Your classic motorcycle is more than transportation-it’s an investment and a passion project. Standard motorcycle insurance won’t cut it because vintage bikes have unique needs that regular policies simply don’t address.

At Central Ohio Insurance Services, Inc., we understand that classic motorcycle insurance in Columbus requires specialized coverage tailored to your specific ride. Let’s walk through what sets your vintage bike apart and how to protect it properly.

Why Your Classic Motorcycle Needs Different Protection

Age, Condition, and How You Actually Ride

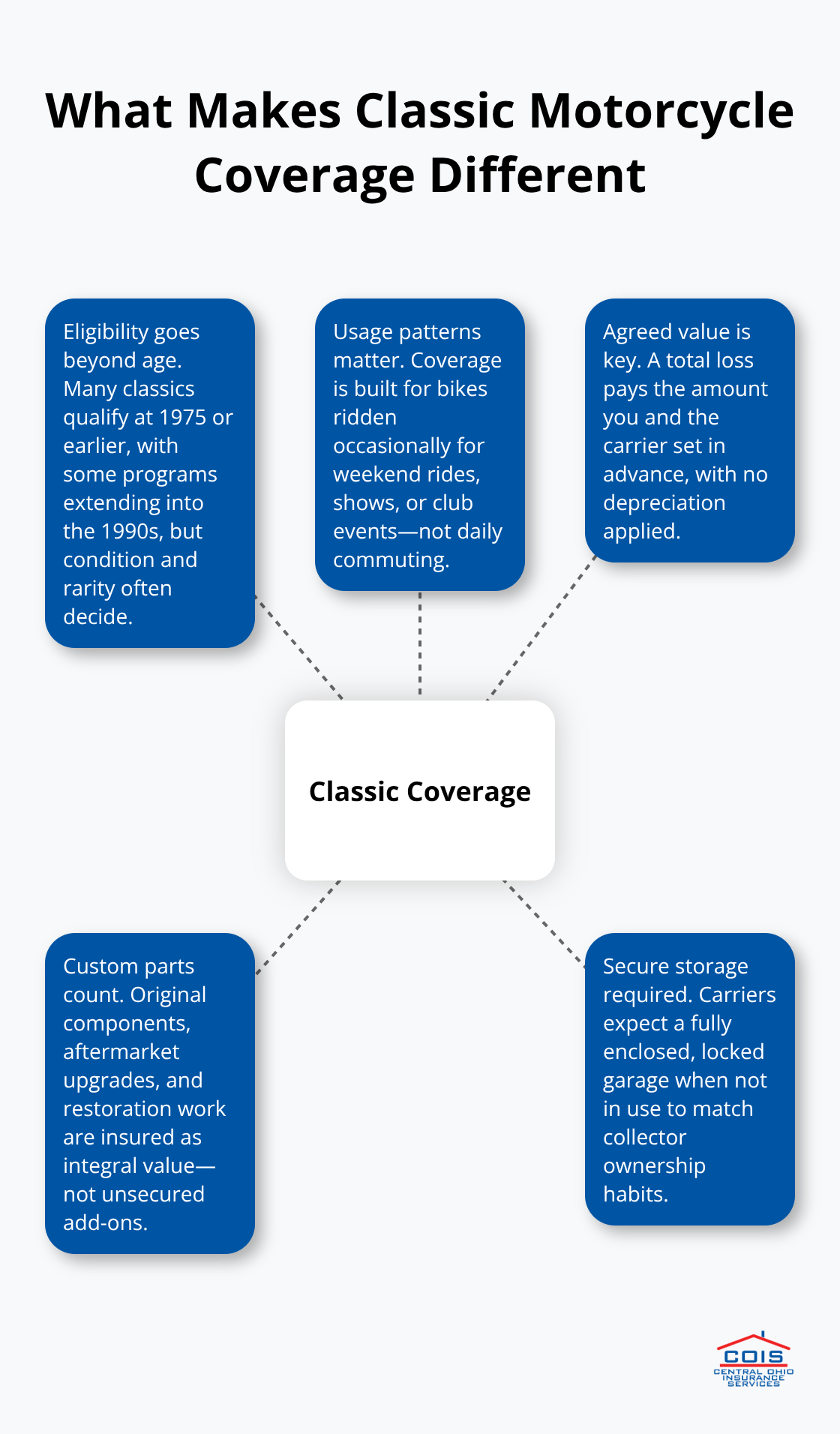

Classic motorcycles occupy a completely different category than standard bikes, and insurance companies recognize this distinction for good reason. A vintage motorcycle from 1975 or earlier typically qualifies for specialized classic coverage, though some insurers extend eligibility to bikes as recent as 1996. The key difference isn’t just age-it’s the bike’s condition, rarity, and how you actually use it. If your motorcycle sits in a secured garage and comes out for weekend rides, shows, or club events rather than daily commuting, you operate in the classic motorcycle space. Standard policies assume daily use and depreciation patterns that don’t apply to your vintage ride.

Agreed Value versus Actual Cash Value

The financial reality of classic motorcycles demands specialized coverage that standard policies won’t provide. A well-maintained vintage bike appreciates in value over time, making agreed value coverage essential. You and your insurer agree upfront on what the bike is worth, and that’s exactly what you receive if it’s totaled, with no depreciation deduction applied. Standard motorcycle policies use actual cash value, which means the insurer decides what your bike is worth at the time of loss, often leaving you thousands of dollars short.

Custom Parts and Restoration Work

Classic motorcycles frequently feature custom aftermarket parts, original manufacturer components, and specialized restoration work that standard policies either don’t cover or severely limit. A collector’s bike might have $15,000 in custom fabrication work that a regular policy treats as unsecured additions rather than protected assets. Specialized classic coverage protects these investments as integral parts of your motorcycle’s value.

Storage and Usage Requirements

Storage requirements also differ significantly between classic and standard motorcycle policies. Classic motorcycle policies expect your bike to live in a fully enclosed, locked garage when not in use, which standard policies don’t mandate. This requirement reflects how collectors actually own and operate their bikes-not how commuters use theirs. Understanding these storage expectations helps you maintain both your coverage and your bike’s condition.

What This Means for Your Coverage Search

Your vintage motorcycle requires protection designed specifically for how you own and operate it. Standard policies simply can’t match the specialized needs that come with classic bikes. When you start comparing coverage options, you’ll want to focus on carriers that understand these distinctions and offer the tailored protection your vintage ride deserves.

Why Standard Policies Fail Classic Motorcycle Owners

Actual Cash Value Destroys Your Investment

Standard motorcycle insurance treats your vintage bike like a commuter that depreciates by the day. The moment you ride a 1975 Harley or a restored Honda CB750 off the lot, a regular policy applies actual cash value, which means an insurer decides what your bike is worth when damage occurs, not what you and the bike’s history actually support. You lose thousands in a total loss because depreciation tables don’t account for your restoration work, rare parts, or the collector’s premium your bike commands. Agreed value coverage, the foundation of proper classic motorcycle protection, insures your collector bike for an amount you and your insurer agree upon upfront, and that’s what you receive if the worst happens. Standard policies won’t offer this flexibility because they’re designed for bikes that lose value, not ones that hold it.

Coverage Gaps Leave Custom Work Unprotected

The coverage gaps extend far beyond valuation. Standard motorcycle policies impose mileage limits or restrict coverage for bikes used primarily for pleasure riding, weekend shows, or club events, yet they still charge rates built on commuter assumptions. Your custom fabrication work, aftermarket handlebars, or original manufacturer parts receive minimal or no protection under standard coverage. You face a choice between leaving investments uninsured or filing claims that carriers deny because they didn’t recognize those components as legitimate parts of your bike’s value.

Roadside Assistance Misses What Vintage Bikes Need

Roadside assistance on standard policies focuses on towing to a repair facility, not the specialized care vintage bikes require. A standard tow truck operator may not understand how to transport a rare 1960s motorcycle without causing damage. Specialized classic motorcycle coverage addresses these concerns with carriers experienced in handling collector bikes.

Finding Coverage Built for How You Actually Ride

Standard motorcycle insurance fails because it was never designed for how you own your classic bike. Carriers that specialize in classic motorcycles understand that your vintage ride sits in a secured garage most of the time, comes out for weekend rides and shows, and holds value rather than depreciating. These carriers build policies around agreed value, custom parts protection, and usage patterns that match reality instead of forcing your bike into a commuter mold. The difference between standard and specialized coverage isn’t subtle-it’s the difference between protecting your investment properly and discovering too late that your policy never covered what matters most. When you start evaluating your options, you’ll want to focus on what specific coverage features matter most for your particular vintage motorcycle.

Securing the Right Coverage for Your Vintage Motorcycle

Agreed Value Coverage Protects Your Investment

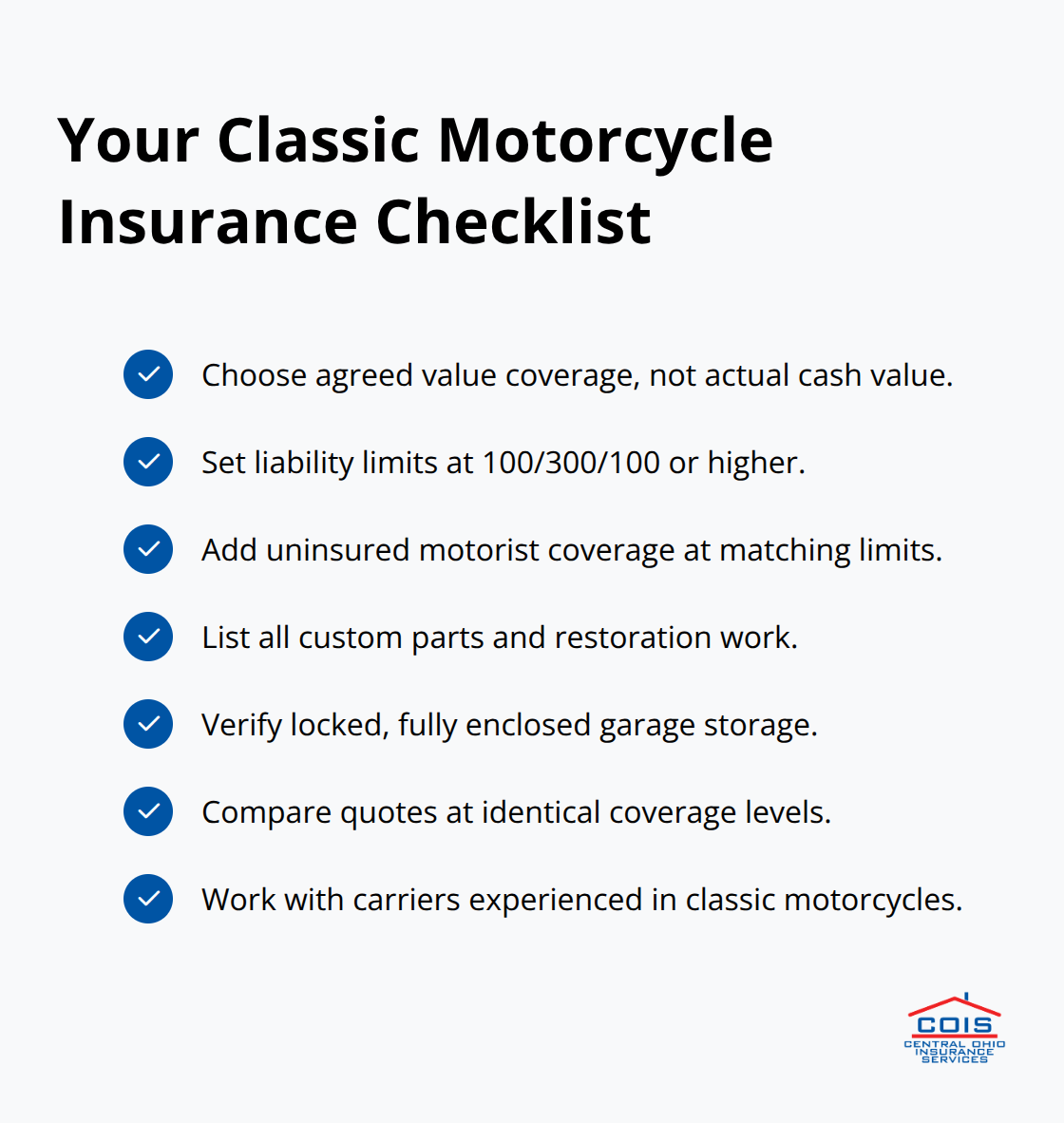

Agreed value coverage stands as the single most important decision you’ll make when selecting classic motorcycle insurance, and this choice separates adequate protection from inadequate coverage. You establish an insured value upfront with your carrier based on the motorcycle’s condition, restoration work, and market value. If your 1975 Harley-Davidson Shovelhead underwent a complete frame-off restoration with $18,000 invested in parts and labor, you insure it for that amount, and you receive exactly that in a total loss claim with zero depreciation applied. Actual cash value, the default on standard policies, means the insurer determines your bike’s worth at claim time using depreciation tables designed for bikes that lose value annually, leaving you thousands short on a restoration investment. Nationwide’s classic motorcycle program uses agreed value as standard, while State Farm’s approach varies by policy type, making it essential to confirm this feature before committing to any carrier. Your bike holds value because of its condition and history, not because it depreciates like a commuter, so your insurance must reflect that reality.

Liability Limits Require Careful Evaluation

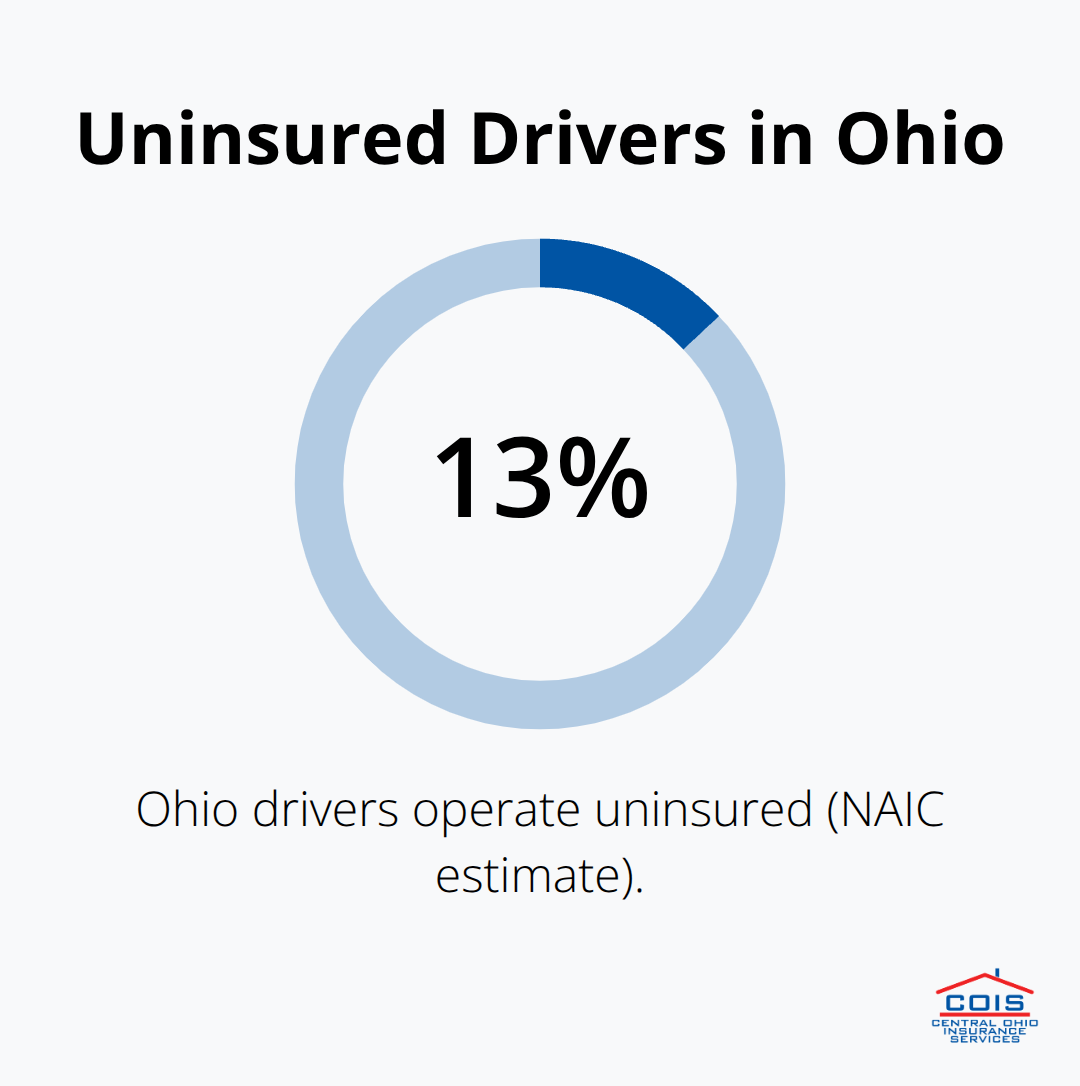

Liability and uninsured motorist coverage demand careful attention because Columbus traffic involves uninsured drivers at rates higher than many assume, and your vintage bike deserves protection matching your actual exposure. Ohio law mandates motorcycle liability coverage, but the minimum limits of 12.5/25/7.5 (bodily injury per person/per accident and property damage) are dangerously low for a collector who can afford a vintage restoration. If an uninsured driver hits your classic motorcycle and causes injury to a passenger or property damage to someone else’s vehicle, those minimum limits evaporate instantly. Carriers like Nationwide and Hagerty allow you to select higher liability limits without penalty, and you should try 100/300/100 or better to reflect both the value of your bike and your financial exposure.

Uninsured Motorist Protection Fills a Critical Gap

Uninsured motorist coverage protects you if someone without insurance causes an accident, covering medical expenses and bike damage up to your selected limit-a feature you absolutely need given that roughly 13 percent of Ohio drivers operate uninsured according to the National Association of Insurance Commissioners. When comparing carriers, request quotes at identical liability and uninsured motorist levels so you evaluate apples-to-apples pricing rather than fall for lower quotes built on inadequate limits. This approach reveals which carriers truly offer the best value for your specific coverage needs.

Final Thoughts

Protecting your classic motorcycle in Columbus requires three core decisions: selecting agreed value coverage that reflects your bike’s true worth, establishing liability limits that match your financial exposure, and partnering with a carrier that understands vintage bikes rather than forcing them into standard policy molds. Your restoration investment, custom parts, and the way you actually use your motorcycle demand insurance built specifically for collectors, not commuters. Standard policies fail because they apply depreciation logic to bikes that hold value, leaving you thousands short when you need coverage most.

You’ll need to provide accurate information about your motorcycle’s condition, restoration work, current value, and usage patterns when you request quotes for classic motorcycle insurance Columbus. Carriers like Nationwide, Hagerty, and State Farm each approach classic motorcycle insurance differently, so comparing quotes at identical coverage levels reveals which offers the best protection for your specific bike. Specify your agreed value amount, desired liability limits, and any custom parts or aftermarket equipment you want protected to prevent surprises later.

We at Central Ohio Insurance Services, Inc. shop multiple carriers to find competitively priced solutions for your classic motorcycle insurance needs, handling the comparison work so you don’t have to. Whether your bike is a 1975 Harley, a restored Honda CB750, or a rare collector’s piece, our licensed team understands the specialized protection your investment requires. Contact our Pickerington office to discuss your classic motorcycle coverage and receive a custom quote that reflects what your bike actually means to you.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.