A motorcycle accident in Columbus can wipe out your savings fast. Medical bills, vehicle repairs, and legal fees add up quickly when you’re liable for injuries or damage.

At Central Ohio Insurance Services, Inc., we help riders understand exactly how much Columbus motorcycle liability insurance they need. The right coverage protects your assets and gives you real peace of mind on the road.

Why Motorcycle Liability Coverage Matters in Columbus

Ohio’s Legal Requirements

Ohio law requires every motorcycle rider to carry liability insurance before hitting the road. The state minimum is $25,000 per person for bodily injury, $50,000 per accident for bodily injury, and $25,000 for property damage. Ohio Revised Code sections 4507.212 and 4509.101 establish these thresholds, and you must show proof at traffic stops, accident scenes, and vehicle inspections. An insurance ID card on your phone or in your wallet satisfies this requirement. However, these minimums reflect what Ohio lawmakers deemed necessary-not what actual accident costs demand in Columbus.

What Real Accidents Cost

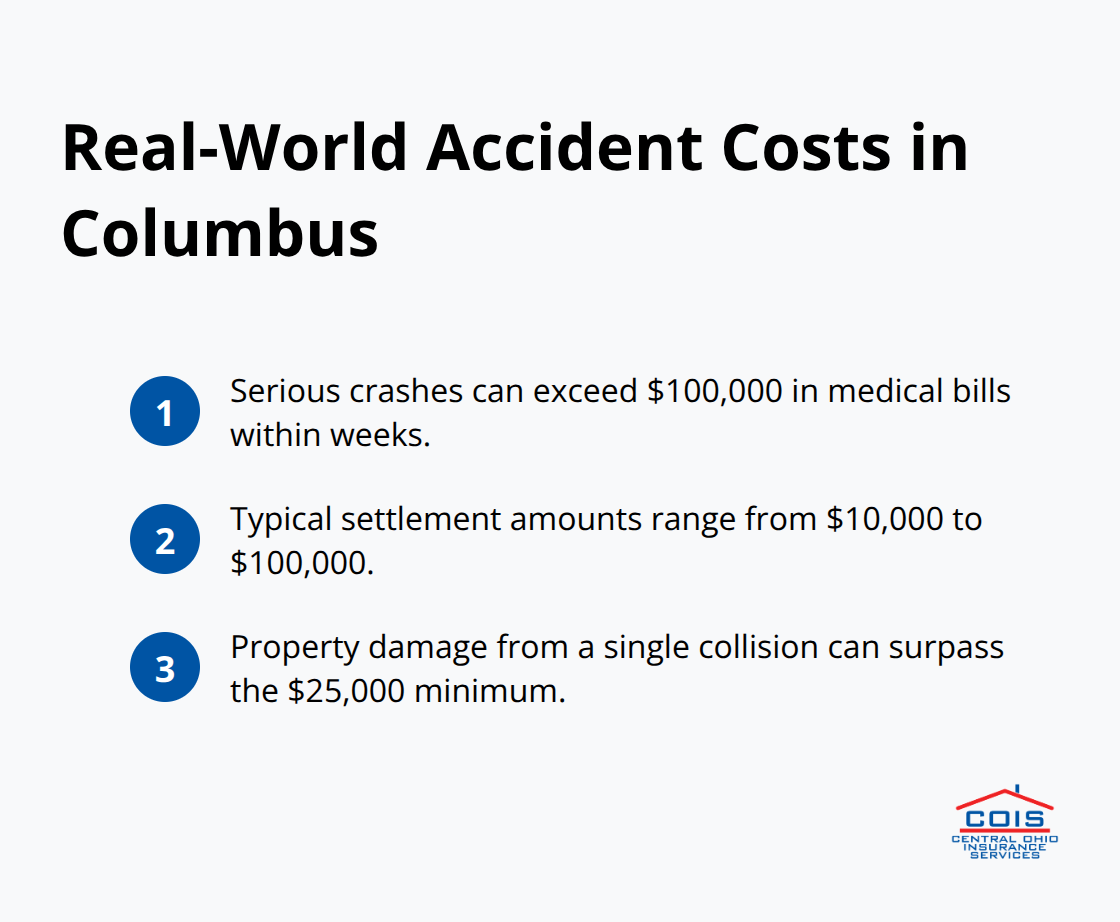

A single serious motorcycle crash generates medical bills exceeding $100,000 within weeks. If you’re liable for injuries to another rider or passenger, your personal assets become targets for judgment claims. Columbus motorcycle accident settlements typically range from $10,000 to $100,000 depending on injury severity and fault determination.

If you hit someone with only the state minimum bodily injury limit, you personally cover anything above that amount. Ohio’s comparative negligence law means you face liability even if you’re partially at fault, as long as the other party bears more responsibility. Property damage liability covers vehicle repairs, but a single collision with another motorcycle or car easily exceeds the minimum.

Why Minimums Leave You Exposed

MoneyGeek recommends carrying at least $50,000 per person and $100,000 per accident in bodily injury coverage, plus $25,000 property damage, to meaningfully protect your finances. Many lenders who finance motorcycles require even higher limits-typically $100,000 per person and $300,000 per accident-because they understand the gap between minimums and actual costs. These lenders recognize that state minimums create substantial financial risk for riders who own their bikes outright. Your coverage level directly determines how much of a judgment you pay from your own pocket. The difference between state minimums and adequate coverage often means the difference between protecting your home and losing it.

Finding Your Right Coverage Level

Your specific risk factors shape how much liability coverage you actually need. Factors like your riding frequency, the roads you travel, your experience level, and local traffic patterns all influence your decision. Central Ohio Insurance Services, Inc. helps Columbus riders assess these factors and recommend coverage levels that match their financial situation rather than settling for state minimums that leave them exposed. The next section explains how liability limits work in real claims scenarios so you can make an informed choice.

Understanding Liability Limits and What They Cover

Bodily Injury Liability Per Person

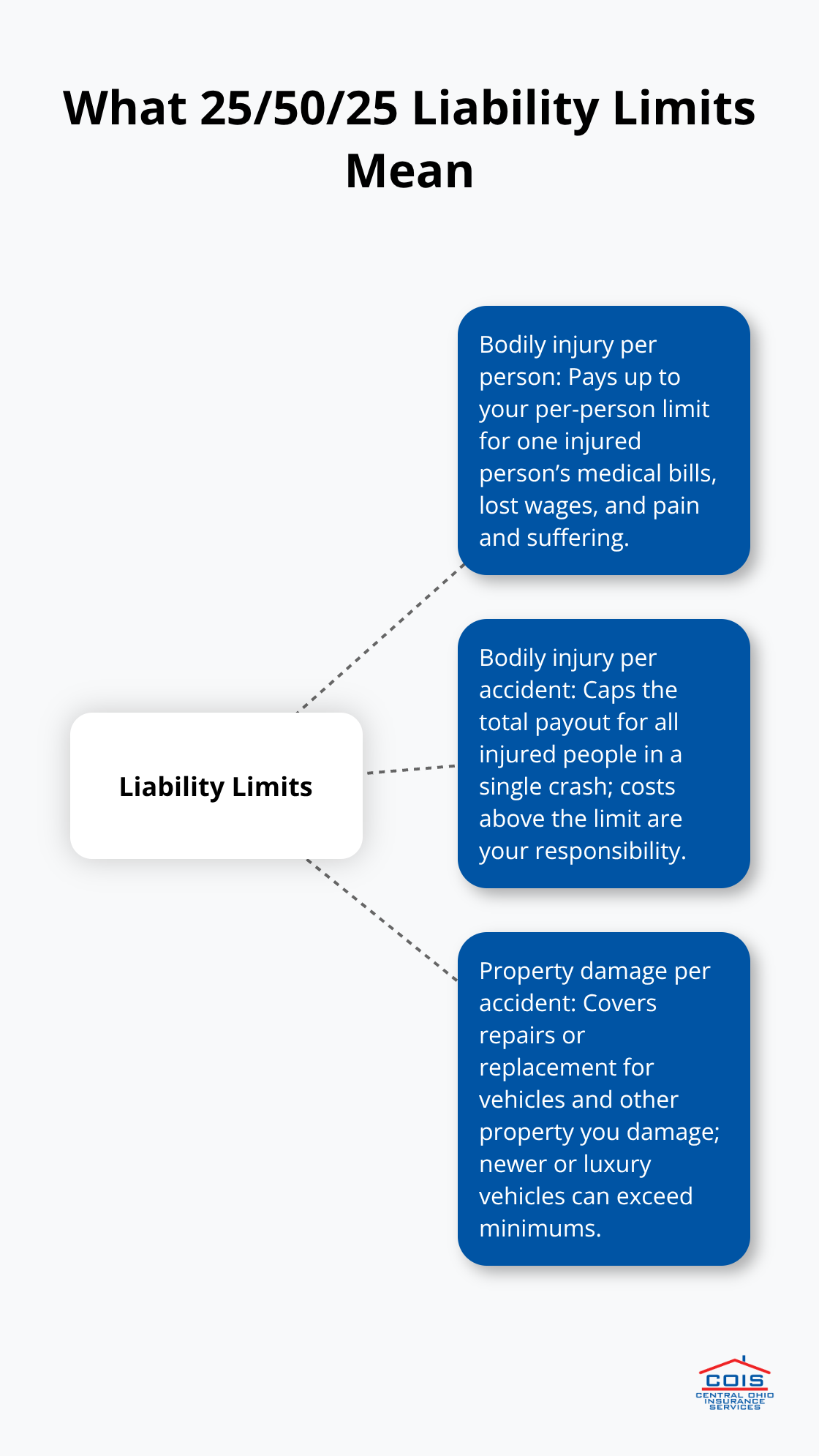

Liability limits appear as three numbers on your policy: bodily injury per person, bodily injury per accident, and property damage per accident. Ohio’s $25,000/$50,000/$25,000 minimum liability limits represent the state’s minimum requirements, but these numbers mean nothing until you understand what happens when you cause an accident. Your bodily injury limit per person caps what your insurer pays for one injured person’s medical bills, lost wages, and pain and suffering. If that person’s damages exceed your limit, you personally pay the difference from your bank account or through wage garnishment.

Bodily Injury Per Accident and Property Damage

The per-accident limit represents your total bodily injury payout across all injured parties in a single crash. If you hit two riders and rack up $80,000 in combined medical costs, your $50,000 per-accident limit covers only part of it, leaving you responsible for the $30,000 gap. Property damage liability works the same way but covers vehicle repairs and other property harm. A collision with a newer motorcycle or luxury car easily generates $30,000 to $50,000 in damage, and your $25,000 minimum leaves significant exposure.

How Real Claims Scenarios Expose Thin Minimums

A moderate motorcycle crash with one serious injury typically generates $40,000 to $60,000 in medical expenses within the first year alone. If you carry only Ohio’s $25,000 per-person limit, your insurer pays $25,000 and you owe $15,000 to $35,000 out of pocket. Courts in Ohio allow injured parties to pursue judgments against you personally, meaning creditors can garnish your wages for years. Lenders financing motorcycles require higher limits specifically because they know state minimums fail to protect borrowers.

Why Adequate Coverage Matters More Than Minimums

Industry experts recommend increasing your liability limits to at least $100,000 per person and $300,000 per accident, which reflects what actual accident costs demand in today’s market. Your choice between minimums and adequate coverage isn’t theoretical-it determines whether a single accident drains your savings or leaves your finances intact. Columbus motorcycle accident settlements typically range from $10,000 to $100,000 depending on injury severity and fault determination. The gap between what Ohio requires and what accidents actually cost creates substantial financial risk for riders who settle for state minimums.

Choosing Coverage That Protects Your Assets

Your specific risk factors shape how much liability coverage you actually need. Factors like your riding frequency, the roads you travel, your experience level, and local traffic patterns all influence your decision. A local independent insurance agency can help you assess these factors and recommend coverage levels that match your financial situation rather than settling for state minimums that leave you exposed. For protection beyond your motorcycle policy limits, consider exploring umbrella insurance as an additional layer of liability protection.

Finding Your Right Coverage Level

Your riding habits and financial exposure determine how much liability coverage actually protects you. A Columbus rider who commutes five days a week on busy streets faces different risks than someone who rides recreationally on weekends, and your coverage should reflect that reality. Riding frequency increases accident probability-more time on the road means higher exposure. The roads you travel matter too; downtown Columbus traffic and highway riding create different hazard profiles. Your experience level and riding history influence risk substantially. A rider with ten years of clean riding creates less exposure than someone new to motorcycles. Local traffic patterns in Columbus shape your needs, particularly during rush hours on I-270 and I-71 where motorcycle accidents tend to cluster. Your financial situation matters most of all. If you own a home, have savings, or earn a solid income, state minimums leave your assets vulnerable to judgment claims. If you finance your motorcycle, your lender already made this decision for you (typically requiring 100/300/100 coverage). These aren’t theoretical considerations-they directly determine how much of an accident judgment you pay personally versus your insurer.

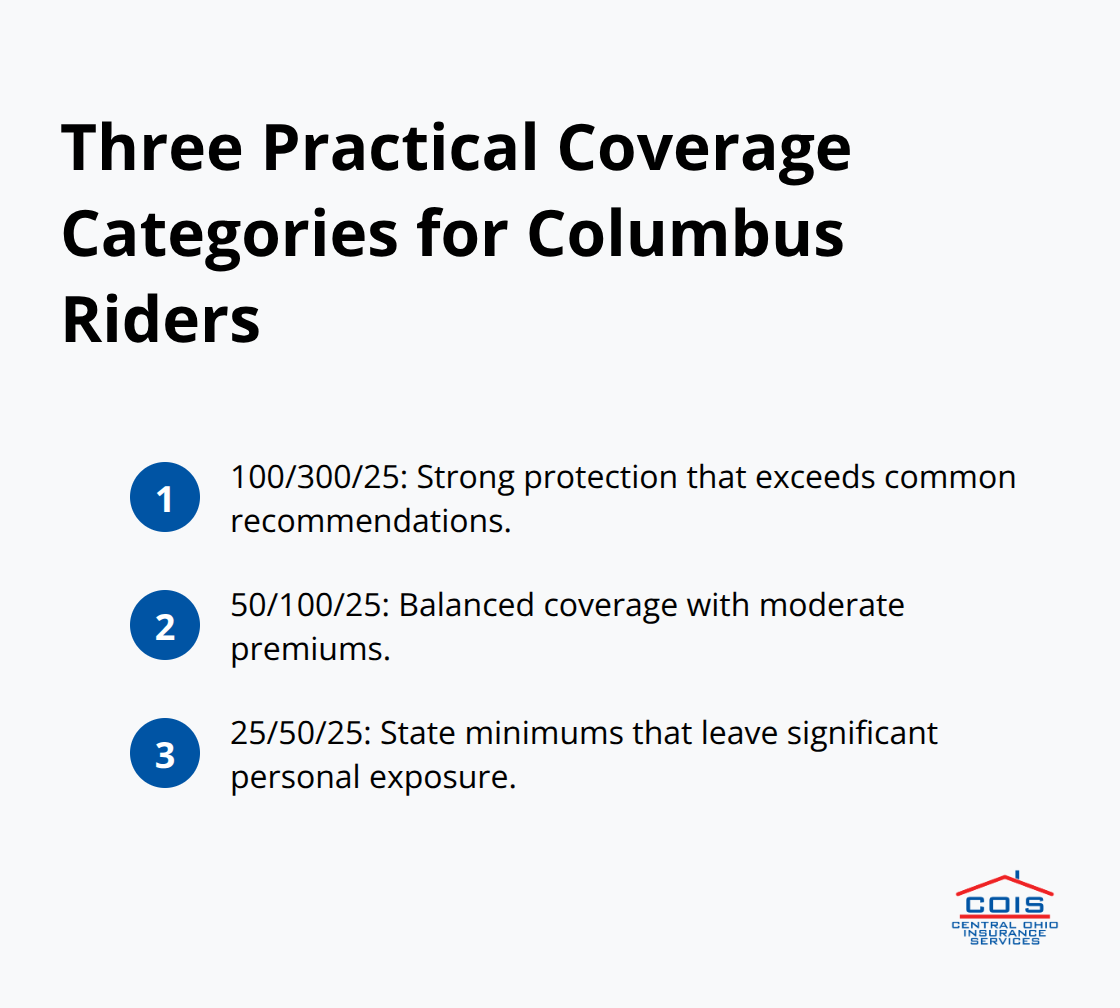

Three Practical Coverage Categories

Most riders fall into one of three practical categories. Conservative riders who want genuine protection carry 100/300/25 limits, which exceeds what MoneyGeek recommends as adequate coverage and protects most Columbus accident scenarios. Mid-range riders often choose 50/100/25 coverage, balancing reasonable protection against moderate premium costs.

Riders with minimal assets sometimes accept state minimums at 25/50/25, though this approach creates substantial personal liability exposure.

The Real Cost Difference

The cost difference between these options remains relatively small. The average annual liability-only motorcycle policy in Ohio costs around $169 according to Ratefilings.com data, and stepping up to better coverage typically adds only $20 to $40 annually. That modest increase buys protection worth thousands in a real accident. A licensed insurance agent can help you compare these options and find coverage that fits your budget without sacrificing protection.

Questions That Reveal Your Actual Needs

Before selecting your coverage, ask yourself whether you could personally pay a $50,000 judgment if a serious accident happened today. If the answer is no, your state minimums aren’t adequate. Ask whether your income could withstand wage garnishment for years following a judgment. Ask what assets you’d lose if someone sued you successfully (your home, savings, vehicle, or future earnings). These questions reveal your actual coverage needs better than any formula.

Final Thoughts

Columbus motorcycle liability insurance protects your financial future far more than your bike. A single serious crash generates medical bills and property damage exceeding $100,000, leaving you personally responsible for anything above your policy limits. The gap between Ohio’s $25,000 state minimum and what actual accidents cost creates real risk for riders who settle for inadequate coverage.

Your specific situation determines the right coverage level-riding frequency, the roads you travel, your experience, and your financial assets all shape how much protection you actually need. Most riders discover that stepping up from state minimums to adequate coverage costs only $20 to $40 more annually, a modest investment for genuine protection. A licensed insurance agent can help you assess your specific risk factors and recommend coverage that matches your financial situation rather than settling for minimums that create exposure.

Central Ohio Insurance Services, Inc. helps Columbus riders navigate these decisions with clear guidance and competitive quotes from multiple carriers. Contact them today to secure coverage that gives you genuine peace of mind on Columbus roads.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.