Your 1987 Corvette or 1965 Mustang isn’t just another car on the road. Standard auto insurance policies treat them like everyday vehicles, which means they’re drastically undervalued and poorly protected.

At Central Ohio Insurance Services, Inc., we understand that antique car insurance in Columbus requires specialized coverage designed specifically for collectors. This guide walks you through why your historic vehicle needs different protection than a regular car.

Why Your Antique Car Isn’t Like Your Daily Driver

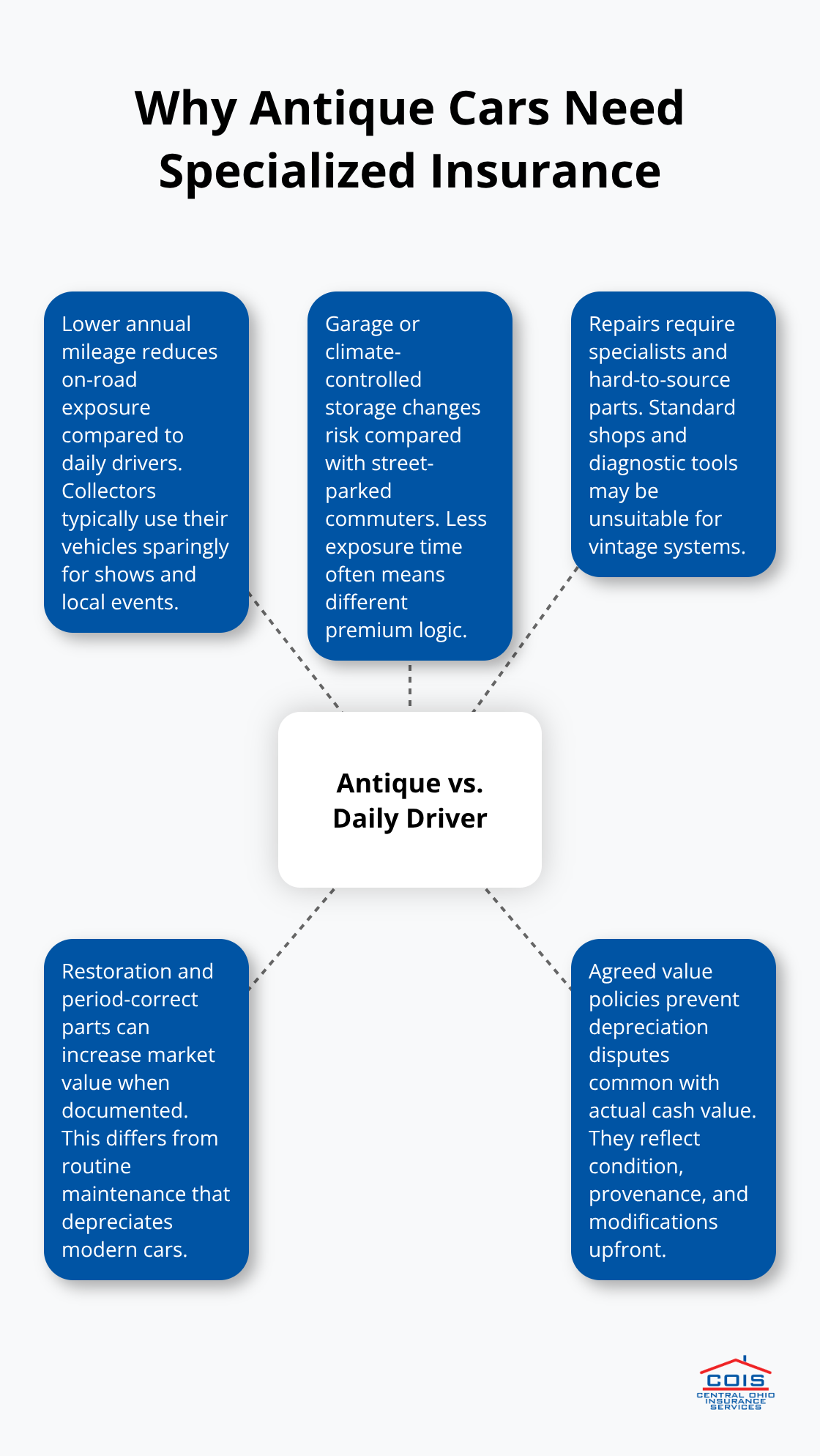

Antique cars operate under fundamentally different rules than modern vehicles. The average collector car in the United States travels fewer than 5,000 miles per year, according to classic car insurance industry standards.

Your 1987 Corvette might sit in a climate-controlled garage for months while your daily sedan racks up 12,000 to 15,000 miles annually. This dramatic difference in usage patterns means standard auto insurance pricing and coverage structures simply don’t fit. Insurance companies calculate premiums based on exposure risk, and a vehicle that rarely leaves the garage presents vastly different exposure than a car commuting five days a week.

Additionally, antique vehicles require specialized repair facilities. A 1965 Mustang needs technicians familiar with carburetor tuning and points-based ignition systems, not modern computerized diagnostics. Standard repair shops won’t stock the correct parts, and mechanics unfamiliar with vintage systems may cause more damage than they fix. The restoration work on an antique car also accumulates value differently than standard vehicle maintenance. Replacing original components with period-correct parts, restoring interior trim, or repainting to match factory specifications represents an investment that increases the vehicle’s market value, not a depreciation expense like brake pads on a 2024 sedan.

Age Determines Your Coverage Approach

Vehicles older than 25 to 30 years qualify as antiques or classics, but age alone doesn’t capture what makes them special. A 1963 Jaguar E-Type Roadster and a 1963 Ford Fairlane require entirely different coverage strategies despite their identical age. The Jaguar’s rarity and documented provenance mean its value appreciates with proper preservation, while the Fairlane might depreciate under standard valuation methods.

This is why agreed value coverage matters for antique cars. Unlike actual cash value policies that pay what the insurance company decides your car is worth at claim time, agreed value coverage pays the full amount you and your insurer establish upfront. You work with an appraiser to document the vehicle’s condition, history, and market value before any loss occurs. If a covered total loss happens, you receive that agreed amount minus your deductible, with no depreciation disputes. Agreed value coverage eliminates the frustration of an insurer offering $15,000 for a $28,000 antique car because they applied standard depreciation schedules designed for vehicles that lose 15 to 20 percent of value annually.

Modifications and Originality Change Everything

Most antique cars in private collections have some modifications or restoration work completed. These changes directly affect insurance coverage and valuation. A stock 1970 Dodge Charger and a 1970 Charger with a modern 500-horsepower engine conversion represent completely different risk profiles and values. Standard auto policies either exclude modified vehicles or charge rates designed for regular cars, missing the nuance entirely.

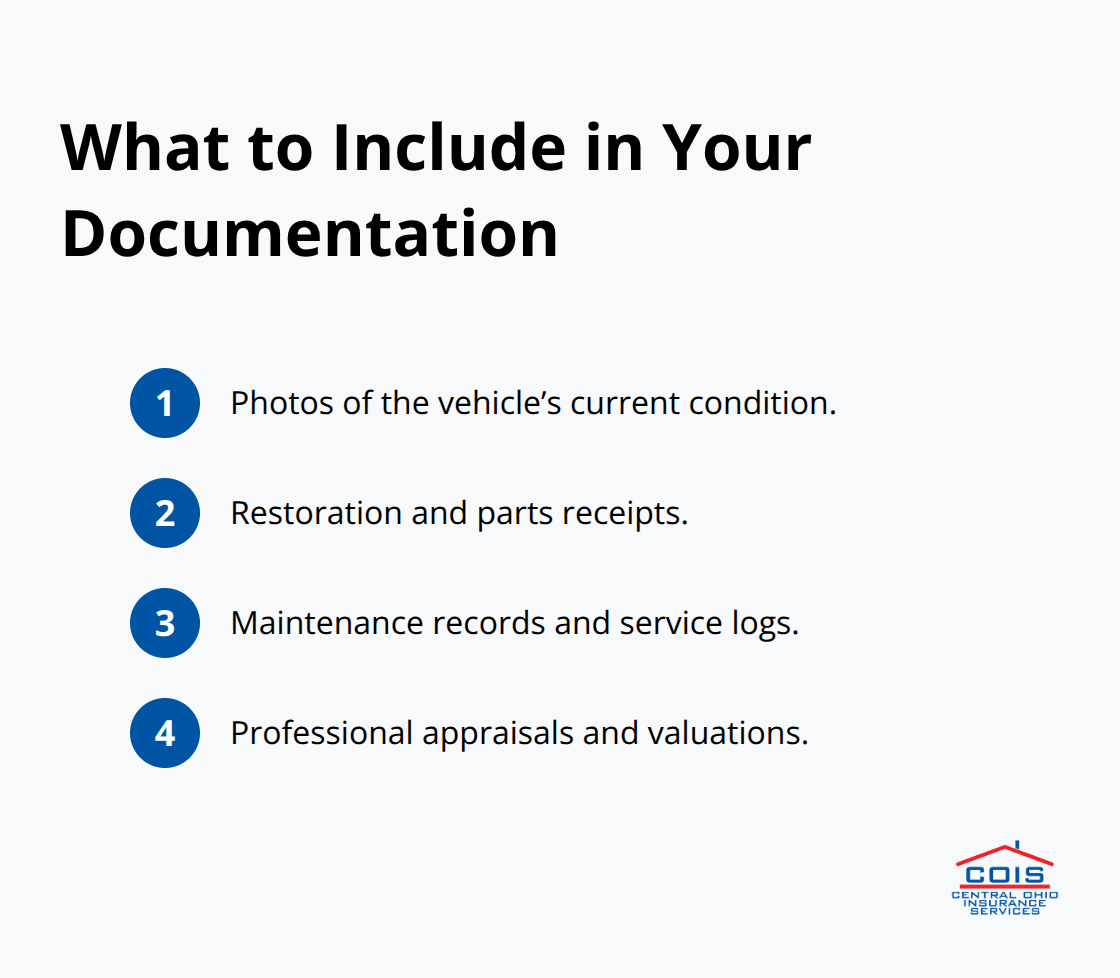

Specialty antique car insurance accounts for the specific modifications you’ve made. Whether you’ve upgraded the electrical system to modern standards, installed a newer transmission for reliability, or added custom upholstery, your policy should reflect these changes. Documentation proves invaluable here. You should keep receipts, before-and-after photos, and detailed records of any work performed to support both your agreed value appraisal and your insurance claim if something happens.

The Smithsonian Institution’s preservation philosophy emphasizes that a car is original only once, making careful documentation of what you change and why essential for protecting the vehicle’s long-term value and your insurance coverage accuracy. This attention to detail separates collectors who maintain their investment from those who watch their vehicle’s value slip away. As you prepare your antique car for proper coverage, the next step involves understanding which specific coverage options actually protect your collection.

Which Coverage Actually Protects Your Antique Car

Agreed value coverage insures your classic car for what you and your insurer agree it’s worth. This approach locks in your vehicle’s value before any loss occurs, eliminating the depreciation disputes that plague standard policies. When you insure a 1970 Dodge Charger with actual cash value coverage, the insurance company applies depreciation schedules designed for vehicles that lose thousands of dollars annually. A car worth $28,000 today might be valued at $15,000 at claim time simply because the insurer applied a 15 to 20 percent annual depreciation rate intended for modern vehicles. Agreed value coverage prevents this entirely. You work with an appraiser to document your antique car’s condition, history, modifications, and market value upfront. If a covered total loss occurs, you receive that agreed amount minus your deductible, with no negotiation or depreciation applied. This matters because antique cars often appreciate in value when properly maintained and preserved, not depreciate like daily drivers. Your documentation should include photos of the vehicle’s current condition, restoration receipts, maintenance records, and any appraisals completed. This documentation becomes your protection against undervaluation.

Comprehensive and Collision Coverage for Limited-Use Vehicles

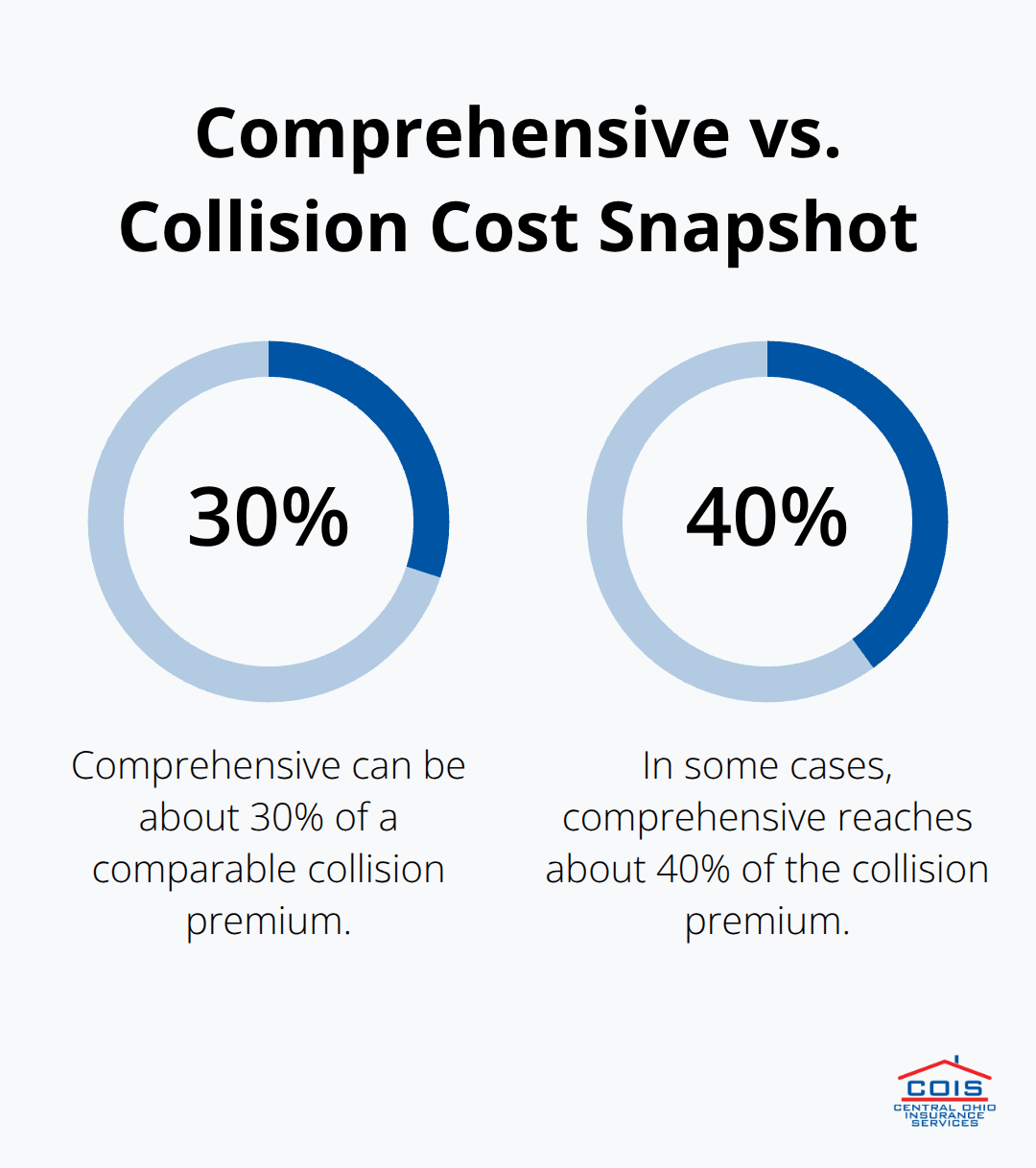

Comprehensive coverage protects against theft, vandalism, weather damage, and animal collisions, while collision coverage handles accidents with other vehicles or objects. For antique cars driven fewer than 5,000 miles annually, collision coverage presents a genuine question worth asking. If your 1987 Corvette spends most of its time in a climate-controlled garage and only travels to car shows or local events, the collision risk drops substantially compared to a daily driver. Many collectors choose comprehensive coverage without collision to reduce premiums while maintaining protection against the hazards their vehicles actually face. Weather damage, theft, and vandalism represent real risks for parked vehicles, particularly if stored in a standard garage rather than a secure facility. Collision coverage makes more sense if you regularly drive your antique car on public roads or attend events that require highway travel. The decision depends entirely on your actual usage patterns and risk tolerance. Comprehensive coverage typically costs significantly less than collision-sometimes 30 to 40 percent of the total collision premium-making it an efficient way to maintain meaningful protection without unnecessary expense.

Roadside Assistance and Spare Parts Coverage

Antique cars break down differently than modern vehicles, and standard roadside assistance often fails collectors. Your 1965 Mustang needs a flatbed tow to a specialist facility, not the nearest quick-lube shop with a standard tow truck. Quality antique car policies include flatbed towing specifically because vintage vehicles cannot be safely towed on two wheels without risking transmission and suspension damage. Spare parts coverage addresses another real collector need. Original components for older vehicles become increasingly scarce and expensive. If you maintain a collection of original parts for your restoration projects or keep extras for your primary vehicle, specialty policies can cover these items separately from the vehicle itself. This coverage applies whether those parts sit at home, in a garage, or travel to events. Transportation coverage becomes valuable if your antique car undergoes restoration and temporarily cannot be driven, or if you transport it to shows and events. This coverage pays for rental transportation while your vehicle is being repaired or is in transit, ensuring you maintain mobility without using your classic car for daily driving that would increase mileage and risk.

Building Your Coverage Strategy

The right combination of coverage depends on how you actually use your antique car. A show car that travels to three or four events annually requires different protection than a weekend driver that logs regular miles on local roads. Start by honestly assessing your vehicle’s annual mileage, storage conditions, and planned activities. An independent insurance agent can help you compare collector car insurance quotes from multiple carriers and identify which coverage options align with your specific situation and budget. This personalized approach ensures you pay for protection that matters while avoiding unnecessary coverage gaps.

Why Standard Policies Fail Antique Car Owners

Standard auto insurance companies built their pricing models around vehicles that depreciate predictably and get driven daily. A 2024 sedan loses 15 to 20 percent of its value annually according to industry depreciation schedules. Insurance companies apply these same depreciation rates to antique cars, which creates a fundamental mismatch. Your 1970 Dodge Charger worth $28,000 gets valued at $15,000 under actual cash value because the insurer applies depreciation intended for vehicles losing thousands monthly. This undervaluation happens automatically, and you learn about it only after a total loss occurs when negotiation becomes impossible. Agreed value coverage solves this problem entirely, but standard policies refuse to acknowledge that antique cars appreciate rather than depreciate. Additionally, standard policies impose mileage restrictions that don’t align with how collectors actually drive. Many policies penalize you for exceeding 15,000 miles annually, yet collectors typically drive under 5,000 miles per year according to classic car insurance industry standards. You pay full rates for mileage you never use, subsidizing commuters while receiving inadequate protection for your specific situation.

Restoration Work Adds Value That Standard Policies Ignore

Standard insurers view restoration work as vehicle maintenance, not value creation. When you spend $8,000 replacing original upholstery with period-correct materials or $12,000 restoring a carburetor to factory specifications, standard policies treat this as routine repair expense covered under depreciation schedules. Antique car specialists understand restoration adds significant market value, particularly when documented properly. Your receipts, before-and-after photos, and detailed work logs prove this value increase to specialty insurers, but standard policies ignore this documentation entirely.

Spare Parts Coverage Remains Completely Absent

Standard carriers refuse to cover spare parts stored separately from your vehicle. If you maintain a collection of original components for your 1965 Mustang or keep backup parts for reliability, standard auto policies exclude these items completely. Specialty antique car coverage includes spare parts protection, recognizing that original components represent substantial investment and become increasingly difficult to source. These parts (whether stored at home, in a garage, or transported to events) deserve the same protection as your primary vehicle.

Finding Coverage That Matches Your Collection

An independent insurance agent can help you compare quotes from multiple carriers and identify which coverage options align with your specific situation and budget. This personalized approach ensures you pay for protection that matters while avoiding unnecessary coverage gaps. Agents who specialize in collector vehicles understand the real risks you face and structure policies accordingly, ensuring your restoration investments receive proper protection rather than dismissal as routine depreciation.

Final Thoughts

Antique car insurance in Columbus operates on fundamentally different principles than standard auto policies. Your 1965 Mustang or 1970 Dodge Charger appreciates in value when properly maintained, yet standard insurers apply depreciation schedules designed for vehicles losing 15 to 20 percent annually. Agreed value coverage locks in your vehicle’s worth upfront, eliminating the undervaluation disputes that plague collectors using regular policies.

We at Central Ohio Insurance Services, Inc. understand that your antique car represents both a passion and an investment. As a local independent insurance agency in Pickerington, Ohio, we shop multiple carriers to find coverage that actually protects your collection rather than treating it like a daily commuter. Our licensed team recognizes that restoration work adds value, that original components deserve protection, and that driving fewer than 5,000 miles annually should lower your premiums, not penalize you.

Getting proper protection for your historic vehicle starts with a conversation about how you actually use your car and what you’ve invested in its preservation. Contact us to request a quote and discuss your collection with someone who understands antique cars. We’ll compare options from trusted carriers and help you build coverage that matches your budget and protects your investment for years to come.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.