Boat ownership in Columbus comes with real costs, and insurance is one of them. We at Central Ohio Insurance Services, Inc. know that finding affordable boat insurance Columbus doesn’t mean sacrificing the protection you need.

This guide walks you through what drives your rates up, proven ways to cut your premiums, and the coverage options that actually matter for your situation.

What Drives Your Boat Insurance Costs

Your boat insurance premium in Columbus isn’t random. Insurance carriers analyze hard data points that directly correlate to risk, and understanding these factors helps you make smarter decisions. The three biggest drivers of your rate are what you own, how you use it, and your track record on the water. Boat type and value sit at the top of the list because a $15,000 fishing boat costs far less to insure than a $150,000 cabin cruiser. Hull material, engine size, and age matter too-aluminum boats typically cost less to cover than fiberglass ones, and newer vessels with modern safety systems often qualify for lower premiums.

Boat Type Determines Your Baseline Cost

Personal watercraft like Jet Skis and WaveRunners carry higher premiums than pontoons because they’re involved in more accidents statistically. Fishing boats fall in the middle range, while sailboats and slower pontoons typically offer the lowest rates. The boat’s age and condition matter as much as its type. A 2010 model with original equipment costs more to insure than a 1995 model because replacement parts are pricier and repair shops charge more for newer technology. Horsepower and engine count push rates up directly-a twin-engine speedboat will run 30 to 50 percent more than a single-engine version of similar hull size.

Usage Patterns and Storage Location Shape Your Rate

Where you store your boat and how frequently you take it out shape your rate significantly. A pontoon boat used on calm inland lakes near Columbus gets a better rate than the same boat operated in coastal waters or taken out 200 days a year. Seasonal storage during winter months qualifies you for lay-up discounts in Ohio. Freshwater-only boating costs less than saltwater or mixed-water use because saltwater corrodes hulls faster and increases claim frequency. Keeping your boat at home versus docking it year-round at a marina also affects pricing-marina storage sometimes triggers higher rates due to increased theft and weather exposure.

Your Boating Record Drives Long-Term Rates

A clean claims history over five years typically earns you the best available rates. One accident or incident can add 20 to 40 percent to your premium for three to five years. Safety course completion, however, works in your favor immediately and sometimes qualifies you for multi-year discounts. Completing an approved boating safety course can lower your premium by 10 percent or more, making it one of the fastest ways to cut costs without reducing coverage.

Your experience and claims history round out the calculation-a boater with ten years of clean operation and a completed safety course will pay substantially less than someone with two accidents in three years.

Now that you understand what insurers examine when they calculate your rate, the next section shows you exactly how to reduce those costs without compromising the protection your boat needs.

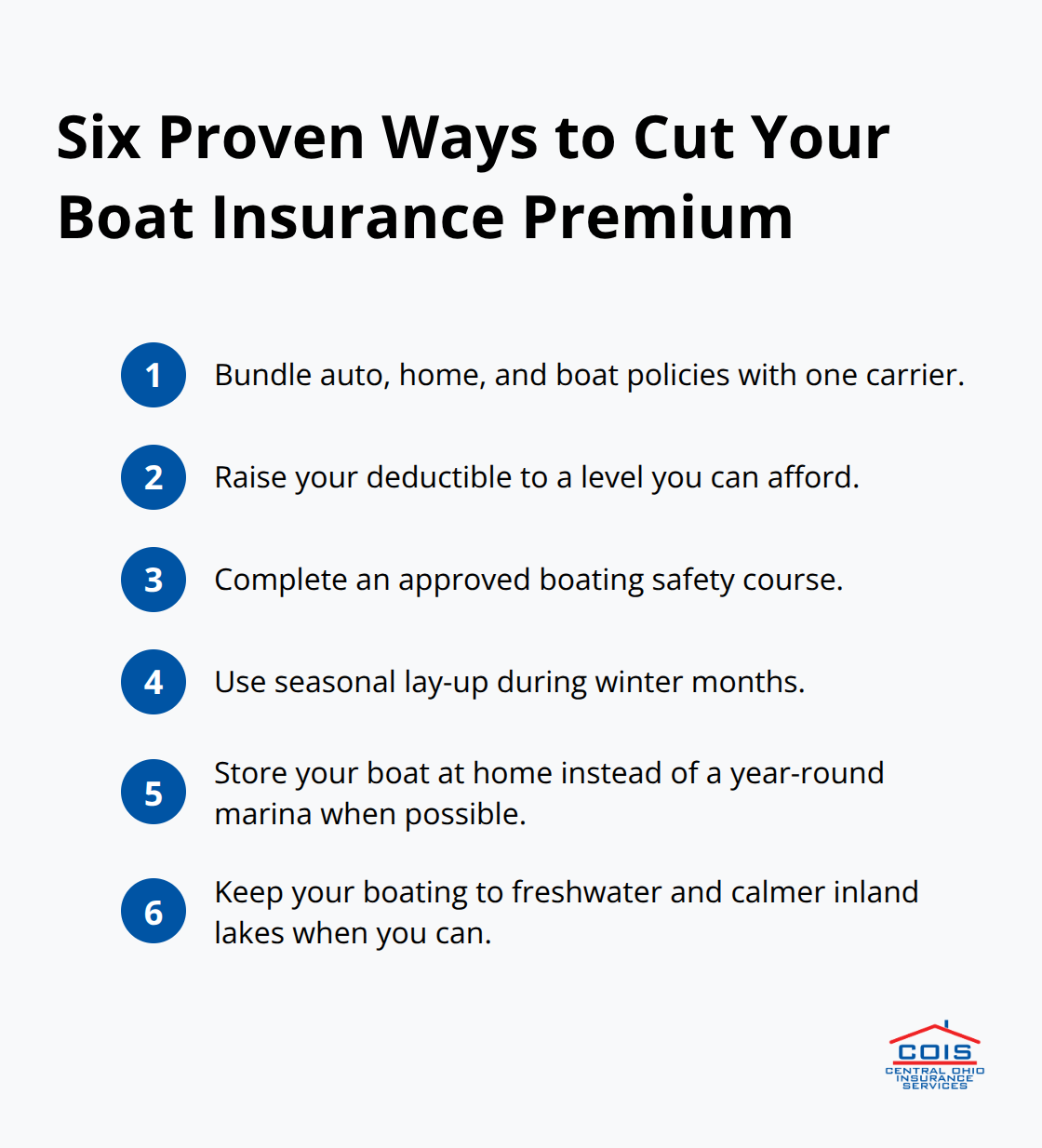

How to Cut Your Boat Insurance Premiums Without Sacrificing Protection

Reducing what you pay for boat insurance requires action, not luck. Three concrete strategies work consistently for Columbus boaters: bundling your policies, adjusting your deductible, and completing a boating safety course. These aren’t theoretical suggestions-they’re backed by how insurance carriers price risk and reward responsible boaters.

Bundle Your Policies for Immediate Savings

Bundling auto, home, and boat insurance with the same carrier typically cuts your boat premium by 10 to 25 percent, depending on the carrier and what policies you combine. Nationwide and GEICO Marine both offer multi-policy discounts that stack, meaning a boater who bundles boat, auto, and homeowners coverage saves substantially more than someone carrying policies separately. The math is straightforward: carriers want to keep multiple policies under one roof because it reduces their servicing costs and your likelihood of switching.

When you shop for quotes, ask about bundle discounts explicitly. Many boaters miss this savings opportunity because they don’t request it upfront. As an independent agency, Central Ohio Insurance Services, Inc. shops multiple carriers to help you find the best bundle rates available in your area.

Raise Your Deductible to Match Your Financial Situation

Your deductible choice directly controls your out-of-pocket cost after a claim, and most boaters set it too low. Increasing your deductible from $500 to $1,000 typically lowers your annual premium by 10 to 15 percent, while jumping to $2,500 can cut costs by 20 to 30 percent depending on your boat’s value and coverage type.

This strategy only works if you have cash reserves to cover the higher deductible after an incident. Don’t increase it beyond what you can actually pay out of pocket. The goal is to lower your premium while maintaining financial protection, not to create a hardship if you file a claim.

Complete a Boating Safety Course for Long-Term Discounts

Boating safety course completion pays immediate dividends on your premium. Completing an approved course through BoatUS Foundation, your state’s boating safety program, the U.S. Power Squadrons, or the U.S. Coast Guard Auxiliary qualifies you for discounts ranging from 10 percent to 15 percent on your premium. Many carriers offer these discounts for three to five years after completion, making a single 8-to-10-hour course investment one of the fastest ways to lower your rate.

These three moves-bundling policies, raising your deductible to a level you can afford, and taking a safety course-can reduce your annual boat insurance cost by 35 to 50 percent while keeping you properly protected on the water. With your premiums optimized, the next step is understanding which coverage options actually protect your boat and your wallet in Columbus.

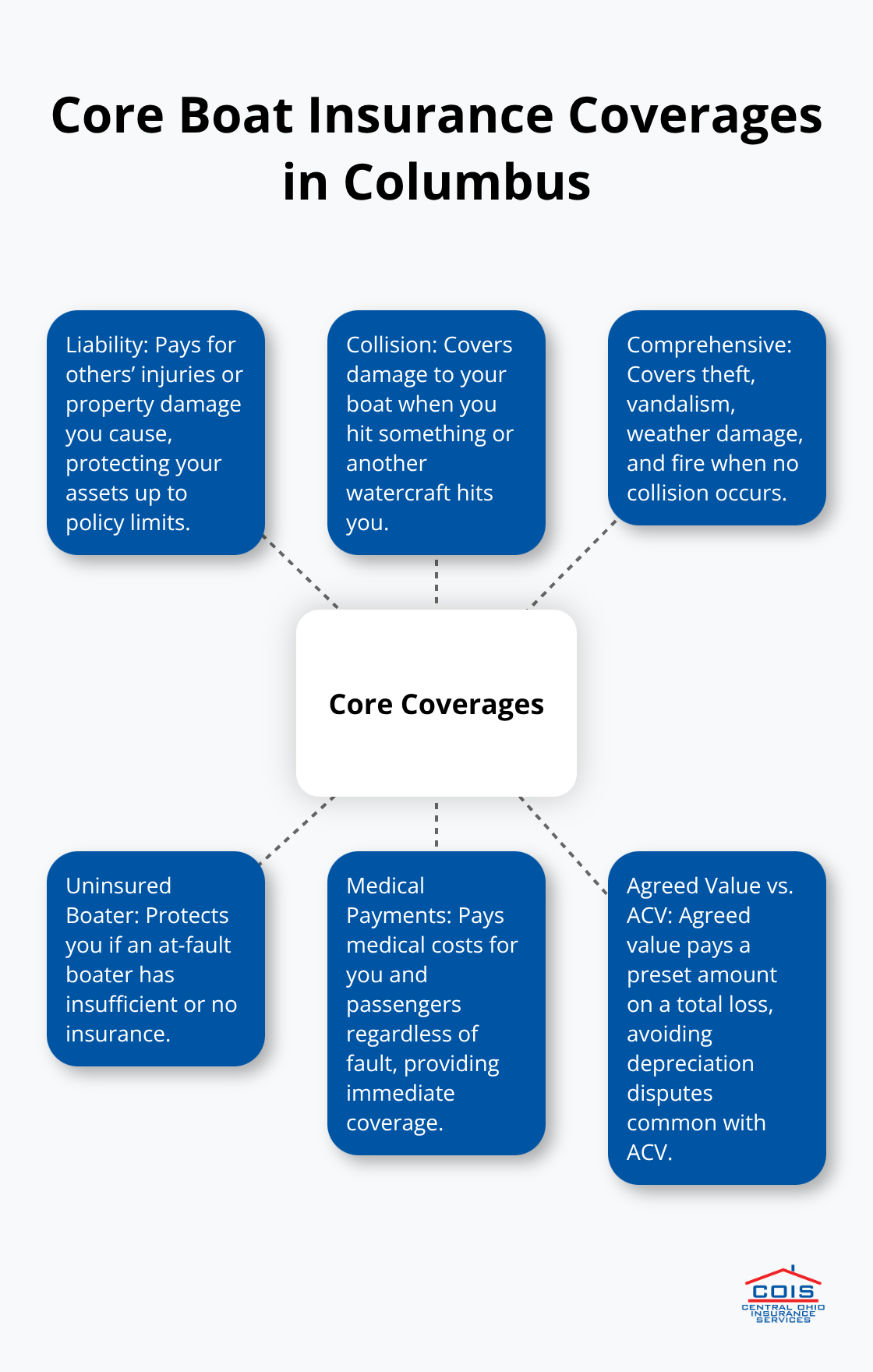

Coverage That Actually Protects Your Boat in Columbus

Most Columbus boaters carry too much of the wrong coverage and too little of what actually matters. We at Central Ohio Insurance Services, Inc. see this pattern repeatedly when boaters shop policies without understanding what each component does. Liability coverage is the foundation because it protects you when you damage someone else’s boat, property, or injure another person. If you hit another watercraft and cause $50,000 in damage, your liability coverage pays for repairs and medical costs up to your policy limit, not your personal assets. Ohio doesn’t legally require boat insurance in most cases, but if you financed your boat or dock at a marina, the lender or marina will demand liability coverage as a condition of their agreement.

Collision and Comprehensive: Protecting Your Own Boat

Collision and comprehensive coverage protects your own boat from damage. Collision pays for damage when you hit something or something hits you, while comprehensive covers theft, vandalism, weather damage, and fire. Most boaters underestimate how often comprehensive claims happen in Ohio-winter storms, hail, and theft from marinas are common threats that collision won’t address. The real decision point comes down to your boat’s age and value. A 2015 pontoon boat worth $40,000 absolutely needs both collision and comprehensive because replacement costs would devastate your finances. A 1998 fishing boat worth $8,000 might justify dropping comprehensive if you store it securely at home, but collision still matters because a single accident could exceed the boat’s value.

Uninsured Boater Coverage: Your Safety Net

Uninsured boater coverage protects you when another boater hits you and carries insufficient insurance or none at all. This is the coverage most boaters forget about entirely, yet it’s one of the most practical additions available. If an uninsured jet ski operator crashes into your boat causing $15,000 in damage, their lack of insurance becomes your problem unless you carry uninsured boater protection. In Ohio’s busy waterways around Columbus, where recreational boating traffic is high during summer months, this coverage pays for itself within a single claim scenario. The difference between a $400 annual premium and a $425 premium often comes down to whether you add uninsured boater coverage-the extra $25 per year is genuine insurance wisdom, not an unnecessary add-on.

Medical Payments and Agreed Value Coverage

Medical payments coverage protects you and your passengers regardless of who caused an accident. Coverage typically ranges from $500 to $10,000 per person and covers medical expenses immediately after an incident without waiting for liability determinations. If a passenger gets injured boarding your boat and needs emergency care, medical payments coverage covers those costs without anyone having to prove fault first. When you compare quotes from multiple carriers, ask specifically about agreed value versus actual cash value for your hull coverage. Agreed value pays the amount you both settled on at policy purchase if your boat is totaled, avoiding depreciation disputes that plague actual cash value policies. A boat that cost $50,000 five years ago might only be worth $30,000 today, but if you purchased agreed value coverage at $45,000, that’s what you’ll receive in a total loss. This distinction matters enormously for boats that hold value well, like quality fishing boats and sailboats.

Equipment and Environmental Coverage

Personal effects coverage and unattached equipment coverage are worth examining based on your specific boating style. If you regularly carry expensive fishing equipment, scuba gear, or water sports equipment, personal effects coverage protects these items up to stated limits. Many boaters assume homeowners insurance covers gear on the boat-it typically doesn’t, or covers only a fraction of the value. Fuel spill liability and wreckage removal coverage address environmental cleanup costs if your boat sinks or leaks fuel into the water. Ohio’s environmental regulations make you responsible for cleanup costs, which can reach thousands of dollars for significant spills. This coverage is inexpensive to add and protects you from devastating liability exposure.

Start with liability as your mandatory foundation, add collision and comprehensive based on your boat’s age and value, then layer in uninsured boater protection because it’s affordable and genuinely protects against real risks in Columbus’s boating environment. Everything else becomes optional based on how you actually use your boat and what equipment you carry.

Final Thoughts

Affordable boat insurance in Columbus requires action, not luck. Bundling policies, adjusting your deductible to match your financial situation, and completing a boating safety course cut your premiums by 35 to 50 percent without leaving you underprotected on the water. Your coverage foundation matters more than your premium amount-liability protects your assets when you damage someone else’s boat or property, while collision and comprehensive protect your own vessel based on its age and value.

Shopping quotes from multiple carriers reveals dramatic price differences for identical coverage. One carrier might quote $600 annually while another charges $850 for the same boat and limits, making comparison shopping the fastest way to find genuine value. Contact Central Ohio Insurance Services, Inc. to discuss your specific boating situation and receive personalized quotes from multiple carriers in your area.

Your licensed team explains your options in plain language, handles the paperwork, and provides ongoing support if you file a claim. Getting your quote takes minutes and costs nothing, so start today and see exactly how much you can save on quality boat insurance.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.