Picking the right auto insurance in Ohio means understanding what coverage you actually need versus what’s just nice to have. We at Central Ohio Insurance Services, Inc. help drivers cut through the confusion by matching policies to real driving situations.

Your vehicle’s age, how often you drive, and your budget all play a role in finding the best Ohio auto coverage options for you. This guide walks you through the choices so you can make a decision that protects both your wallet and your car.

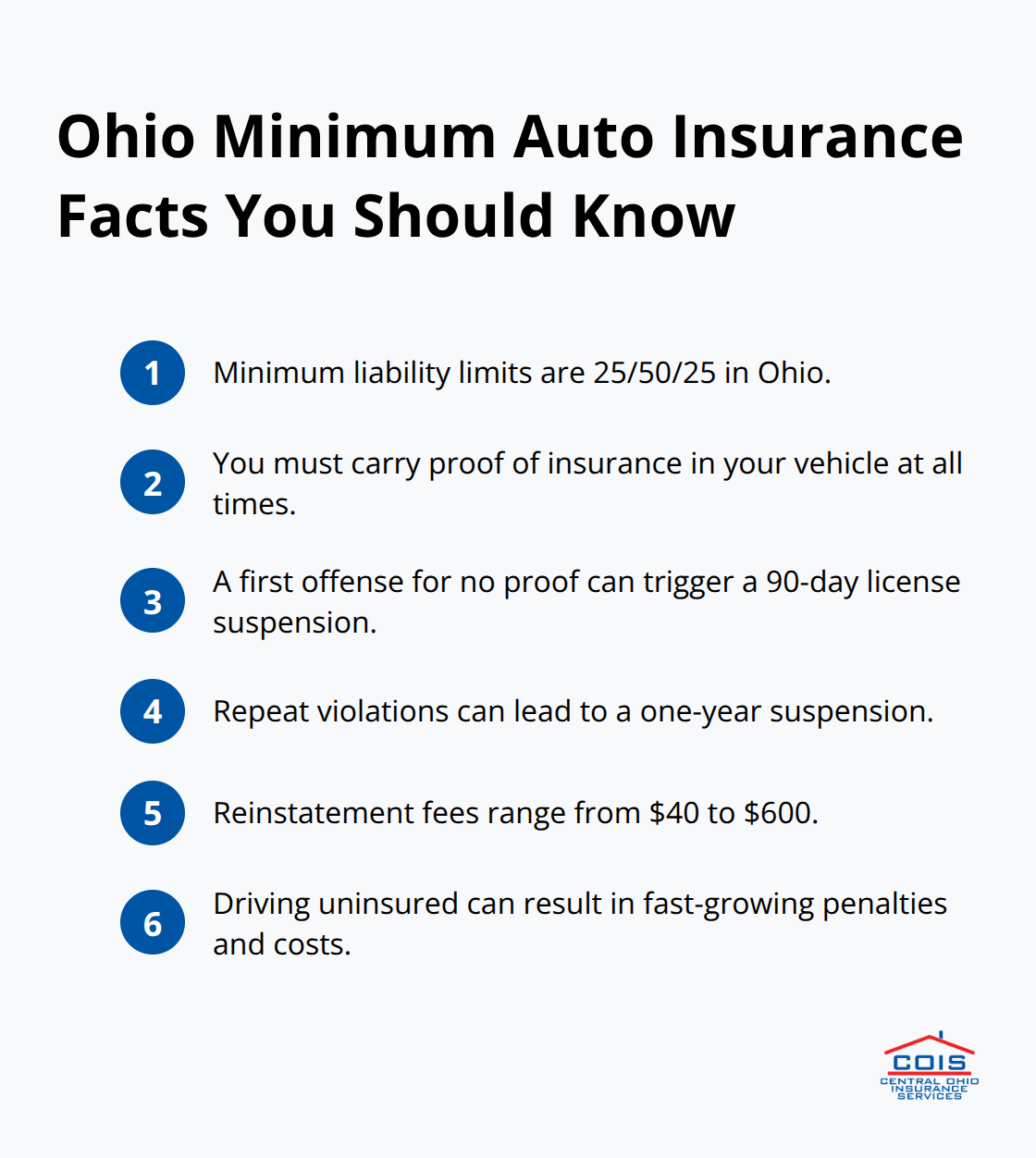

Ohio’s Minimum Coverage Requirements and Why They Fall Short

State-Mandated Liability Limits

Ohio law requires every driver to carry liability insurance with minimum limits of $25,000 per person for bodily injury, $50,000 per accident for bodily injury across all injured parties, and $25,000 per accident for property damage. Ohio Revised Code 4507.212 and 4509.101 establish these requirements, and you must carry proof of coverage in your vehicle at all times. If police stop you or you’re involved in an accident, you’ll need to show your insurance ID card or face penalties including license suspension for 90 days on a first offense, jumping to one year on repeat violations, plus reinstatement fees ranging from $40 to $600 depending on how many times you’ve been caught driving uninsured.

The reality is that these minimums are dangerously low. A single serious crash can generate medical bills, lost wages, and property damage well beyond $25,000 per person, leaving you personally liable for the difference. We at Central Ohio Insurance Services, Inc. strongly recommend increasing your liability limits to at least $100,000 per person and $300,000 per accident, especially if you have meaningful assets to protect. The cost difference between minimum and higher limits is surprisingly small-often just $10 to $20 per month-yet the protection gap is enormous.

The Uninsured Driver Problem in Ohio

About 15% of Ohio drivers carry no insurance at all, according to the Ohio Department of Insurance, and underinsured drivers are even more common in certain areas. If an uninsured or underinsured driver causes your accident, uninsured motorist coverage pays your medical bills and vehicle repairs up to your selected limit, while underinsured motorist coverage kicks in when the at-fault driver’s liability limits don’t cover your full damages. Without these protections, you’d have to sue the other driver personally or absorb the costs yourself.

Uninsured motorist property damage coverage is a separate optional add-on that specifically covers damage to your vehicle when hit by an uninsured driver. Many drivers skip this coverage thinking they’ll never encounter an uninsured motorist, but the statistics prove otherwise. Ohio’s fault-based system means the at-fault driver’s insurance pays, but only if they carry coverage-and roughly one in seven Ohio drivers don’t. Adding uninsured motorist coverage at your liability limits costs very little and protects you from a financial catastrophe when someone else breaks the law.

Moving Beyond the Bare Minimum

The gap between what Ohio requires and what actually protects you financially is substantial. Your next decision involves choosing what additional coverages make sense for your specific vehicle and driving situation.

What Coverage Actually Protects Your Vehicle and Health

Collision and Comprehensive Coverage for Your Vehicle

Collision and comprehensive coverage protect your vehicle when you cause an accident or when events outside your control strike. Collision pays for damage from crashes with other vehicles or objects, while comprehensive coverage covers theft, weather, wildlife, and vandalism. If you finance or lease your vehicle, your lender requires both coverages, and for good reason. In Ohio, comprehensive coverage costs approximately $1,811 annually according to February 2026 data. If your car is worth less than $5,000, dropping these coverages might make financial sense, but for anything newer or with a loan balance, skipping them exposes you to serious financial risk. A single hail storm, fender bender, or theft can cost thousands to repair or replace, far exceeding what you’d save in premiums over several years.

Medical Payments Coverage: Immediate Protection After an Accident

Medical payments coverage is where many Ohio drivers make a critical mistake by skipping it entirely. MedPay pays medical expenses for you and your passengers after an accident, regardless of who caused the crash, and it doesn’t count against your health insurance or deductible. Adding $5,000 in MedPay coverage typically costs $10 to $20 per month and covers ambulance rides, hospital stays, surgery, and rehabilitation. Unlike health insurance, MedPay doesn’t ask questions about fault or require you to pursue a liability claim first. If you or a passenger faces unexpected medical costs after an accident, MedPay steps in immediately without delays or bureaucratic hurdles.

Uninsured Motorist Bodily Injury: Protection When the Other Driver Lacks Coverage

Uninsured motorist bodily injury coverage operates differently and protects you specifically when an uninsured or underinsured driver causes your injury. This coverage pays your medical bills, lost wages, and pain and suffering up to your selected limit when the at-fault driver lacks sufficient insurance. Setting your uninsured motorist limits equal to your liability limits (for example, $100,000 per person and $300,000 per accident) ensures consistent protection across your policy. The cost difference between $50,000 and $300,000 in uninsured motorist coverage is minimal, yet the financial security difference is enormous.

Your vehicle’s age and current loan balance heavily influence which of these coverages you actually need versus which ones represent unnecessary expense.

How Much Coverage Do You Actually Need?

Start with what you owe versus what your vehicle is worth. If you financed or leased your car, your lender already made the decision for you: comprehensive and collision coverage are mandatory, typically with liability limits of at least 100/300/50 (meaning $100,000 bodily injury per person, $300,000 per accident, and $50,000 property damage). For owned vehicles without a loan, the calculation becomes personal. A car worth $3,000 doesn’t justify paying $150 monthly for collision and comprehensive coverage when those premiums total $1,800 annually. However, a vehicle worth $25,000 absolutely warrants full coverage because a single accident could cost $8,000 to $15,000 in repairs, wiping out years of premium savings. The real threshold sits around $5,000 in vehicle value; below that, dropping physical damage coverage often makes mathematical sense, but above it, the risk exposure grows too large to ignore.

How Your Driving Patterns Shape Coverage Needs

Your actual driving patterns matter far more than where you live or how old you are. A driver who commutes 45 minutes each way on interstate highways faces different risk than someone who drives two miles to a local office three days per week. High-mileage drivers accumulate more accident exposure, making collision and comprehensive coverage essential. Conversely, if you drive fewer than 5,000 miles annually and mostly on local roads, your accident probability drops significantly, though uninsured motorist coverage remains critical since that risk doesn’t decline with mileage. Your driving history also directly impacts what coverage makes sense; a clean record over five years suggests you can comfortably choose a $1,000 deductible to lower premiums, while multiple at-fault accidents in the past three years mean a $500 deductible offers better protection despite higher monthly costs. The Ohio Department of Insurance data shows that drivers with one accident in the past three years pay approximately 15% more in premiums, while those with two accidents face roughly 40% increases, making loss prevention through defensive driving more valuable than trying to save money on deductibles.

Your Actual Asset Protection Needs

Consider what you own beyond your car when setting liability limits. If you rent an apartment and have minimal savings, the state minimum of 25/50/25 might technically be acceptable since creditors struggle to garnish wages or seize rental housing. However, if you own a home worth $300,000, have a retirement account, or earn $75,000 annually, you absolutely need liability limits of at least 100/300/50 because a serious accident could trigger a judgment that follows you for years. A $500,000 judgment against someone with $25,000 in coverage leaves a $475,000 gap that creditors can pursue through wage garnishment for years. Try matching your liability limits to your total net worth plus three years of income; that calculation protects you from losing everything in a catastrophic accident. The cost difference between minimum and adequate limits runs $15 to $25 monthly for most drivers, making this the easiest financial decision in auto insurance.

Medical Payments Coverage for Your Household

Medical payments coverage reveals where many Ohio drivers make expensive mistakes through oversimplification. Some skip it entirely, assuming their health insurance covers accident injuries, while others purchase excessive amounts, thinking it provides duplicate protection. The practical answer depends on your household’s health insurance deductible and whether you have passengers regularly. If your health insurance deductible sits at $2,500 and you frequently drive friends or family, carrying $10,000 in MedPay coverage costs roughly $12 monthly and creates a safety net that covers that deductible immediately after an accident without waiting for insurance claims to process. If you’re uninsured or have a high-deductible health plan, MedPay becomes genuinely valuable. If you have comprehensive health coverage with a $500 deductible and rarely carry passengers, $2,500 in MedPay coverage serves your needs adequately at minimal cost. The mistake comes from either extreme: skipping it entirely or treating it as unnecessary because you have health insurance.

Final Thoughts

Your Ohio auto coverage options should match your actual driving situation, not generic recommendations or outdated assumptions. The coverage that protects a driver commuting 50 miles daily on busy highways differs significantly from someone driving locally a few times weekly, and a financed vehicle with a $25,000 loan balance requires different protection than an owned car worth $4,000. The gap between state minimums and adequate protection isn’t theoretical-it’s the difference between a manageable accident and financial devastation that follows you for years through wage garnishment and asset seizure.

Working with a local insurance agent transforms this process from overwhelming to straightforward. An agent reviews your specific vehicle, driving patterns, household composition, and financial situation to recommend coverage that actually matches your life rather than pushing you toward either excessive coverage you don’t need or dangerous gaps that expose you to catastrophic loss. We at Central Ohio Insurance Services, Inc. shop multiple carriers to find competitive pricing on the exact coverage combination that fits your needs, then provide ongoing support when you need to file a claim or adjust your policy as your situation changes.

Gather your current policy documents and contact Central Ohio Insurance Services, Inc. for a comprehensive review. Bring information about your vehicle, your annual mileage, and any recent accidents or violations, and a licensed agent will walk through each coverage type and show you exactly what different deductible and limit combinations cost. Many drivers discover they’re either overpaying for unnecessary coverage or carrying dangerous gaps they didn’t realize existed.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.