Boat owners in Ohio often overlook critical coverage gaps that leave them exposed to significant financial risk. At Central Ohio Insurance Services, Inc., we’ve seen firsthand how the right boat insurance requirements Ohio protects your investment and keeps you safe on the water.

Many boat owners assume basic coverage is enough, but Ohio’s waterways demand more comprehensive protection than most realize. This guide walks you through everything you need to know about adequate boat insurance.

What Ohio Law Actually Requires for Boat Insurance

Ohio does not mandate boat insurance by state law, but this legal freedom masks a dangerous assumption many boat owners make. The moment you finance a boat or dock it at a marina, lenders and facilities may impose their own requirements, typically demanding liability coverage. We recommend treating these lender requirements as a baseline, not a ceiling. Liability coverage protects you when you cause injury or property damage to others on the water-and Ohio’s busy waterways on Lake Erie, the Ohio River, and inland lakes mean collision risks are real.

Understanding Ohio’s Cost Reality

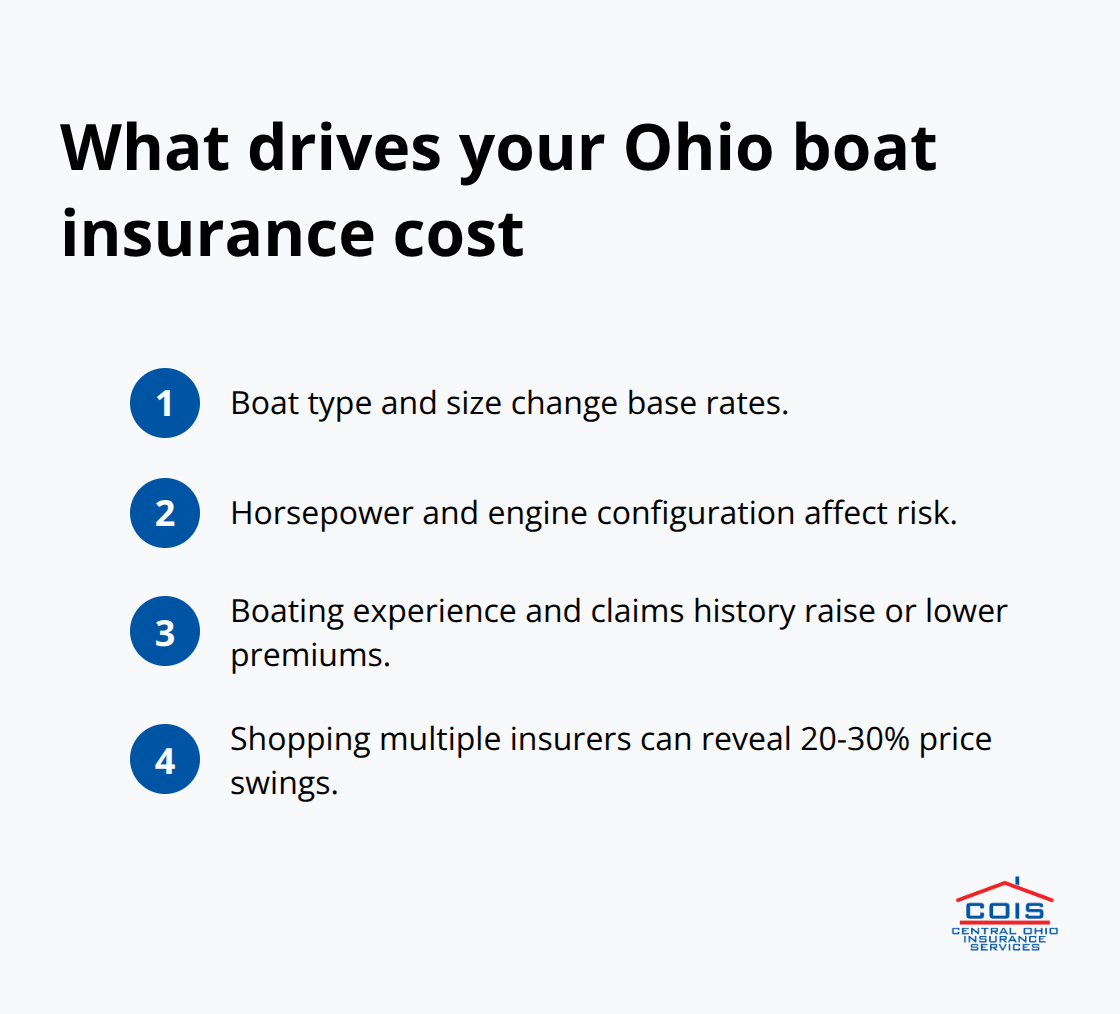

The average boat insurance cost in Ohio runs about $304.70 annually through Progressive, though liability-only policies start around $100 per year, making basic protection affordable for most boat owners. Your specific costs depend on boat type, horsepower, engine configuration, boating experience, and claims history, so comparing quotes across carriers matters significantly. Boat owners who shop multiple insurers typically find 20-30% variations in annual premiums for identical coverage, which means a few hours of comparison work can save hundreds of dollars.

Core Coverage That Protects Your Investment

Liability coverage is non-negotiable because a serious accident can expose your personal assets. Comprehensive coverage handles theft, vandalism, fire, weather damage, and animal collisions-critical protections given Ohio’s storm season and boat theft risks. Collision coverage pays for damage when you hit another boat, dock, or object, which happens far more often than owners expect. Medical payments coverage protects you and passengers regardless of fault, covering injuries that liability alone won’t address.

Additional Protections Worth Considering

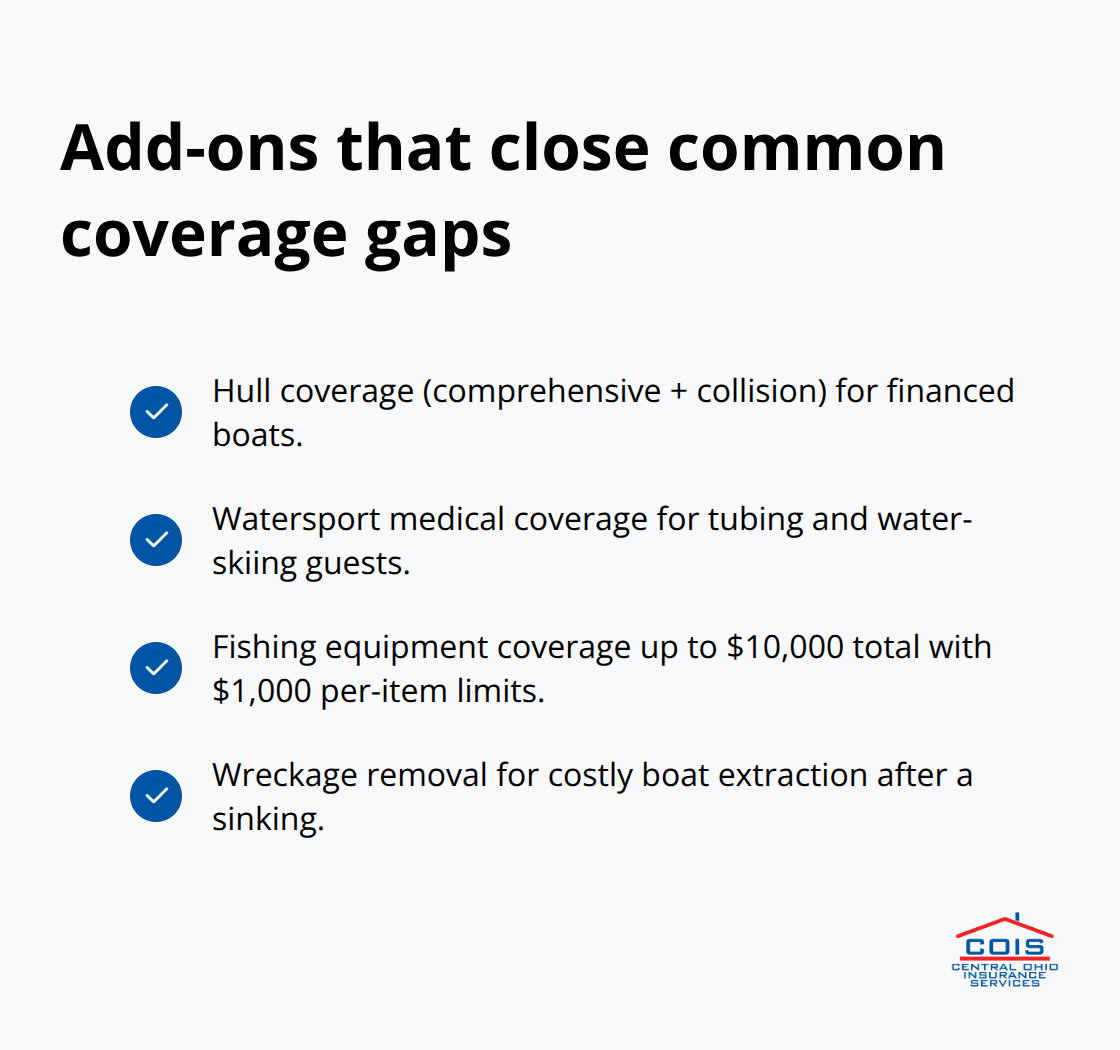

If you financed your boat, your lender almost certainly requires hull coverage (comprehensive and collision combined) to protect their investment, and you should maintain it anyway. Optional add-ons like watersport coverage pay medical expenses for guests injured during tubing or water-skiing, while fishing equipment coverage protects tackle and gear up to $10,000 with a $1,000 per-item limit. Wreckage removal coverage handles the cost of extracting a sunken boat from the water-an expense that can reach thousands without insurance backing.

Maximizing Your Savings Through Bundling

Multi-policy bundling with your auto or homeowners coverage typically saves 15-25% on boat insurance, making it worth consolidating if you already insure other assets with the same carrier. Many Ohio boat owners overlook this discount opportunity, paying full rates when they could reduce their total insurance costs significantly. Your independent agent can identify which carriers offer the best bundling discounts for your specific situation and help you structure policies to maximize savings.

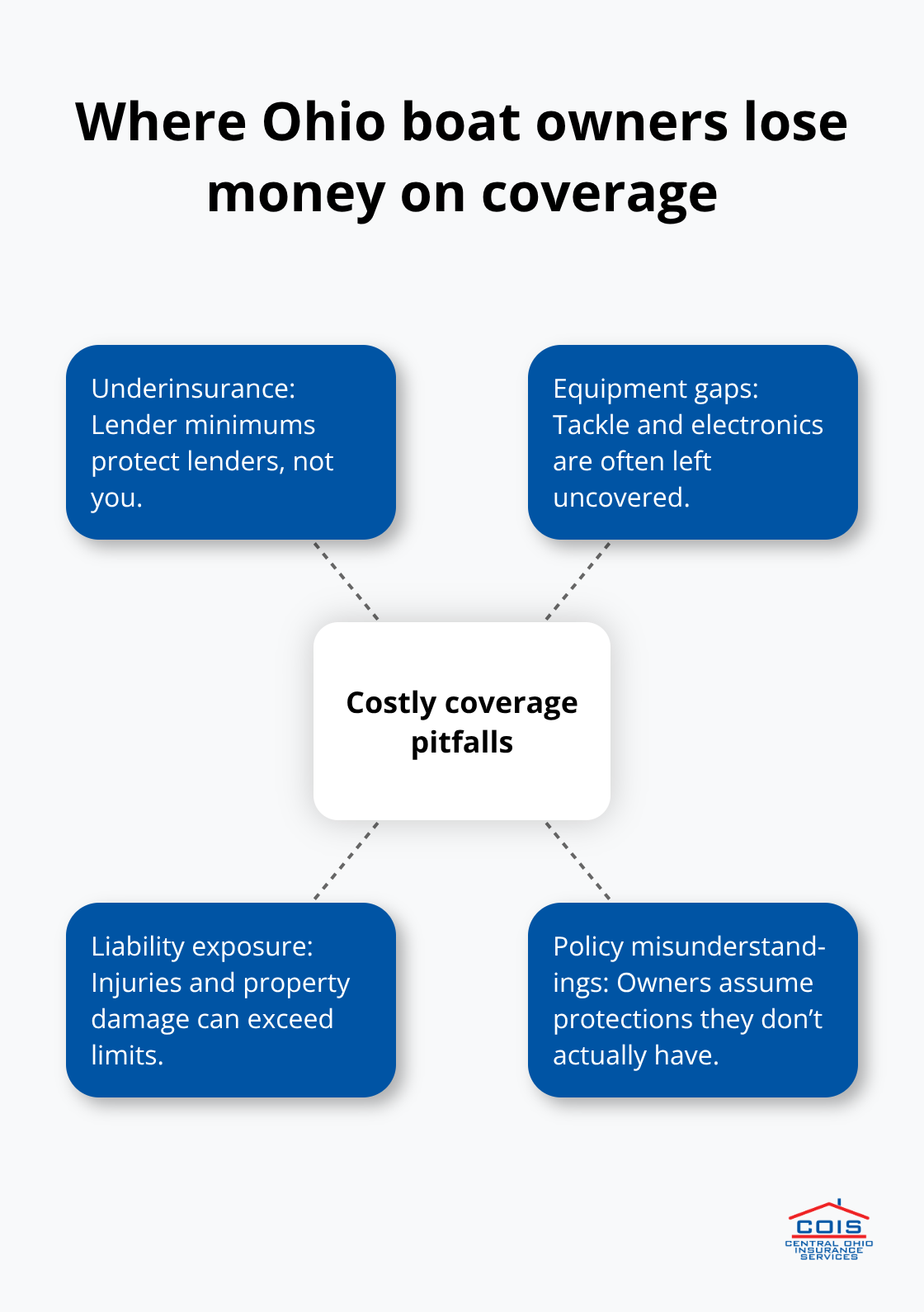

Where Boat Owners Actually Lose Money on Coverage

The Underinsurance Trap Most Owners Fall Into

Most Ohio boat owners carry insurance, but they carry the wrong kind. The gap between what owners think they have and what they actually have creates financial exposure that can exceed the boat’s value itself. Underinsurance happens because boat owners often accept whatever coverage their lender requires without understanding that lender minimums exist to protect the lender’s investment, not yours.

If you financed a $40,000 boat and your lender requires only liability coverage with $100,000 limits, you face $40,000 in personal loss if your boat sinks or burns. Progressive data shows that boats valued between $25,000 and $75,000 represent the largest underinsurance segment because owners assume comprehensive and collision coverage costs prohibitively more than it actually does. In reality, adding hull coverage to a liability-only policy typically costs less than most owners expect, yet many skip it thinking they’re saving money when they’re actually gambling with tens of thousands of dollars.

Equipment Protection Gaps That Drain Your Wallet

Equipment protection exposes another massive gap. Fishing boats especially suffer from this oversight because owners insure the hull but leave tackle, electronics, and specialized gear completely vulnerable. Standard boat policies cover fishing equipment up to $10,000 total with a $1,000 per-item limit, but many Ohio boat owners never read that fine print and discover the limit too late after a theft.

Electronics like GPS units, fish finders, and radar systems get stolen constantly from boats docked at marinas, and replacing a quality navigation system costs $3,000–$8,000. A single theft can wipe out your equipment coverage limit, leaving you to pay out of pocket for replacements. This oversight costs boat owners thousands annually across Ohio’s marinas and launch ramps.

Liability Exposure That Exceeds Your Expectations

Liability exposure on the water extends far beyond what most owners grasp because a single serious accident creates claims that exceed your policy limits. If a guest on your boat suffers injury during water-skiing and requires ongoing medical care costing $500,000, standard medical payments coverage maxes out at $5,000, leaving you personally liable for $495,000.

Ohio’s busy waterways mean collision risks are genuine, not theoretical, and a collision with another boat results in damage claims from both your boat and the other vessel, potentially exceeding $100,000 combined. Your liability policy should carry at least $300,000 in bodily injury coverage and $100,000 in property damage coverage if you regularly have guests aboard or operate in high-traffic areas like Lake Erie. These higher limits cost far less than most owners expect and protect your personal assets from catastrophic claims.

Taking Action Before an Accident Happens

The financial consequences of inadequate coverage hit hardest after an accident occurs, when you cannot adjust your policy retroactively. An independent agent can review your current coverage and identify gaps that expose you to personal liability. Central Ohio Insurance Services, Inc. helps boat owners across the region structure policies that match their actual risk exposure rather than just meeting lender minimums.

Your next step involves comparing what your current policy actually covers against what you think it covers-a conversation that takes minutes but can save you hundreds of thousands of dollars.

Getting the Right Coverage Without Overpaying

Shop Multiple Carriers to Find Real Savings

Comparing boat insurance quotes across multiple carriers reveals the uncomfortable truth that identical coverage can cost 20-30% more with one insurer than another. Accepting the first quote you receive likely costs you hundreds of dollars annually. We at Central Ohio Insurance Services, Inc. recommend obtaining quotes from at least three carriers before committing to any policy because boat insurance pricing varies dramatically based on how each company assesses risk factors like boat type, size, age, engine power, location, usage, and your boating experience.

When you request quotes, specify exactly the same coverage limits and deductibles across all quotes so you’re comparing apples to apples rather than making assumptions about which policy offers better value. An independent agent shops carriers on your behalf and identifies which companies offer the lowest rates for your specific boat and boating profile, saving you the legwork of contacting five different insurers individually.

Leverage Local Knowledge for Ohio-Specific Rates

Independent agents understand regional factors that directly impact Ohio boat insurance costs, such as Lake Erie’s notorious weather patterns and the theft risks associated with specific marinas. This local expertise allows them to recommend coverage levels that match actual conditions rather than generic national standards. Your agent can explain why a boat stored at a particular marina costs more to insure than one stored at another location just miles away, information that national online quote tools never provide.

Consolidate Policies to Unlock Hidden Discounts

Bundling your boat insurance with auto coverage options and homeowners policies typically delivers 15-25% savings across your entire insurance portfolio, yet many Ohio boat owners maintain policies with different carriers and leave hundreds of dollars in annual discounts unclaimed. When you consolidate with a single carrier, that company has greater incentive to retain your business and often extends loyalty discounts beyond the standard multi-policy reduction. A few minutes of conversation with your agent reveals exactly how much you save by moving all your policies to one carrier.

Update Your Coverage as Your Situation Changes

After you establish adequate coverage, you must review your policy annually to prevent your insurance from becoming outdated as your boat ages, your boating habits change, or your financial situation improves. If you upgraded from a fishing boat to a larger cruiser, your old policy limits may no longer match your boat’s actual value, and an annual review catches these gaps before they create problems. Your coverage should evolve with your changing needs rather than staying frozen in whatever you selected years ago.

Final Thoughts

Boat insurance requirements in Ohio don’t mandate state coverage, but the financial consequences of inadequate protection far exceed what proper coverage costs. Liability exposure, underinsurance, and equipment gaps combine to create financial disasters that responsible boat owners prevent through deliberate planning. The gaps we’ve outlined throughout this guide represent real money leaving your pocket after accidents happen, when adjusting your policy becomes impossible.

Your next move involves three concrete actions: contact an independent agent to review your current policy against the coverage standards we’ve discussed, request quotes from multiple carriers using identical coverage specifications so you can compare actual costs, and consolidate your boat insurance with your auto and homeowners policies to capture the 15-25% bundling discounts that most Ohio boat owners leave unclaimed. Local expertise matters because regional factors directly impact your boat insurance costs and coverage needs, and an agent familiar with Lake Erie’s weather patterns and Ohio’s marina theft risks understands risk factors that national online quote tools completely miss. This knowledge translates into coverage recommendations that protect your actual situation rather than generic national standards.

We at Central Ohio Insurance Services, Inc. help boat owners across Ohio structure policies that match their real risk exposure rather than just meeting lender minimums. Contact Central Ohio Insurance Services, Inc. to review your boat insurance and eliminate the coverage gaps that expose you to financial risk on the water.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.