggest investments, and protecting it with the right Central Ohio car insurance matters more than you might think. Weather patterns, road conditions, and local traffic risks in our region create unique coverage needs that national carriers often overlook.

We at Central Ohio Insurance Services, Inc. understand what it takes to keep your vehicles protected with policies built for Central Ohio drivers. This guide walks you through your coverage options, how to find affordable rates, and why working with a local agent makes a real difference.

Why Local Agents Beat National Carriers for Central Ohio Drivers

Regional Weather and Traffic Create Unique Coverage Needs

Central Ohio’s weather and traffic patterns demand insurance solutions that national call centers cannot provide. Columbus receives an average of 51 inches of annual precipitation, with winter storms that bring ice accumulation and reduced visibility on major corridors like I-270 and I-71. These conditions drive up collision and comprehensive claims in our region compared to national averages. Urban density in Columbus also matters-the city averages about $2,092 per year for full-coverage auto insurance, well above Ohio’s statewide average of $1,842, because accident frequency rises in densely populated areas. National carriers use broad geographic pricing models that lump Central Ohio into regional buckets, missing the specific risk factors that affect your actual premium and coverage needs.

Shopping Multiple Carriers Saves You Money

An independent agent at a local agency shops multiple carriers on your behalf instead of locking you into one company’s rates and products. This competition between insurers directly lowers your costs-drivers who switch carriers save $759 to $1,019 annually depending on their current provider. Local agents understand which carriers offer the best rates for your specific situation: a young driver in Westerville faces different pricing than a mature driver in Circleville, and a local agent knows these differences because they work in the community. They also know which discounts apply to your household-bundling auto with homeowners insurance can save over 25 percent nationally, and local agents catch multi-policy discounts that online quote tools sometimes miss.

Personalized Service National Carriers Cannot Match

National carriers prioritize speed and volume; they process thousands of quotes daily with minimal customization. A local independent agent invests time understanding your vehicle type, driving history, credit profile, and coverage preferences, then compares actual quotes from four to six carriers instead of selling you one company’s standard package. If you have a speeding ticket on your record, a local agent knows which carriers forgive minor violations and which penalize them heavily-a difference that could cost you $200 to $400 annually. When a claim happens, local agents advocate for you with adjusters in the same region rather than routing you through a national claims center where your case becomes a case number.

Local Knowledge Protects Your Interests

Central Ohio Insurance Services, Inc. operates from Pickerington with licensed staff who understand local roads, local insurers’ practices, and local risks. This local foundation gives you an advantage that no national 1-800 number can match. Your agent knows the specific carriers that offer competitive rates in your ZIP code and which ones charge premiums that don’t reflect actual local risk. When you need guidance on whether collision coverage makes sense for your vehicle or how much liability protection your assets require, a local agent provides answers based on what works for Central Ohio drivers-not generic national advice.

Coverage Decisions Require Local Context

The coverage options available to you depend partly on where you live and how you drive. A local agent helps you navigate liability limits, physical damage protection, and optional coverages like uninsured motorist coverage with an understanding of Central Ohio’s specific accident patterns and claim frequencies. This context matters when you decide whether to add comprehensive and collision coverage or when you evaluate deductible levels that balance your budget against your risk tolerance. Your next step involves understanding what coverage options actually protect your vehicle and finances in Central Ohio’s driving environment.

What Coverage Do You Actually Need in Central Ohio

Liability Coverage Protects Your Financial Future

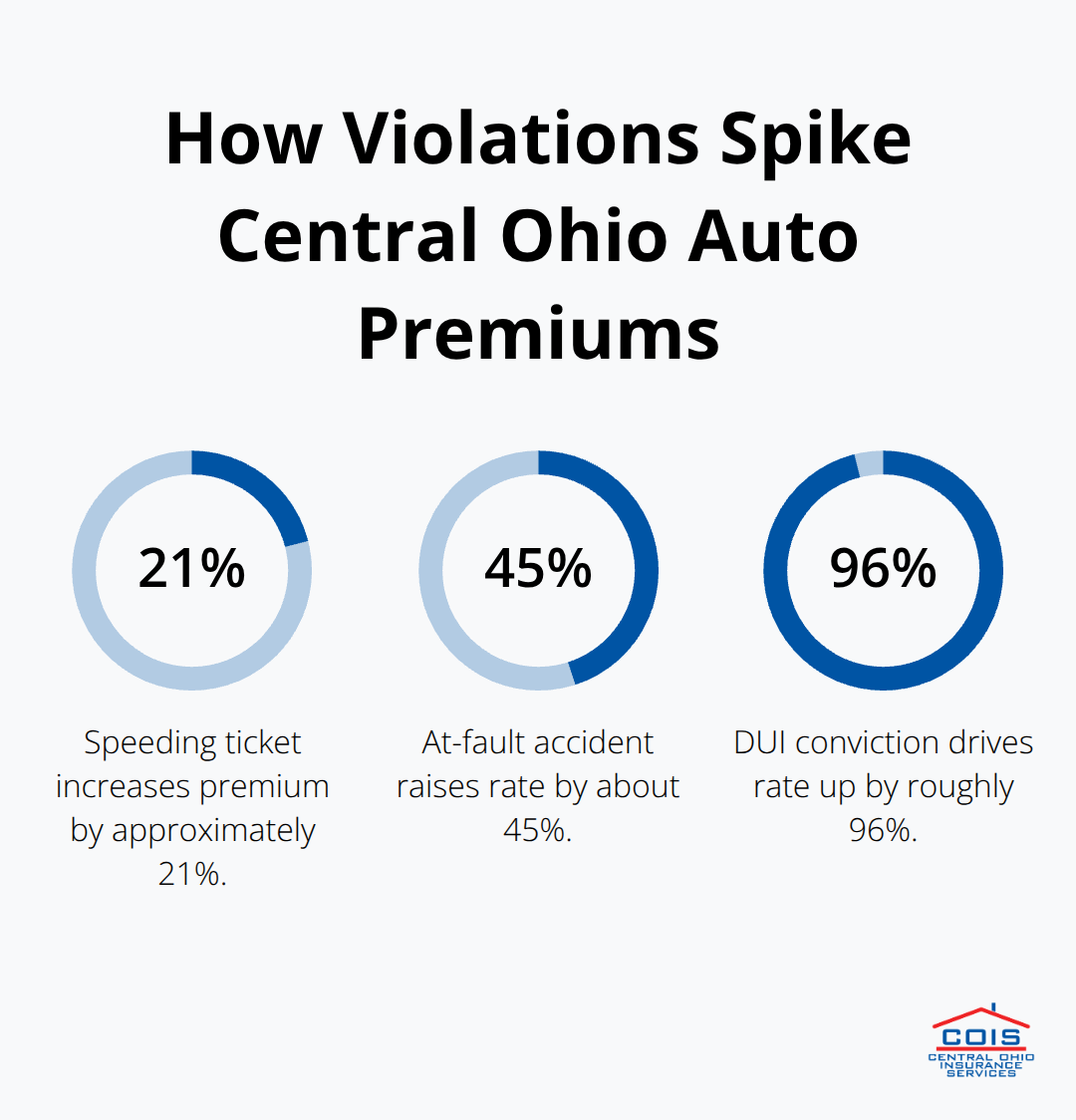

Ohio’s minimum liability requirements of $25,000 per person and $50,000 per accident leave your finances dangerously exposed. If you cause an accident and injure someone seriously, medical bills can easily exceed $100,000, and you’ll pay personally for anything above your policy limit. Central Ohio’s higher accident frequency in Columbus and surrounding areas means liability claims happen more often here than statewide averages suggest, so carrying limits closer to $50,000 per person and $100,000 per accident protects your actual assets. A speeding ticket adds roughly 21 percent to your premium, and an at-fault accident bumps rates by about 45 percent-the difference between minimum coverage and adequate coverage becomes irrelevant once you file a claim that exceeds your limits.

Collision and Comprehensive Coverage Matters More in Urban Areas

Collision and comprehensive coverage matters more in Central Ohio than in rural Ohio counties because urban density drives claim frequency higher. Columbus averages $2,092 annually for full-coverage insurance versus $1,842 statewide, reflecting the real risk difference in our region. If you financed or leased your vehicle, your lender requires both coverages. Even without that mandate, comprehensive coverage pays for theft, hail, and weather damage-Central Ohio’s 51 inches of annual precipitation means ice storms and hail events happen regularly enough to justify the protection. Collision coverage covers accidents you cause or damage from impact, and choosing a $500 deductible versus $1,000 costs roughly 15 to 20 percent more annually but makes sense if you have limited savings for repairs.

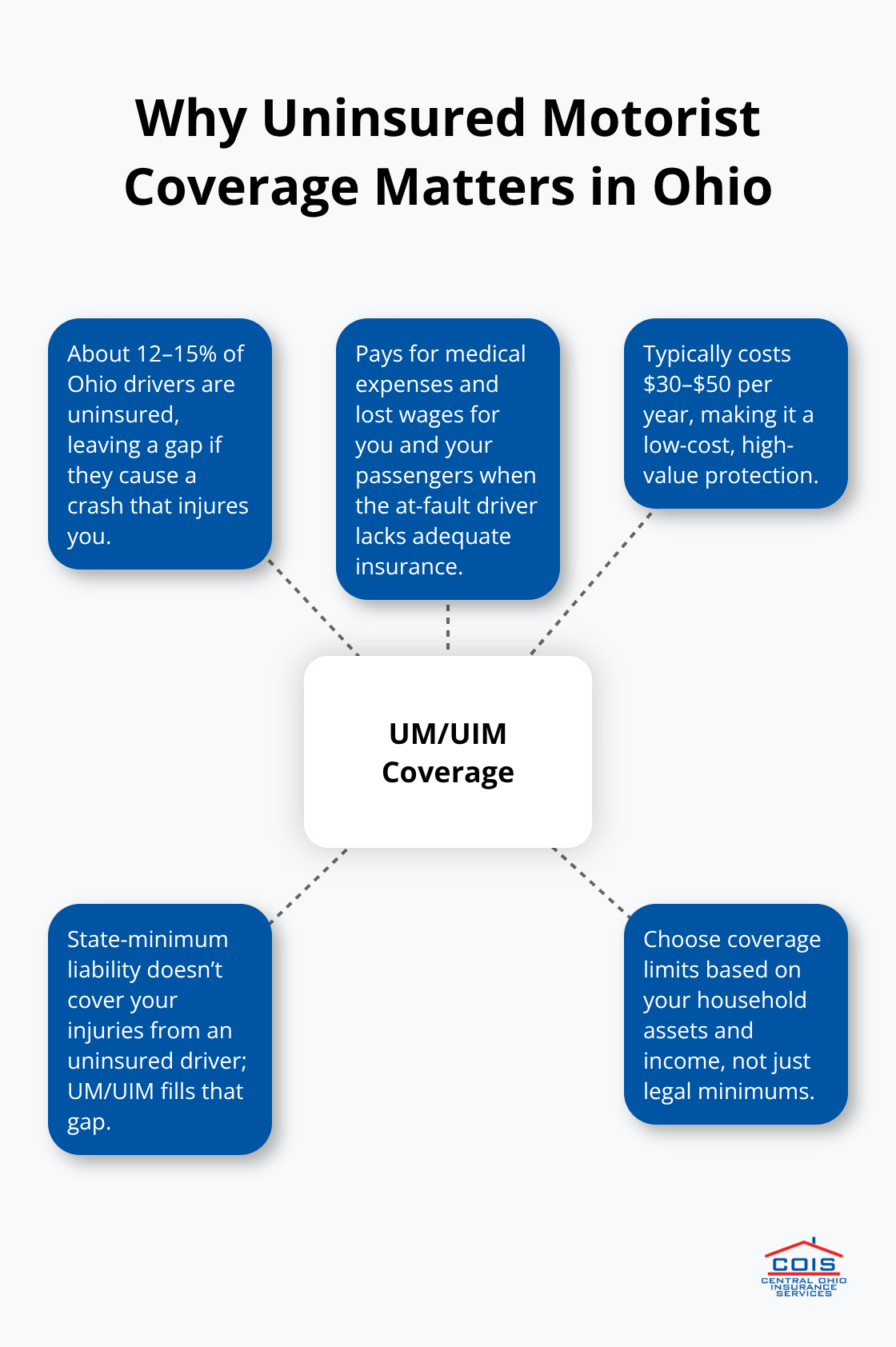

Uninsured Motorist Coverage Fills a Critical Gap

Uninsured and underinsured motorist coverage protects you when another driver lacks adequate insurance or carries none at all. Ohio requires you to carry at least the state minimum in liability coverage, but roughly 12 to 15 percent of Ohio drivers remain uninsured, meaning collision alone won’t cover injuries to you or your passengers if they hit you. This optional coverage costs little-typically $30 to $50 annually-and covers medical expenses and lost wages for you and your family when an uninsured driver causes the crash.

Your household assets and income should guide your coverage limits rather than settling for minimums, since the goal of insurance is protecting what you’ve built, not just meeting legal requirements. Understanding your specific coverage needs sets the stage for finding rates that actually fit your budget and situation.

What Really Drives Your Central Ohio Car Insurance Rate

Location and Urban Density Shape Your Premium

Your Central Ohio auto insurance premium reflects where you live more than most drivers realize. Columbus ZIP codes carry different risk profiles than rural areas, and insurers price accordingly based on accident frequency and traffic congestion. Urban density in Columbus pushes full-coverage premiums to about $2,092 annually, roughly $250 more than Ohio’s statewide average of $1,842, because accidents correlate directly with population density. Surrounding areas show variation: Reynoldsburg averages around $2,032 annually, while Circleville sits closer to $1,780 for full coverage. This geographic pricing reflects real claim data, not arbitrary regional buckets that national carriers apply across broad territories.

Driving History and Credit Profile Impact Rates Significantly

Your past driving decisions and financial responsibility directly affect what you pay. A single speeding ticket raises your rate by approximately 21 percent, an at-fault accident by about 45 percent, and a DUI conviction by roughly 96 percent according to Bankrate’s analysis. Credit history matters equally-poor credit increases your costs by about 79 percent compared to excellent credit, while excellent credit can lower your rate by roughly 19 percent.

These factors compound quickly: a young driver with a recent accident in Columbus faces substantially different pricing than a 55-year-old with a clean record in Circleville. Age itself carries weight too-a 25-year-old pays around $2,384 annually for full coverage, while mature drivers typically pay significantly less for identical protection.

Vehicle Type and Age Determine Repair and Theft Risk

What you drive influences your premium substantially. A BMW 330i costs about 29 percent more to insure than a Ford F-150 in Ohio, reflecting repair costs and theft risk. Newer vehicles with advanced safety features often qualify for discounts that older cars cannot access. Specialty vehicles like motorcycles, RVs, and collector cars require different rating formulas entirely, which is why comparing quotes across carriers matters-one insurer may price your specific vehicle type more competitively than another.

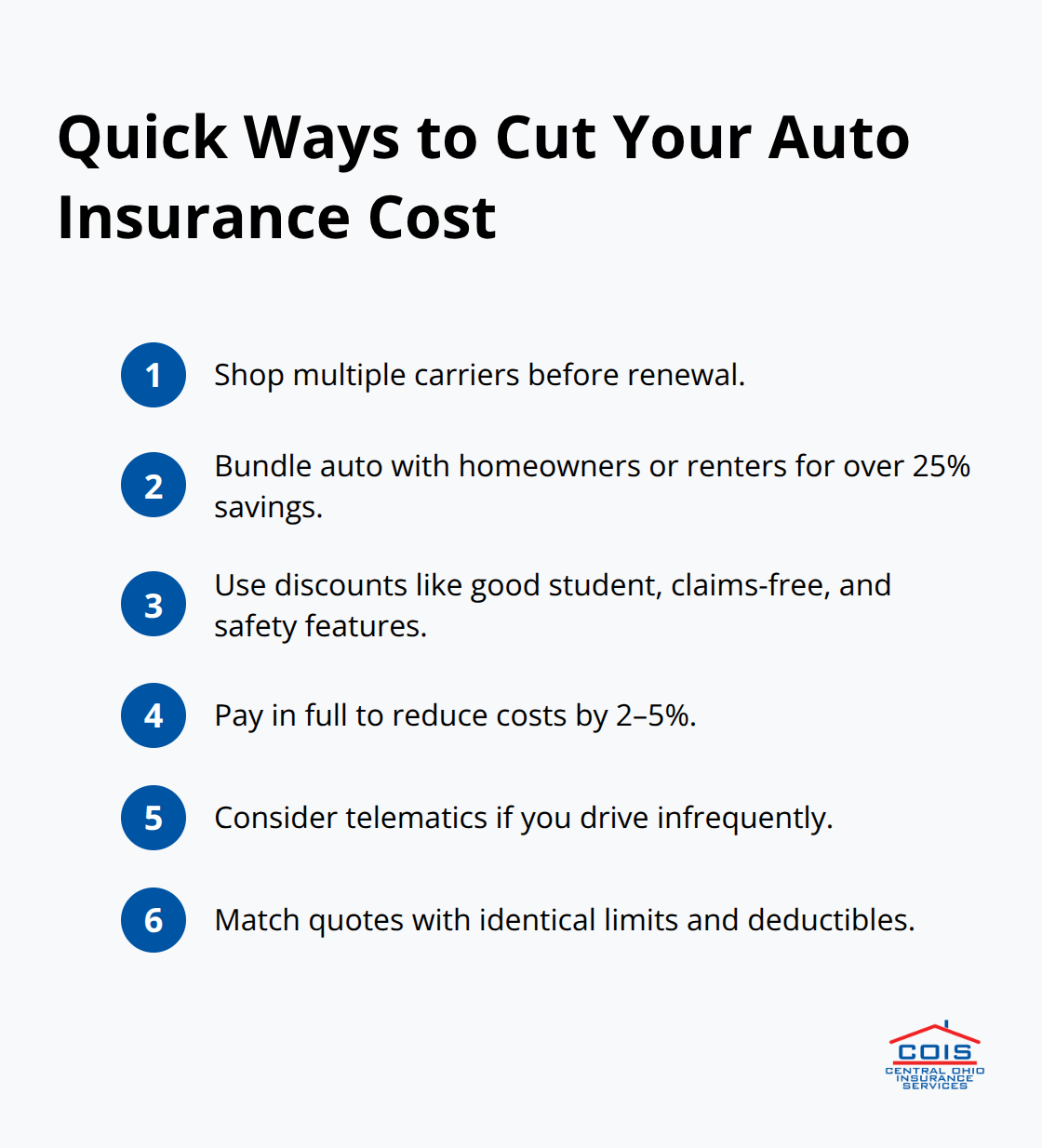

Discounts and Shopping Strategies Cut Costs Dramatically

Shopping multiple carriers reveals rate differences that can exceed $1,000 annually for identical coverage. Bundling your auto policy with homeowners or renters insurance saves over 25 percent on auto coverage nationwide, a discount that online quote tools frequently miss. Good student discounts, claims-free discounts, safety feature discounts, and professional association discounts each reduce your premium by 5 to 15 percent depending on the carrier. Paying your annual premium in full instead of splitting payments into monthly installments sometimes reduces your overall cost by 2 to 5 percent.

Telematics programs that monitor your driving habits benefit low-mileage drivers or those willing to share data for potential savings.

Compare Quotes Across Multiple Carriers Before Renewal

The key to finding affordable rates involves obtaining quotes from at least three different carriers before your policy renews. Compare identical coverage limits and deductibles across each quote, then review which discounts each carrier applies to your specific situation. Rate shopping takes roughly 30 minutes online or by phone, and the savings typically exceed $500 to $800 annually for Central Ohio drivers who take the time to compare. An independent agency like Central Ohio Insurance Services, Inc. handles this comparison work on your behalf, shopping multiple carriers to find competitive rates without locking you into a single company’s pricing structure.

Final Thoughts

Central Ohio car insurance works best when you partner with an agent who understands your region’s specific risks and shops multiple carriers on your behalf. National carriers treat Central Ohio as a data point in a spreadsheet, but local independent agents treat it as home. We at Central Ohio Insurance Services, Inc. operate from Pickerington with licensed staff who know the roads you drive, the weather patterns that affect your vehicle, and the carriers that offer competitive rates in your ZIP code.

Your coverage decisions matter more than your premium alone-carrying minimum liability limits leaves your personal assets exposed when accidents happen, and collision or comprehensive coverage protects your vehicle investment in a region where urban density drives claim frequency higher than statewide averages. Shopping multiple carriers before renewal saves most Central Ohio drivers $500 to $800 annually, yet most drivers renew without comparing options. Bundling auto with homeowners insurance adds another 25 percent savings opportunity that online quote systems frequently miss.

Start your quote today by contacting Central Ohio Insurance Services, Inc. or calling 614-861-3100. Our team in Pickerington handles the comparison work across multiple carriers so you see actual rates side by side. Your vehicle deserves protection built for Central Ohio’s driving environment, not generic national coverage.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.