Classic car insurance premiums vary wildly depending on factors most owners don’t consider until they get a quote. At Central Ohio Insurance Services, Inc., we’ve seen collectors overpay by hundreds of dollars annually simply because they didn’t understand what insurers actually look at.

The good news is that your costs aren’t fixed. Several concrete steps can lower what you pay while keeping your vehicle properly protected.

How Your Car’s Value Determines What You Pay

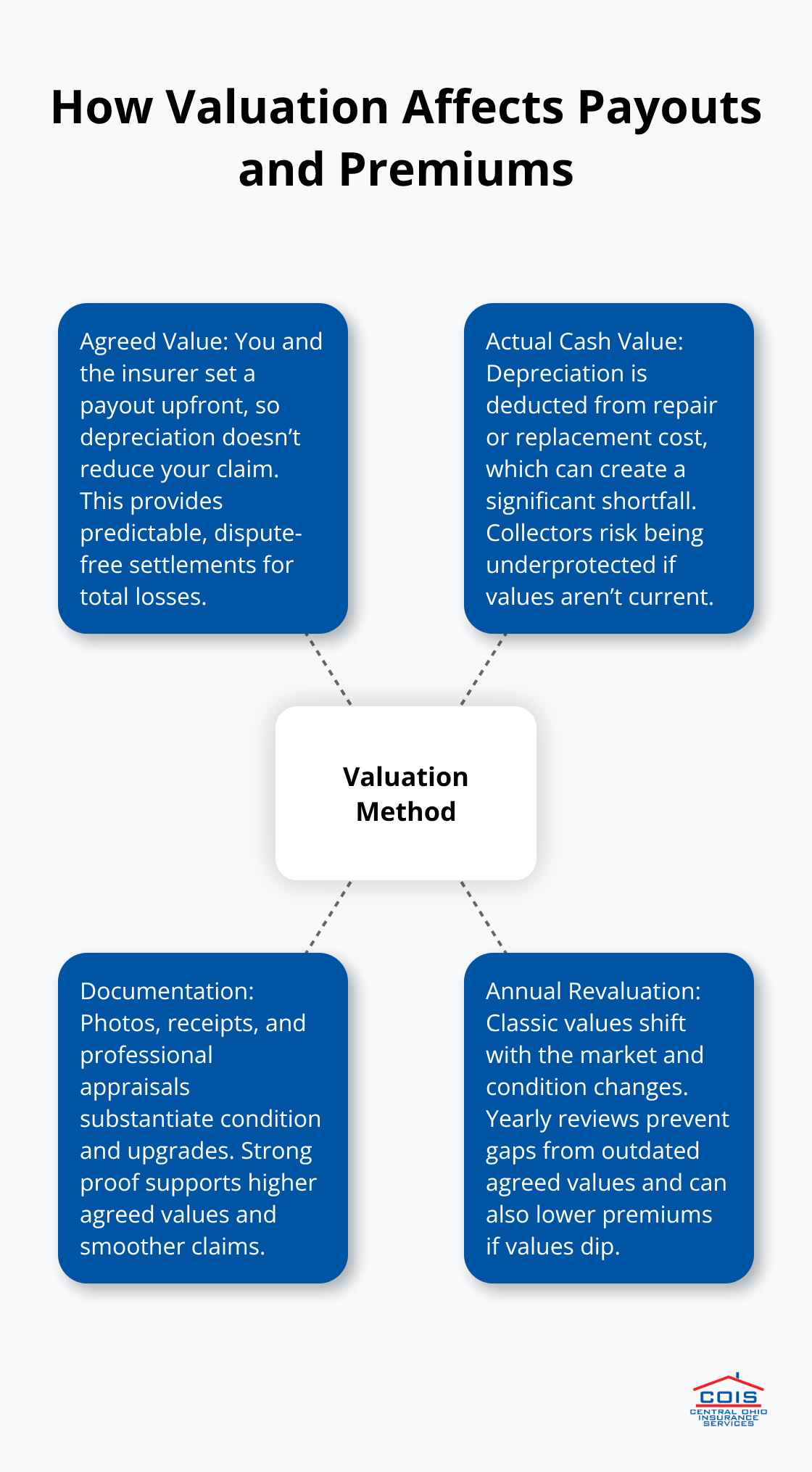

The valuation method your insurer uses fundamentally changes your premium and what you’ll receive if your classic car is damaged or totaled. Agreed value coverage eliminates depreciation and sets a predetermined payout amount that you and your insurer establish upfront, protecting you from depreciation disputes when you need a claim paid. With actual cash value, insurers subtract depreciation from the repair or replacement cost, which means a 1985 classic car worth $15,000 today might only net you $8,000 after depreciation is factored in-a massive gap that leaves collectors underprotected. Agreed value eliminates this problem entirely. You establish the car’s value at policy inception, and that’s what you receive if total loss occurs, assuming repair costs don’t exceed that amount. The difference in peace of mind is substantial, and premiums for agreed value policies remain competitive because classic car owners typically drive 2,000 to 7,500 miles annually, keeping risk low.

Prove Your Car’s Condition With Documentation

Documentation is where most classic car owners stumble. Insurers evaluating agreed value need concrete proof of your car’s condition and market standing, not assumptions. You should take detailed photos of the interior, exterior, engine bay, and undercarriage from multiple angles. Include receipts for any restoration work, parts replacements, or upgrades completed in the last five years. Professional appraisals carry significant weight-Hagerty and American Modern, two major classic car insurers, both rely heavily on documented condition assessments and recent comparable sales. If you invested $8,000 restoring the engine or $3,000 on new upholstery, that documentation directly supports a higher agreed value and prevents underinsurance. Many owners skip this step and regret it later when their agreed value sits artificially low. You should bring your documentation to the agent conversation; it demonstrates seriousness and accuracy, making negotiations smoother.

Revalue Your Car Annually to Stay Protected

Annual appraisals protect your investment as market conditions shift. Classic car values don’t depreciate like everyday vehicles; many appreciate steadily, especially well-maintained examples. A car valued at $12,000 three years ago might now be worth $14,500 based on market trends and condition improvements. Without periodic revaluation, you leave money on the table if a total loss occurs, since your payout caps at the outdated agreed value. Conversely, if your car’s value drops due to market softness in a particular model year, you can adjust downward and lower your premium accordingly. Most carriers evaluate agreed value annually during renewal, and you should request reevaluation proactively if you complete significant restoration work or if market data suggests meaningful value changes. This annual conversation with your agent takes 20 minutes but prevents thousands in coverage gaps.

The valuation foundation you establish now directly influences how much you’ll pay each year and what protection you actually receive. Your next decision involves the other major cost drivers-factors like how you use the car, where you store it, and your driving history all shape your final premium.

What Really Drives Your Classic Car Insurance Cost

Age, Model, and Vehicle Condition Shape Your Rate

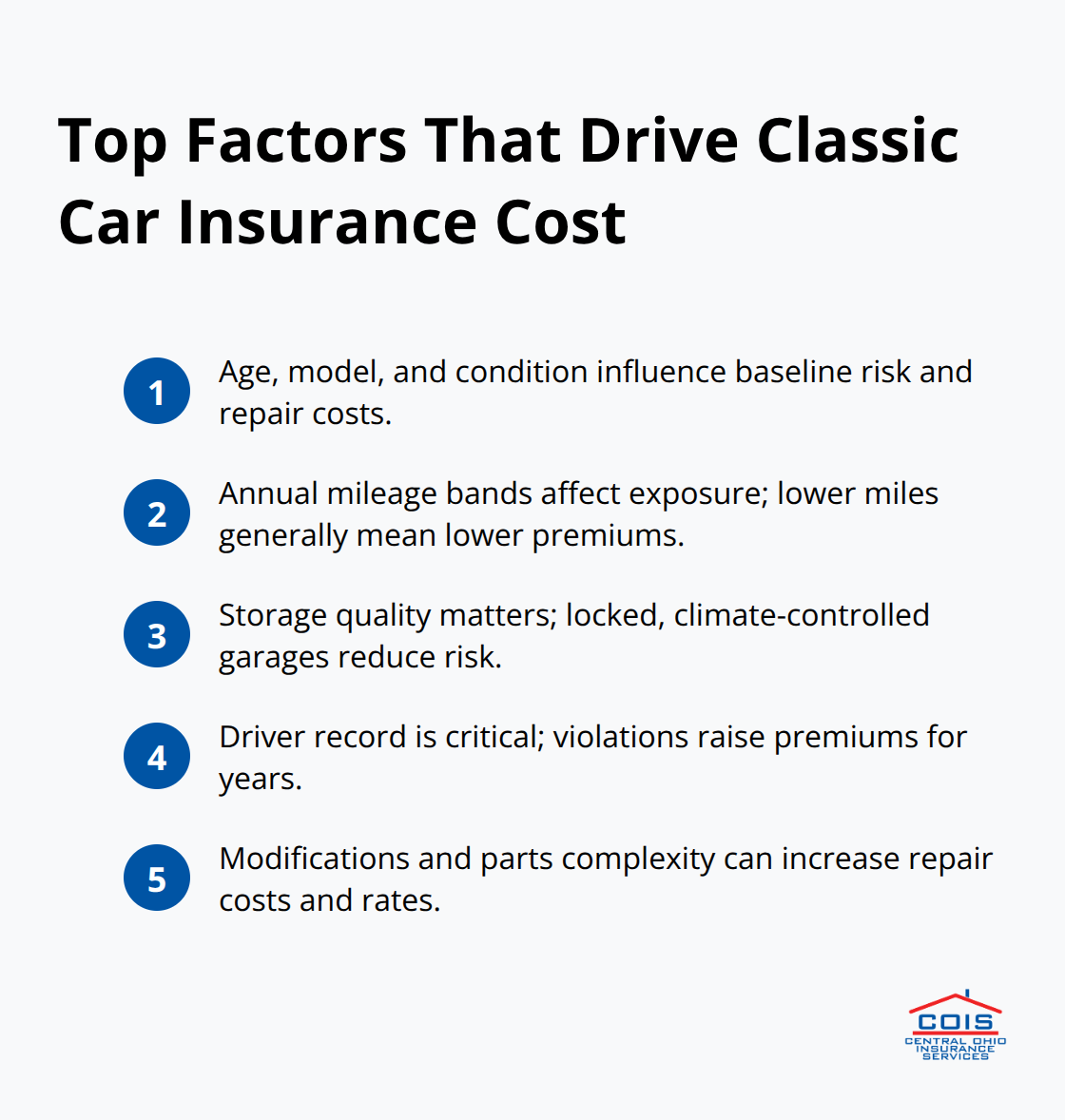

Your vehicle’s age, model, and condition form the foundation of your premium calculation, and these factors matter far more than most owners realize. A 1975 Chevrolet Corvette and a 1995 Porsche 911 might both qualify for classic car coverage, but their premiums differ dramatically because insurers assess risk through a specific lens: how often the car leaves the garage, where it sits when parked, and who drives it. The model year itself influences pricing-certain 1960s and 1970s vehicles have documented lower theft rates than others, and insurers possess years of claims data proving which classics cost more to repair and which ones sit safely in garages. A meticulously maintained original-condition 1985 Mercedes typically costs less to insure than a heavily modified hot rod, since modifications increase repair complexity and parts sourcing difficulty.

Mileage and Storage Create Measurable Cost Differences

Classic cars insured for 2,000 to 7,500 miles annually cost substantially less than vehicles driven 10,000 miles per year, since lower mileage directly correlates with fewer accident opportunities. Your storage setup matters equally-a car parked in a climate-controlled, locked garage reduces theft and weather-related damage risk far more effectively than one sitting in an open carport. Storing classic cars in a secured environment like a locked garage usually results in reduced insurance premiums, making climate control one of the highest-return investments you can make for cost reduction. Insurers know this relationship between storage and risk, and they price accordingly.

Driving Record and Security Measures Impact Premiums

Your driving record carries outsized weight; a single speeding ticket or minor accident can spike your rate by hundreds of dollars annually, while a clean history spanning five years signals lower risk and qualifies you for meaningful discounts. Any traffic violations within the last five years appear on your record and affect pricing. Documented security measures like alarm systems or GPS tracking reduce your comprehensive premium by approximately 15 to 20 percent, and insurers recognize and often discount these installations. A defensive driving course can earn you premium reductions with many carriers if you’ve had violations in the past three years.

Prepare Documentation for Your Agent Conversation

Honest mileage declaration prevents coverage gaps and unnecessary premium inflation. Bring documentation of your storage setup, a list of any security devices you’ve installed, and your actual mileage records from the past year to your agent meeting. This concrete information allows your agent to find the most competitive rate because they can accurately represent your risk profile to underwriters rather than relying on estimates that usually work against you. An independent agency can shop multiple carriers, meaning your documented details help them match you with the insurer offering the best combination of price and coverage for your specific situation.

Ways to Lower Your Classic Car Insurance Premiums

Bundle Policies for Immediate Savings

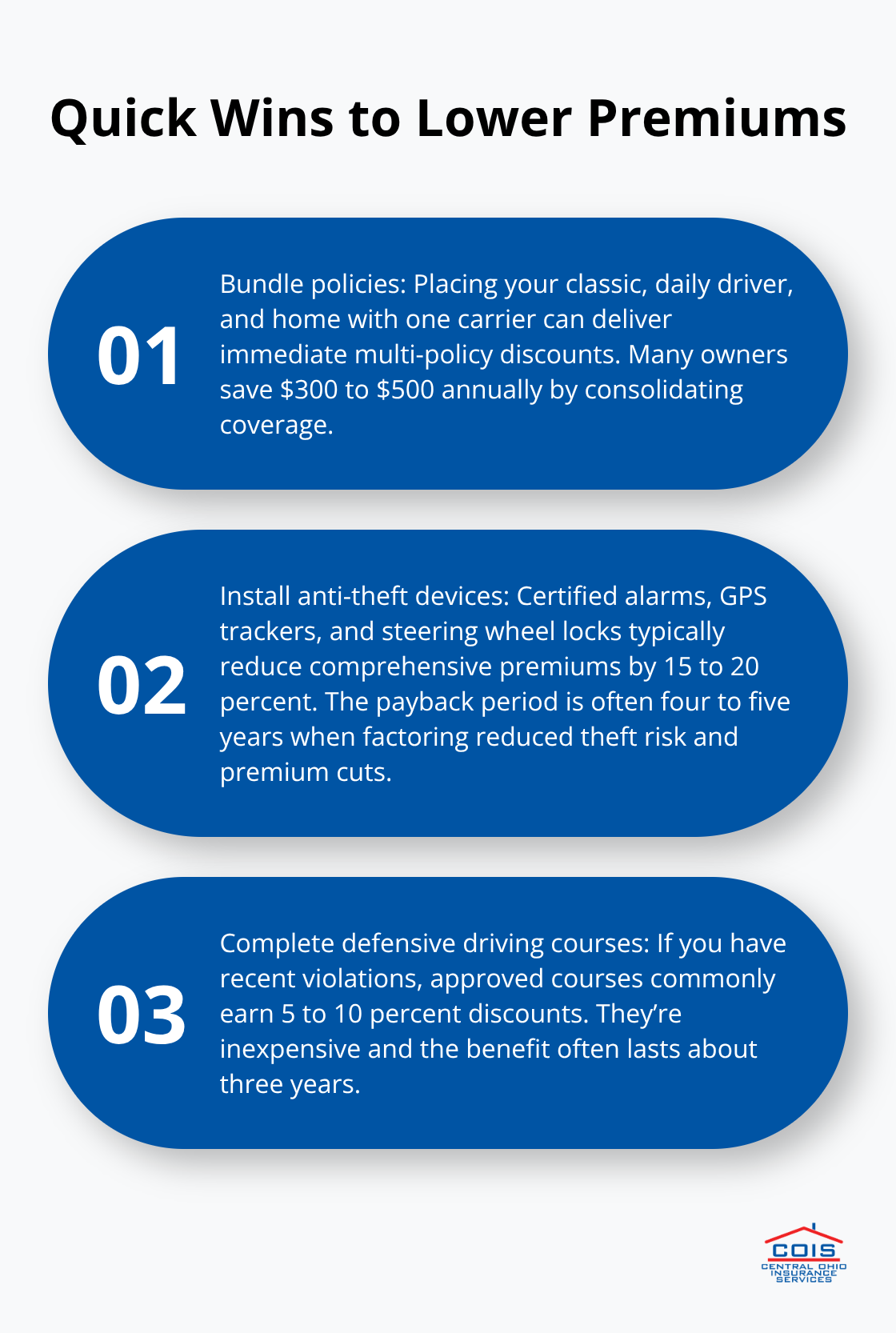

Bundling your classic car policy with homeowners, renters, or other auto coverage yields multi-policy discounts across your entire package, making it one of the fastest ways to lower premiums without sacrificing protection. Most insurers reward customers who consolidate multiple policies, and the savings compound quickly-a collector insuring a classic car, a daily driver, and a home can easily save $300 to $500 annually just by placing everything with one carrier. Shop this bundled approach explicitly when obtaining quotes; many agents won’t highlight the discount unless you ask, and some carriers structure their pricing to reward consolidation more aggressively than others.

Install Anti-Theft Devices and Alarms

Anti-theft devices deliver measurable returns: installing a certified alarm system, GPS tracker, or steering wheel lock typically reduces your comprehensive premium by 15 to 20 percent. These aren’t theoretical savings-insurers base these discounts on documented theft reduction data, meaning a $400 alarm installation that cuts your annual premium by $80 to $120 pays for itself in four to five years while protecting your investment. The upfront cost becomes negligible when you calculate the long-term protection and premium reduction working together.

Complete Defensive Driving Courses

Defensive driving courses work similarly to security installations; if you’ve had a violation in the past three years, completing an approved course often qualifies you for a 5 to 10 percent discount, with some insurers offering even larger reductions. The investment is minimal-most courses cost $25 to $50 and take four hours online-and the discount typically lasts three years. This single action addresses past violations while signaling to insurers that you take safety seriously.

Maintain a Clean Driving History

Your driving record remains the single most controllable factor in your premium equation. A clean five-year history without violations, accidents, or claims signals low risk and positions you for the best available rates; conversely, even one speeding ticket can increase your annual cost by $200 to $400 depending on the violation severity and your insurer’s underwriting rules. Traffic infractions stay on your record for three to five years, so avoiding violations during this window protects your classic car rates substantially.

Document Everything for Your Agent

When you meet with an independent agency, bring documentation of any completed defensive driving courses, proof of security installations, and your actual mileage records. This concrete information allows agents to shop multiple carriers accurately rather than relying on estimates that typically work against you. An independent agency can match you with insurers offering the best combination of price and coverage for your specific risk profile, and your documented clean history becomes a powerful negotiating tool across carriers competing for your business.

Final Thoughts

Classic car insurance premiums reflect multiple interconnected factors, and understanding each one positions you to make smarter decisions about coverage and cost. Your valuation method, vehicle condition, storage setup, driving history, and security measures all work together to determine what you pay annually. Shopping multiple carriers reveals dramatic price differences for identical coverage-one insurer might quote $450 annually for agreed value protection on your 1978 Datsun 280Z, while another quotes $620 for the same vehicle and coverage level.

Gather your documentation before contacting an agent. Compile photos of your vehicle’s condition, receipts for restoration work, your actual mileage records from the past year, and details about your storage setup and any security devices installed (including proof of completed defensive driving courses). This information transforms your agent conversation from vague estimates into precise underwriting details that carriers can accurately price, revealing the true competitive differences between providers.

Contact Central Ohio Insurance Services, Inc. to shop your classic car insurance coverage. Their licensed team handles the carrier comparison work for you, presenting clear options with fast quotes and hands-on guidance throughout the process. Classic car insurance premiums don’t have to drain your budget when you work with professionals who understand the specialty market.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.