Classic car liability coverage protects you when you’re at fault for an accident-but many owners don’t realize their standard auto policy won’t cut it. At Central Ohio Insurance Services, Inc., we’ve seen too many classic car enthusiasts underinsured because they didn’t understand how liability works differently for vintage vehicles.

Your classic car’s high replacement value means higher financial exposure. That’s why choosing the right liability limits matters more than most people think.

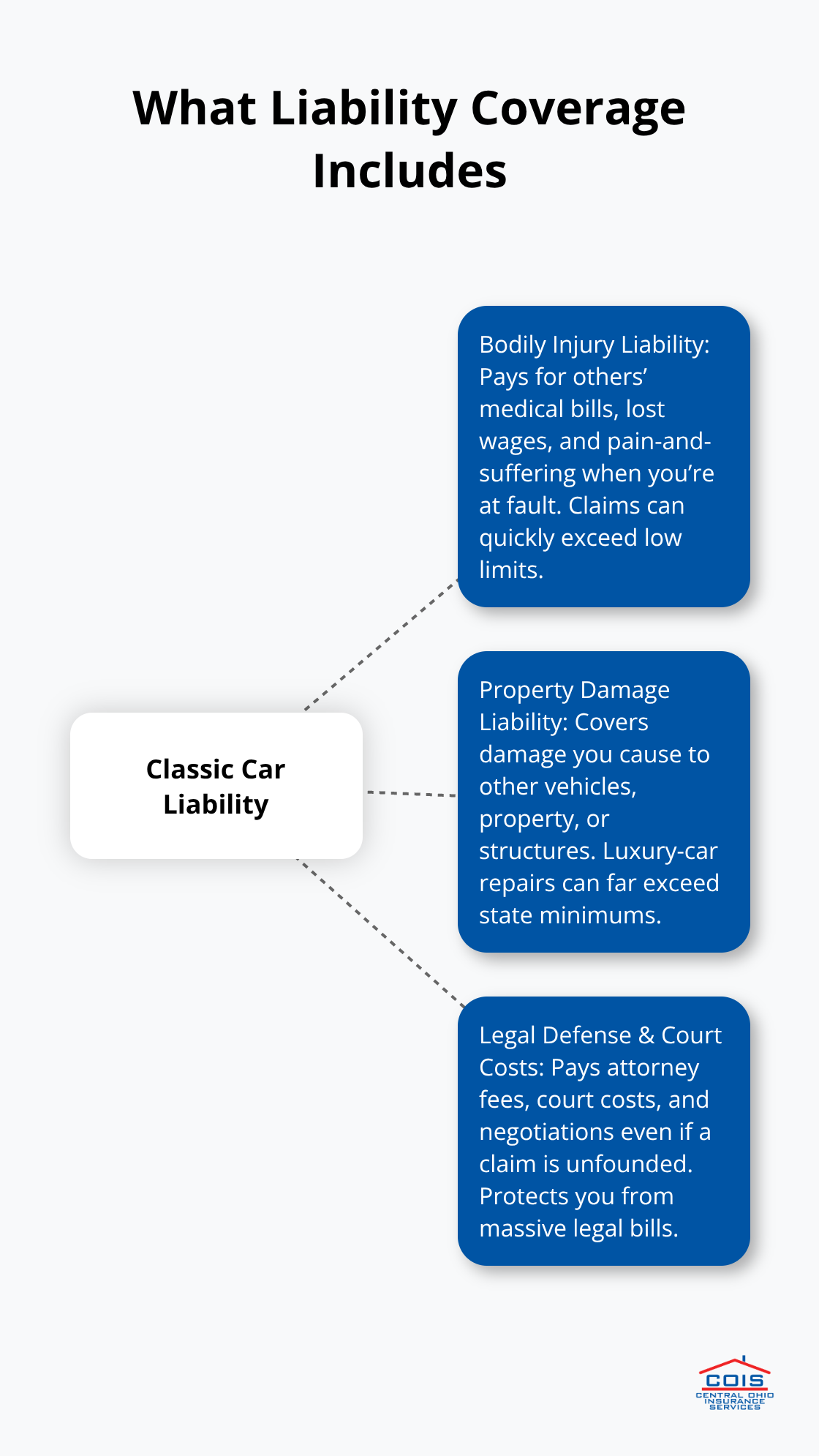

What Your Liability Coverage Actually Pays For

Bodily Injury Liability: The Biggest Expense

Bodily injury liability covers medical expenses, lost wages, and pain-and-suffering claims for anyone injured in a crash you cause. This is where claims get expensive fast. A serious injury can result in medical costs that exceed typical coverage limits, and if the injured person sues, you become responsible for everything above your coverage limits. The injured party’s attorney will pursue maximum compensation, which means your liability protection needs to match the financial exposure your classic car creates.

Property Damage Liability: Protecting Others’ Assets

Property damage liability handles damage to someone else’s vehicle, property, or structures-think hitting a parked car or crashing into a fence. Most states require minimum liability coverage, typically $15,000 for bodily injury per person and $30,000 per accident, plus $5,000 for property damage, according to the National Association of Insurance Commissioners. However, these minimums are dangerously low for classic car owners. If your 1967 Mustang hits a newer luxury vehicle worth $80,000, your state minimum property damage coverage won’t come close to covering the damage.

Legal Defense and Court Costs: Protection You Can’t Ignore

Legal defense and court costs represent a third protection that many owners overlook entirely. If someone sues you after an accident, your liability policy covers the cost of your legal defense-attorney fees, court costs, and settlement negotiations. This protection applies even if the claim turns out to be invalid or exaggerated. Without it, you could spend $50,000 defending yourself in court before your insurer pays a single dollar toward the claim itself.

Recommended Coverage Limits for Classic Car Owners

For classic car owners, we recommend liability limits of at least $250,000 per person and $500,000 per accident, with $100,000 in property damage coverage. This elevated protection matches the financial exposure your valuable classic car creates. If your net worth exceeds $500,000, adding an umbrella policy with $1,000,000 in additional coverage provides serious protection against catastrophic claims. The cost difference between minimum coverage and adequate coverage is often just $30 to $50 annually, making it one of the smartest investments you can make for your classic car collection.

Understanding these liability components sets the foundation for selecting appropriate coverage limits-a decision that depends heavily on your personal financial situation and how frequently you drive your classic car.

Why Your Standard Auto Policy Won’t Protect Your Classic Car

Standard auto insurance policies are built for daily drivers that depreciate predictably. Insurers price these policies assuming your vehicle loses value each year, so they use actual cash value to settle claims. This approach fails spectacularly for classic cars because your 1967 Chevelle or 1955 Thunderbird likely appreciates instead of depreciates. When you file a total-loss claim under a standard policy, the insurer calculates what your car was worth at the moment of loss-often far below what you paid or what it’s actually worth in the collector market. An insurer might total your classic car and offer you $35,000 when you know it’s worth $85,000. Standard policies also routinely exclude vehicles over 25 years old or impose strict mileage limits that contradict how most classic car owners actually use their vehicles. Your standard auto policy probably won’t cover your car if you drive it to a car show 200 miles away, participate in a local cruise night, or take it on a weekend road trip with your car club.

The Real Cost of Underinsurance

The financial exposure from underinsurance extends far beyond the vehicle itself. If you’re at fault in an accident with inadequate liability coverage, you personally pay the difference between your coverage limits and the actual damages. A collision with a newer luxury vehicle can result in $100,000 in property damage alone. Your medical bills, lost wages, and pain-and-suffering claims from an injured party can reach $500,000 or more in serious cases. Standard policies typically cap liability at state minimums-often $15,000 to $25,000 per person according to the National Association of Insurance Commissioners-leaving you exposed to six figures in personal liability. Classic car owners with significant assets face even greater risk because injured parties’ attorneys specifically target high-net-worth defendants. A $50,000 net worth might justify state minimum coverage, but a $500,000 net worth creates exposure that demands $250,000 to $500,000 in liability protection.

Why Agreed Value Matters

Agreed value coverage eliminates the post-loss valuation dispute entirely. Instead of the insurer deciding your car’s worth after a claim, you and your insurer agree on a specific value upfront based on an appraisal, market data, and the car’s condition. If your classic car is totaled, you receive that agreed amount minus your deductible-no negotiation, no depreciation calculation, no surprises. A standard auto policy uses actual cash value, which means the insurer performs a valuation after the loss occurs and often pays significantly less than you expected. Agreed value policies also account for restorations, upgrades, and original parts that increase value beyond the original purchase price. If you’ve spent $30,000 restoring your classic truck, that investment gets recognized in the agreed value. You can adjust the agreed value annually to reflect changes in market prices, condition improvements, or additional work completed on the vehicle.

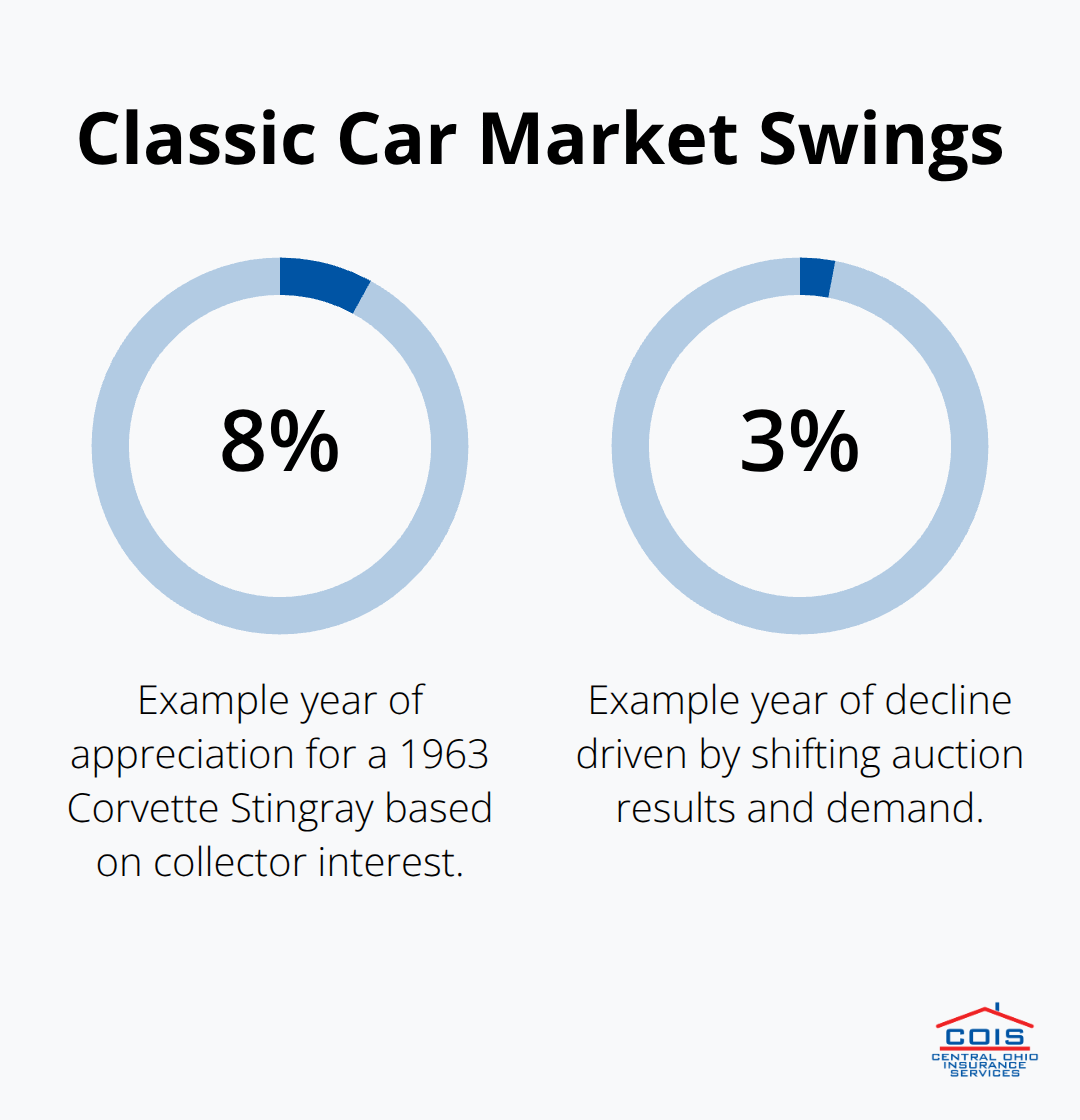

How Market Fluctuations Affect Your Coverage

Classic car values fluctuate based on market demand, condition, and historical significance-factors that standard valuations ignore. A 1963 Corvette Stingray might appreciate 8% one year and decline 3% the next, depending on collector interest and auction results. Agreed value coverage protects you from these market swings because your payout amount stays locked in, regardless of what the market does.

Standard policies leave you vulnerable to timing-if your car is totaled during a market downturn, you receive less than you would have during a peak. This certainty matters enormously when your classic car represents a significant portion of your personal assets. The next step involves selecting liability limits that match your financial situation and how you actually drive your classic car.

How to Match Your Liability Limits to Your Financial Situation

Calculate Coverage Based on Your Net Worth

Your net worth determines how much liability protection you actually need. If you have $150,000 in total assets, state minimum coverage around $15,000 to $25,000 per person creates manageable risk because an injured party can only pursue assets you own. But if you have $750,000 in net worth, that same minimum coverage leaves $725,000 exposed to a lawsuit. Courts don’t care about your insurance limits-they care about what you’re worth. An attorney representing someone seriously injured in your accident will research your home value, investment accounts, and business interests, then demand compensation that matches your ability to pay.

We recommend using this straightforward calculation: your liability limits should equal at least 50 percent of your net worth, with a minimum of $250,000 per person and $500,000 per accident for any classic car owner. If your net worth exceeds $500,000, adding an umbrella policy with $1,000,000 in coverage costs around $150 to $300 annually and protects everything you’ve built. Classic car owners with significant assets who skip this protection are essentially betting their financial future on never causing a serious accident.

Understand Your State’s Minimum Requirements

State minimum requirements create a legal floor, but they’re dangerously inadequate for classic car owners. Ohio requires $12,500 in bodily injury coverage per person and $25,000 per accident, plus $7,500 for property damage, according to the Ohio Department of Insurance. These minimums assume you’re driving a depreciating vehicle in daily traffic, not a collectible that creates outsized liability exposure.

Most states set minimums far below what classic car owners actually need. The National Association of Insurance Commissioners reports that state minimums typically range from $15,000 to $25,000 per person, which won’t cover serious injuries or damage to luxury vehicles. Your classic car’s value and your personal assets demand substantially higher protection than these legal minimums provide.

Adjust Coverage Based on Your Driving Patterns

Your driving frequency and usage patterns should directly influence your coverage selection. If you drive your classic car only to monthly car club meetings and two annual car shows, you create less risk than someone who drives theirs weekly to restaurants and social events, which might justify potentially lower limits-though nothing below $100,000 per person and $300,000 per accident makes sense. Conversely, if you participate in organized drives, parades, or weekend road trips across state lines, your exposure increases substantially because you’re on the road more often and potentially farther from home.

Document how many miles you actually drive annually and what activities you participate in, then discuss those specifics with an insurance professional who understands classic car exposure rather than accepting generic recommendations. An independent insurance agent can evaluate your actual usage and help you select limits that match your real-world driving patterns and financial situation.

Final Thoughts

Classic car liability coverage protects your personal assets and financial future far more than your vehicle itself. Standard auto policies fail classic car owners because they’re built for depreciating vehicles, not appreciating collectibles, and your liability limits must match both your net worth and your actual driving patterns rather than your state’s minimum requirements. A serious accident involving your classic car can expose you to six-figure liability claims that far exceed state minimums, and if you have significant assets, inadequate coverage essentially invites attorneys to pursue everything you own.

The gap between minimum coverage and appropriate coverage costs remarkably little-often just $30 to $50 annually-yet protects hundreds of thousands of dollars in personal wealth. Contact an insurance professional who understands classic car exposure rather than accepting generic recommendations from agents unfamiliar with collector vehicles. We at Central Ohio Insurance Services, Inc. specialize in specialty vehicle coverage and umbrella policies designed specifically for high-net-worth classic car owners, and our licensed team shops multiple carriers to deliver unbiased solutions tailored to your collection’s actual value and your driving patterns.

Review your current coverage annually, especially if you’ve completed restorations, added vehicles to your collection, or changed how frequently you drive your classics. Market values shift, your net worth changes, and your usage patterns evolve-your insurance should reflect that reality. Classic car liability coverage requires periodic attention to remain adequate as your circumstances change.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.