Homeowners who carry both a house and a car often miss out on significant savings. Auto insurance for homeowners becomes far more affordable when you bundle it with your home coverage.

We at Central Ohio Insurance Services, Inc. help homeowners understand how combining policies can reduce premiums while maintaining the protection you need. This guide walks you through the real savings, what to compare, and how to get started.

What You Actually Get When You Bundle Home and Auto

Bundling home and auto insurance means purchasing both policies from the same insurer, which triggers a multi-policy discount on your combined premium. Up to 25% represents what some insurers advertise for multi-policy discounts, which translates to roughly $900 per year if your total annual insurance spend runs $5,000. The mechanics are straightforward: you consolidate billing into a single payment, manage both policies through one online account, and work with one insurer for claims and policy adjustments. Progressive offers new customers who bundle savings over 25% on average, while State Farm reports that bundling auto and homeowners can save up to $1,429 based on a 2025 national survey of new policyholders who switched to their coverage.

However, the discount amount varies significantly by state and insurer, which is why shopping quotes matters more than assuming any bundle is automatically cheaper.

Coverage combinations you can actually bundle

Most insurers allow you to bundle auto with homeowners, renters, condo, or even specialty policies like motorcycle, boat, or RV coverage. The more policies you add, the stronger your discount typically becomes. Progressive highlights a practical benefit: when a single event damages both your home and vehicle, you pay only one deductible instead of two, which can save thousands during a major claim. Managing multiple coverages under one insurer means a single renewal date, one bill, and one point of contact for questions or changes-eliminating the administrative headache of coordinating across separate companies. When you move from renting to homeownership or add a second vehicle, bundling becomes especially convenient because you can adjust coverage in one place rather than coordinating across multiple insurers.

Why insurers push bundling

Insurers offer bundled discounts because they retain more of your business and reduce customer acquisition costs. A customer with both home and auto policies costs less to service than two separate customers, and bundling increases loyalty-dropping one policy often means losing the discount on the other, which discourages switching. This incentive structure means insurers can afford to discount bundled policies while still improving their bottom line. However, that same incentive can work against you if you don’t shop around annually. Many policyholders renew bundled coverage without checking whether unbundling or switching to a competitor would actually save more money. The reality is that a bundled discount from one insurer might be lower, but a competitor’s standalone premium for the same coverage could be lower overall.

The real catch with bundled discounts

Insurers sometimes start with a higher base premium to offer a discount, so the final premium may not reflect true savings. This practice means you need to compare apples-to-apples by matching coverage levels and limits across options. A bundled policy from one carrier might appear cheaper than separate policies from another, but only if you examine the actual coverage you receive. Some insurers also raise premiums over time, which erodes the value of the discount and makes annual shopping essential. The convenience of one insurer can trap you into complacency, so treat your renewal as an opportunity to verify that your bundle still beats the alternatives.

How Much You Actually Save When You Bundle

Real Savings Numbers from Real Homeowners

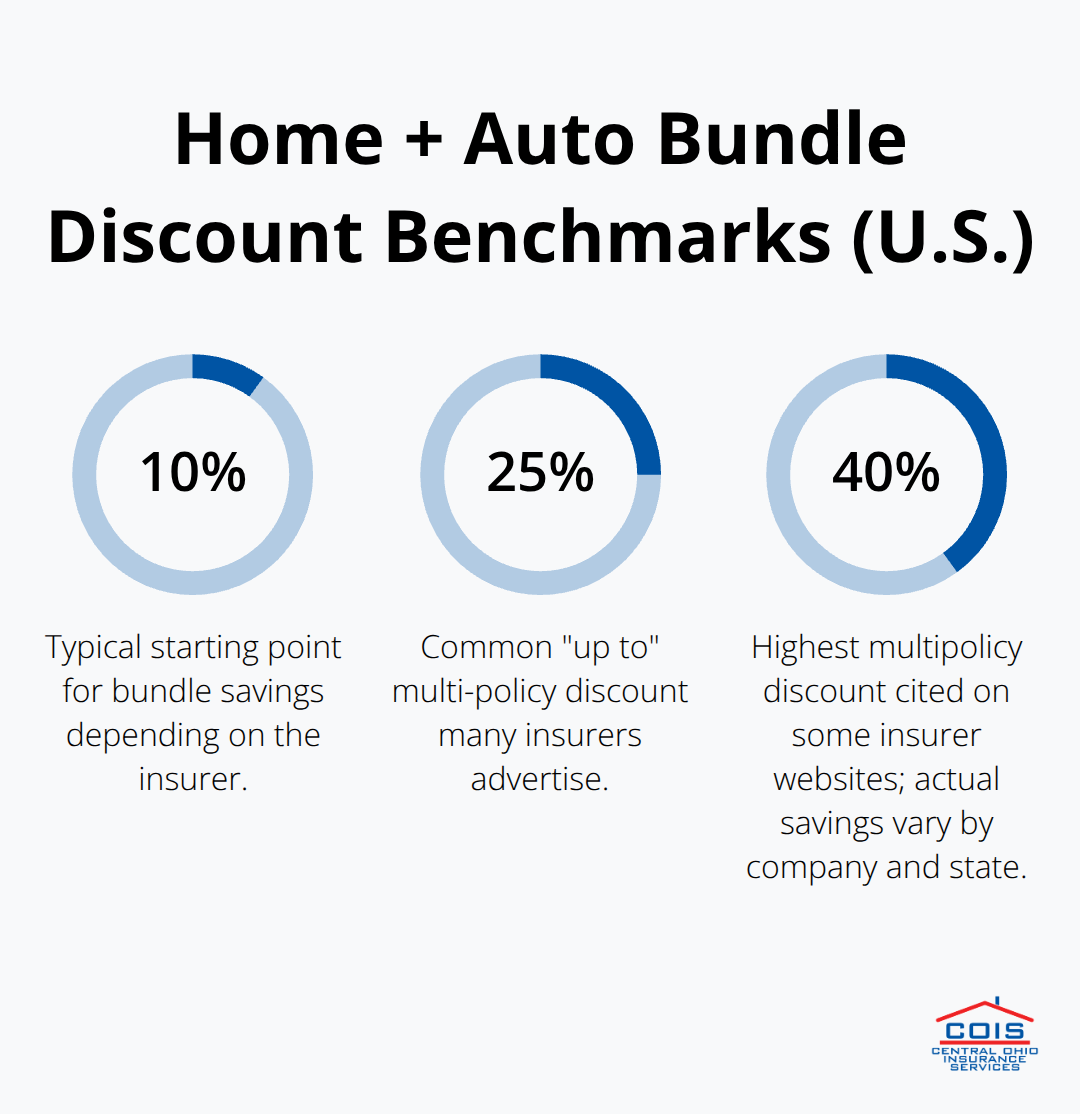

Bundling delivers concrete savings, but the amount depends entirely on your current coverage, where you live, and which insurer you choose. A 2025 State Farm national survey found that homeowners who switched to State Farm and bundled auto with homeowners saved up to $1,429 annually. Progressive reports that new customers who bundle save over 25% on average on their combined premium. When you bundle auto insurance with home coverage through one carrier, savings typically range from 10% to 25% depending on the insurer. A multipolicy discount could save you up to 40%, according to some insurer websites, though the discount will vary depending on the company and where you live. These numbers represent real households with real savings, not theoretical estimates. However, the discount you receive depends on your specific situation: your driving record, home value, location, claims history, and the coverage limits you choose all factor into the final number. Two homeowners with identical homes and vehicles might receive vastly different bundle discounts from the same insurer based on these variables. This is why quoting with multiple carriers matters far more than accepting the first bundled offer you receive.

How Discounts Stack Across Your Policies

The way discounts stack in a bundled package differs by insurer and state. Some insurers apply a flat percentage discount to your combined premium, while others calculate discounts separately for each policy and then combine them. Progressive offers a practical advantage that many homeowners overlook: when a single event damages both your home and vehicle, you pay only one deductible instead of two, potentially saving thousands during a major claim. This single-deductible benefit can be worth more than the percentage discount itself if you experience a covered loss.

Long-Term Bundling: The Loyalty Trap

Long-term bundling creates stability in your premiums because insurers reward loyalty and retention, but this only works if you shop competitively every renewal period. Many homeowners lose bundling savings over time because rates creep upward while they renew without checking alternatives. The insurer has no incentive to maintain your discount if you stay passive. Over ten years, consistent bundling savings could add up significantly, but only if you verify annually that bundling still beats unbundling or switching.

Shopping Your Bundle Every Year Matters

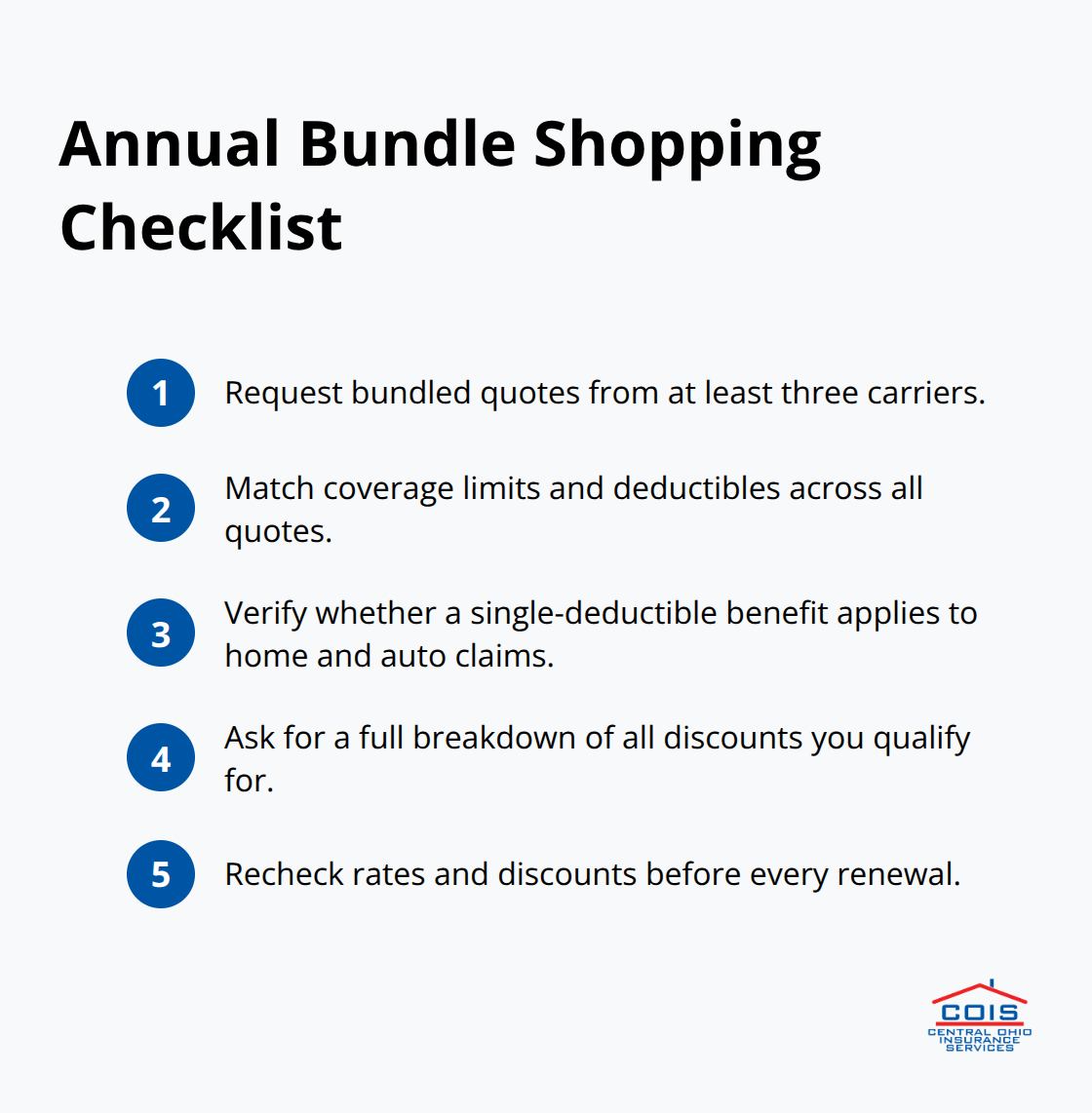

Request bundled quotes from at least three carriers every renewal to confirm your bundle remains competitive. Your current insurer’s rates may have risen while a competitor’s have fallen, or vice versa. The bundled discount you received last year might no longer represent your best option. Taking thirty minutes to shop annually protects thousands in potential savings over your lifetime as a homeowner.

With this foundation on savings in place, the next step involves understanding what coverage limits and deductibles actually protect you when you bundle.

What Coverage and Deductibles Actually Protect You

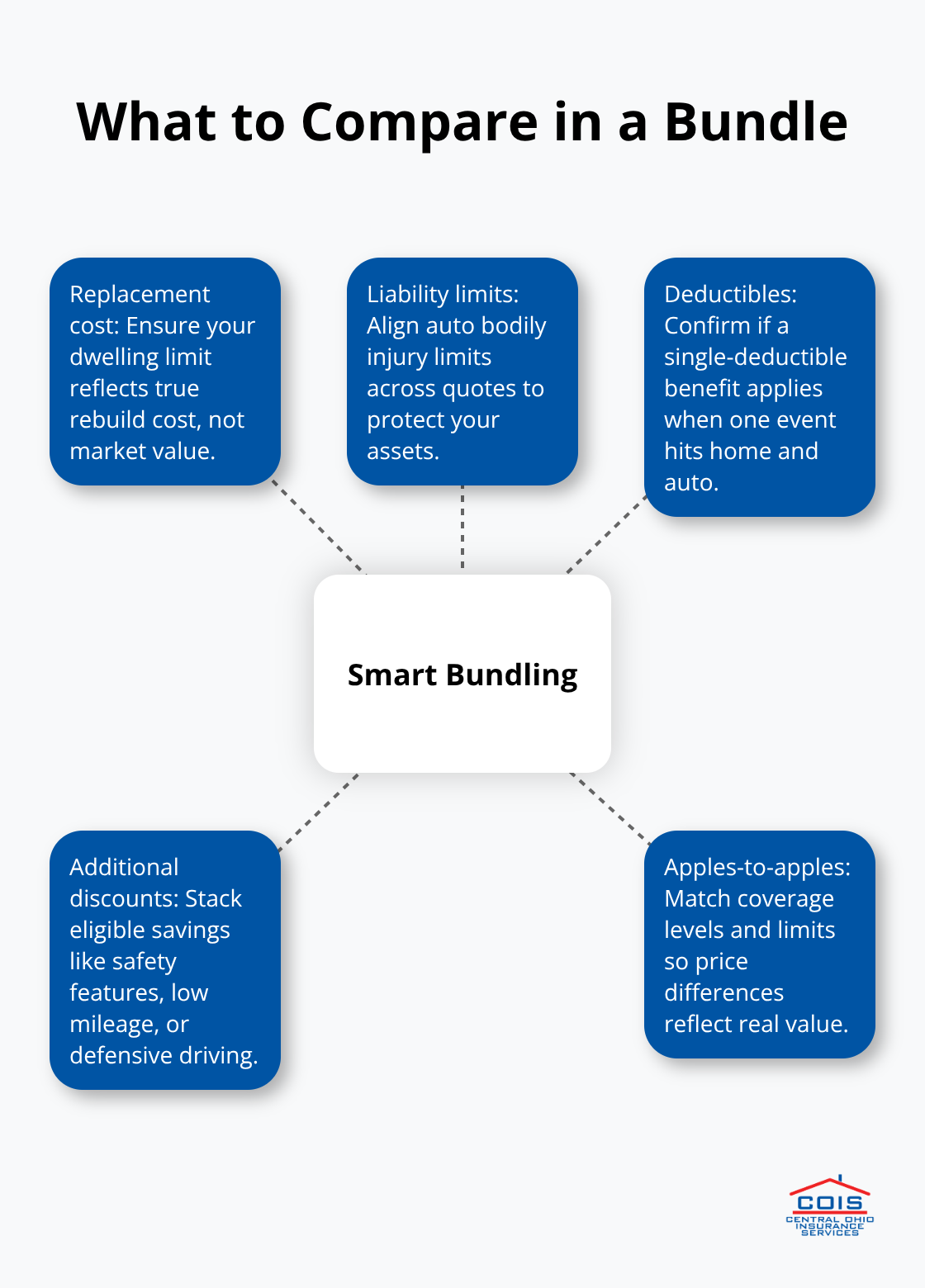

Bundling only works if you have adequate coverage limits and deductibles that match your actual risk. Many homeowners make the mistake of comparing bundled premiums without verifying that the coverage underneath is identical across carriers. A bundled policy from one insurer at $1,200 per year looks cheaper than $1,400 from another, but if the first policy has a $500,000 home coverage limit and the second has $750,000, you’re comparing apples to oranges.

Determine Your Home’s Replacement Cost

Start by establishing your home’s replacement cost, not its market value. If your home costs $400,000 to rebuild after a total loss, your dwelling coverage should reflect that amount. Many homeowners underestimate rebuild costs because they confuse property value with construction expense. Construction costs have risen significantly in recent years, and older estimates often fall short. Contact a local contractor or use online rebuild estimators to establish a realistic figure, then verify that any bundled policy you consider covers that amount.

Match Liability Limits Across All Quotes

For auto coverage, match liability limits across quotes as well. If one carrier quotes you $100,000 in bodily injury liability and another offers $250,000, the premium difference reflects real coverage differences, not just bundling efficiency. We at Central Ohio Insurance Services, Inc. recommend liability limits of at least $250,000 per person and $500,000 per accident for auto, especially if you own a home with assets to protect.

This approach protects your financial security in the event of a serious accident.

Understand How Deductibles Stack in Bundled Policies

Deductibles in bundled policies work differently depending on the insurer, and this distinction can save or cost you thousands. Progressive offers a single-deductible benefit where a covered loss affecting both your home and vehicle uses only one deductible instead of two, potentially saving thousands during a major claim. Most other insurers apply deductibles separately to each policy, so you pay one deductible on your home claim and another on your auto claim if both are damaged in the same event. Ask your insurer directly how deductibles stack in their bundled policies before purchasing.

Higher deductibles lower your premium, but only choose a deductible amount you can actually afford to pay out of pocket if a loss occurs. A $1,000 deductible saves more premium than a $500 deductible, but if you lack emergency savings, a claim could become financially devastating. The deductible you select should align with your financial capacity to handle an unexpected loss.

Identify Additional Discounts and Loyalty Rewards

Loyalty rewards and additional discounts vary wildly by carrier and state, so request a full discount breakdown from each insurer you quote. Some carriers offer discounts for low mileage, safety features, completing a defensive driving course, or maintaining continuous coverage. These add-on discounts can stack with your bundling discount, but only if you actively qualify for them. Don’t accept a bundled quote at face value; instead, ask what additional discounts apply to your specific situation and verify the total savings across all lines before committing. The insurer should provide a clear itemization of every discount applied to your bundled package so you understand exactly what you receive.

Final Thoughts

Bundling auto insurance with homeowners coverage delivers measurable savings and genuine convenience, but only if you approach it strategically. The real value lies not in accepting the first bundled offer you receive, but in comparing multiple carriers to confirm that your bundle actually beats the alternatives. State Farm’s 2025 data shows homeowners who switched and bundled saved up to $1,429 annually, while Progressive reports new customers who bundle save over 25% on average-these numbers represent actual households, not theoretical estimates.

Request bundled quotes from at least three carriers and compare them side by side, matching your coverage limits and deductibles across each quote so you compare identical protection rather than just different prices. Verify that your home’s dwelling coverage reflects your actual rebuild cost and that your auto liability limits protect your assets. Ask each insurer about additional discounts you qualify for and request a full breakdown of how their bundling discount stacks with other savings.

We at Central Ohio Insurance Services, Inc. specialize in helping homeowners navigate bundling decisions with unbiased guidance. Our licensed team shops multiple carriers to find competitively priced auto insurance for homeowners that matches your actual coverage needs, not just the lowest premium. Contact us today to request your bundled quotes and get started.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.