Condo ownership in Columbus comes with unique insurance needs that differ significantly from traditional homeowners coverage. When you’re shopping for Columbus condo insurance quotes, understanding what to look for in a shared building is essential to protecting your investment.

At Central Ohio Insurance Services, Inc., we help condo owners navigate these complexities and find the right coverage for their specific situation. This guide walks you through the key differences, coverage elements, and cost factors that matter most.

Why Your Condo Quote Looks Different from a House Policy

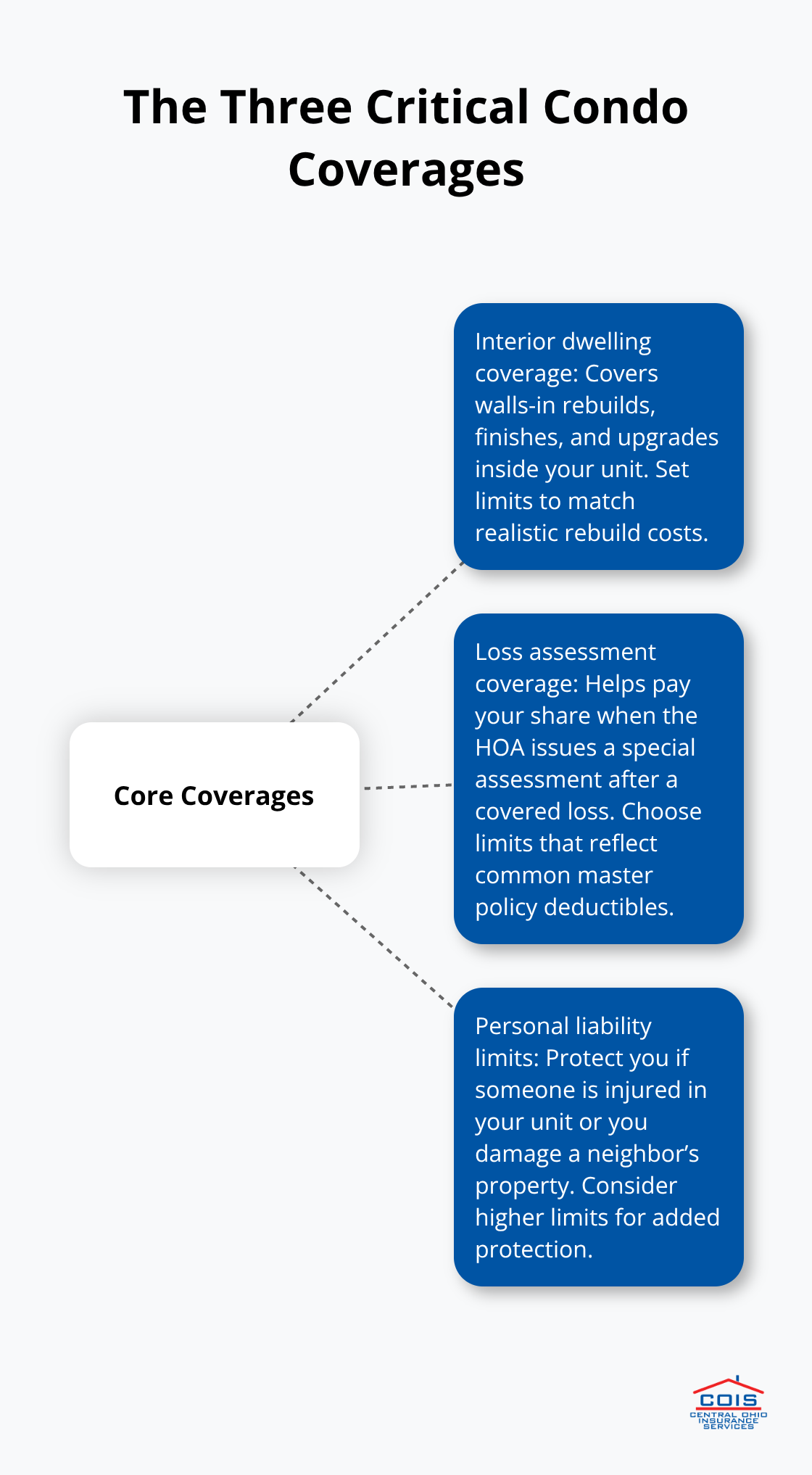

Condo insurance in Columbus operates under fundamentally different rules than a traditional homeowners policy, and this distinction directly impacts your coverage and costs. The core difference centers on what gets covered where: a condo association’s master policy handles the building’s exterior, common areas, and structural elements, while your individual HO-6 policy covers everything inside your unit walls plus your personal liability. This split responsibility means you cannot rely solely on the association’s coverage. According to data from Insure.com, the average Columbus condo owner pays around $574 per year for HO-6 coverage, which reflects the specific risks of unit ownership in a shared building. Your policy must protect interior improvements like drywall, cabinets, flooring, and fixtures that the master policy typically does not cover under bare walls coverage (the most common master policy type in Ohio). This division prevents dangerous gaps: if the association’s policy hits its deductible after storm damage to the building, the association may assess owners for the out-of-pocket cost, which is precisely where loss assessment coverage in your HO-6 becomes critical.

Interior Coverage Starts Where the Master Policy Stops

The master condo policy covers shared amenities, parking lots, lobbies, elevators, hallways, and the building’s structural shell. Your HO-6 policy must cover the interior space, personal belongings, and any upgrades you have made within your unit. Interior rebuild costs for an Ohio condo typically run $30,000 to $80,000 depending on unit size and finishes, so your personal property and dwelling limits need to reflect this reality rather than guessing. If your building experienced a major loss, the association policy would handle exterior repairs and common area restoration, but you would be responsible for your interior restoration costs up to your HO-6 limits. Many Columbus condo owners underestimate this exposure and carry insufficient dwelling coverage, which leaves them facing out-of-pocket losses.

Loss Assessment Coverage Protects Against Hidden Costs

Loss assessment coverage is an optional protection you can add to your condo or homeowners insurance to help pay for special assessment fees. When the association’s master policy covers a loss but the deductible exceeds available reserves, the association typically levies a special assessment against all owners to cover that gap. Standard loss assessment coverage often includes only $1,000 of protection, which is insufficient for most Columbus buildings; bumping this to $10,000 or $25,000 costs only a few dollars more per month and provides realistic protection against these assessments. Ohio Revised Code Section 5311 requires the condo association to maintain adequate liability and property insurance, but gaps between policy limits and actual damage costs fall to owners through assessments.

Personal Liability in Shared Settings Works Differently

Your personal liability coverage protects you when someone is injured at your condo or you cause damage to another unit. In a shared building, this risk is higher than in a single-family home because more people live in close proximity and accidents involving water damage to neighbors’ units are common. Standard liability limits of $100,000 to $300,000 are typical starting points for Columbus condos, though higher limits may be warranted if your unit has significant value or amenities. When you compare quotes from different carriers, pay close attention to how each one structures these three elements-interior coverage, loss assessment protection, and personal liability limits-because the differences directly affect both your premium and your actual protection.

What to Prioritize When Comparing Your Columbus Condo Quote

Interior Dwelling Coverage Must Match Your Rebuild Costs

When you pull quotes from different carriers for your Columbus condo, interior dwelling coverage is where most owners make their first mistake. Your HO-6 policy needs to cover the cost of rebuilding your unit’s interior from the walls inward. The problem is that many quotes show a $40,000 dwelling limit because that’s the default, not because it matches your actual rebuild costs. You need to physically assess your unit and estimate what it would cost to replace your drywall, flooring, cabinetry, and fixtures if a fire destroyed everything inside. If your building has bare walls coverage (the most common type in Ohio), you’re responsible for all of this. Get three contractor estimates or use online rebuild calculators specific to Columbus, then adjust your dwelling limit to actually cover that number rather than accepting the default.

Personal Property Coverage Requires a Real Inventory

Personal property coverage on your quote covers your furniture, electronics, clothing, and everything else you own. Most quotes default to $40,000 or $60,000, but Insure.com data shows that increasing from $40,000 to $60,000 in personal property typically costs only $80 to $100 more annually. You should conduct a room-by-room inventory of your belongings-open your closets, check your kitchen, count your electronics-and add up the replacement cost. Most Columbus condo owners discover they need more coverage than they initially thought once they actually count what they own. This simple exercise prevents you from facing significant out-of-pocket losses after a covered loss.

Loss Assessment Coverage Protects Your Finances from Special Assessments

Loss assessment coverage is where your real financial protection lies, and it’s the coverage that most condo owners either skip or dramatically underestimate. When the condo association’s master policy covers a loss but the deductible is $10,000 or $25,000, the association bills owners for that gap through a special assessment. Standard loss assessment coverage includes only $1,000, which means you could face a $9,000 to $24,000 bill out of pocket. Upgrading to $10,000 or $25,000 in loss assessment coverage costs only $3 to $8 more per month according to Insure.com’s rate analysis, making this one of the best value upgrades available. This single addition to your policy protects you from unexpected financial shocks that most condo owners don’t anticipate.

Water Damage and Flood Protection Depend on Your Location

Standard HO-6 policies cover water damage from burst pipes or roof leaks, but they exclude flood damage from rising water, heavy rain overflow, or saturation from external sources. If your unit is on a ground floor, near a creek, or in an area with known drainage issues, standalone flood insurance through the National Flood Insurance Program costs roughly $400 to $600 annually and covers what your standard policy won’t. This coverage becomes essential rather than optional if your location carries elevated water risk.

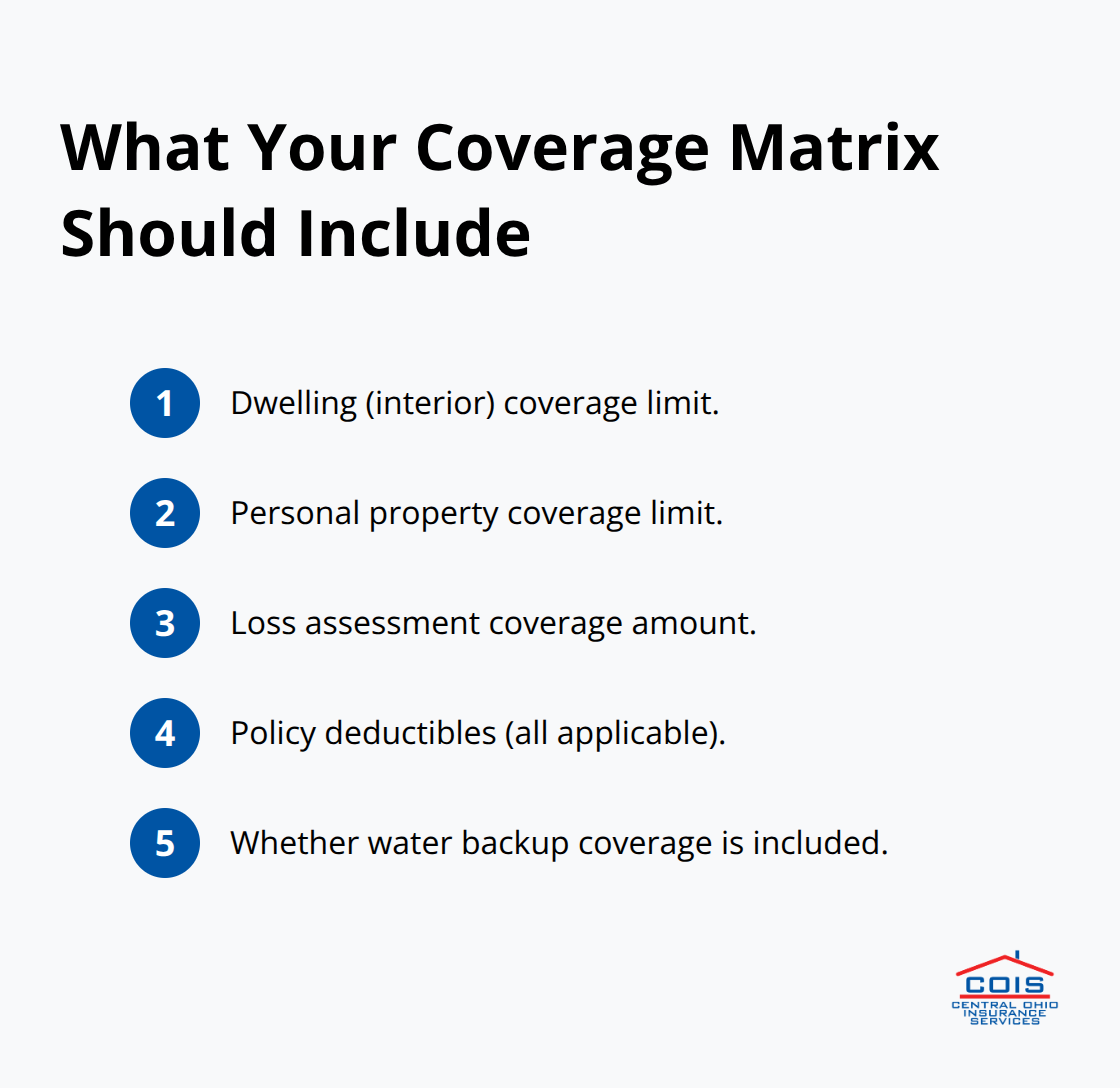

Request a Coverage Matrix to Compare Quotes Accurately

When you compare quotes across carriers, request a coverage matrix from each one that lists dwelling limits, personal property limits, loss assessment coverage, deductible amounts, and whether water backup coverage is included. This matrix makes it simple to compare apples to apples instead of getting confused by different presentation formats.

Don’t accept the default limits on any quote-adjust them to match your actual situation, then compare the adjusted quotes across carriers. Once you’ve identified the right coverage levels for your specific unit and situation, you’re ready to evaluate the cost factors that drive premium differences between carriers.

What Actually Drives Your Columbus Condo Insurance Premium

Building age and construction materials separate affordable quotes from expensive ones, and Columbus carriers price these differences aggressively. A condo built in 1995 with brick exterior and modern electrical systems costs substantially less to insure than a 1970s building with original wiring and wood-frame construction, because older buildings carry higher fire and water damage risk. When you request quotes, carriers pull your building’s year of construction and exterior material from public records, then apply their underwriting guidelines to determine baseline pricing. If your building is pre-1980 with wood framing or aluminum wiring, expect your quote to reflect a 15 to 25 percent premium over comparable newer buildings in Columbus. This reflects actual claims data showing that older buildings file more frequent and costlier claims. The construction material also affects wind and hail deductibles significantly; insurers tightened wind deductible requirements and roof depreciation practices statewide following severe weather events.

Roof Condition Matters More After Recent Storm Activity

Carriers now scrutinize roof condition and material more closely during quotes. Request your building’s roof age and material from the HOA when you shop quotes, because this single detail can swing your premium by $50 to $150 annually. A newer roof with impact-resistant shingles qualifies for better rates than an aging roof with standard asphalt shingles, especially in Ohio’s current underwriting environment.

Your Claims History Determines Pricing More Than You Realize

Your personal claims history over the past five years directly affects your condo insurance quote, and one prior claim can increase your premium by 10 to 25 percent depending on the carrier and claim type. When you request quotes online or from an agent, disclose any water damage, theft, or liability claims filed on your current or previous policies. Carriers also check the association’s claims history through CLUE reports (Comprehensive Loss Underwriting Exchange), meaning even if you personally filed no claims, frequent claims by other unit owners at your building can raise everyone’s premiums. Ask the HOA for a summary of recent claims during the quote process-if the building filed five claims in three years, expect higher quotes across all carriers.

Deductible Selection Affects Both Premium and Financial Risk

Your deductible choice directly impacts your quote cost, and this decision requires understanding your actual financial capacity. A $1,000 deductible costs roughly $574 annually for a typical Columbus condo according to Insure.com data, while a $2,500 deductible can reduce that premium by $60 to $100 per year. Choose a deductible you can actually afford to pay out of pocket if a claim occurs; setting a $2,500 deductible to save $80 per year makes no sense if an unexpected $2,500 bill would strain your finances.

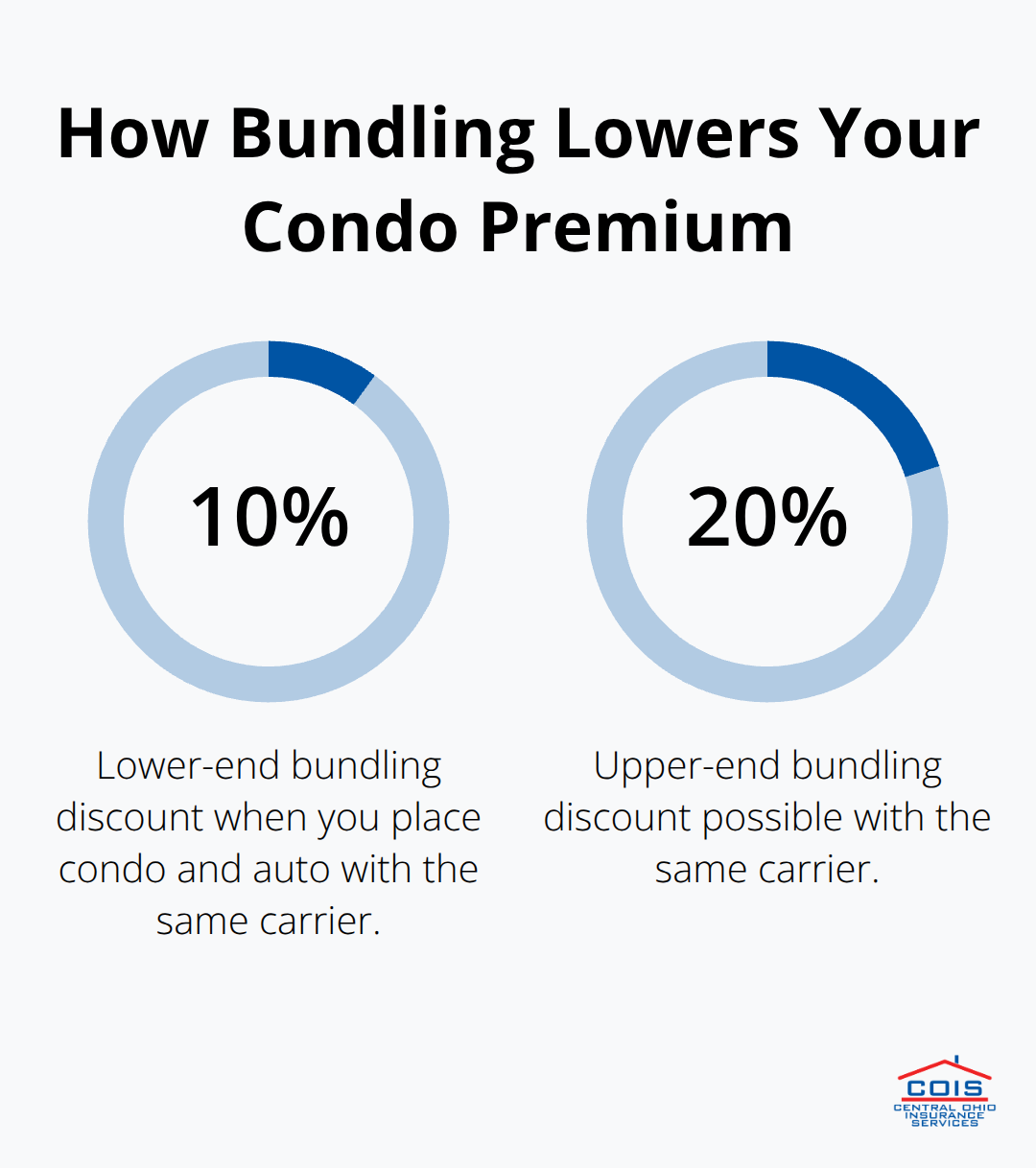

Bundling and Safety Features Cut Premiums Significantly

Bundling your condo insurance with auto insurance from the same carrier saves roughly 10 to 20 percent on your condo premium, making this the single most impactful discount available to Columbus condo owners. If you currently carry auto insurance with State Farm, Progressive, or Allstate, requesting a condo quote from that same carrier typically unlocks immediate savings that far exceed shopping for the lowest single-policy rate.

Water leak detection systems, smart home security devices, and monitored alarm systems qualify for additional discounts ranging from 5 to 15 percent depending on the carrier and specific equipment installed. If your unit lacks these systems, the cost of installing a water leak detector (around $50 to $150) pays for itself within the first year through insurance savings alone. Carriers like Nationwide and Amica actively market their condo discounts for bundling and safety features, but independent agents can access discount programs across multiple carriers and identify which combination saves you the most money on your specific situation. Request quotes that specify all available discounts before you compare final prices, because some carriers bury discounts while others apply them automatically.

Final Thoughts

Protecting your Columbus condo investment requires three essential coverage layers: interior dwelling protection that matches your actual rebuild costs, personal property coverage based on a real inventory of your belongings, and loss assessment protection that shields you from unexpected special assessments. These three elements form the foundation of adequate condo insurance, and skipping any one of them leaves you financially exposed. Water damage coverage and appropriate liability limits complete the picture for most Columbus condo owners.

Shopping for Columbus condo insurance quotes becomes straightforward once you know what to prioritize. Request coverage matrices from multiple carriers that show dwelling limits, personal property amounts, loss assessment coverage, and deductibles side by side, then adjust the default limits on each quote to match your unit’s actual rebuild costs and your belongings’ replacement value. This approach prevents you from overpaying for coverage you don’t need or underinsuring critical gaps.

A local independent agent makes this process faster and more accurate than shopping online alone. Agents at Central Ohio Insurance Services, Inc. shop multiple carriers simultaneously, identify all available discounts specific to your situation, and verify that your coverage meets Ohio Revised Code requirements and your HOA’s governing documents. Contact an independent agent to request quotes that reflect your actual interior rebuild costs and personal property needs, then select the policy that provides the coverage you need at a price that fits your budget.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.