Renting in Columbus means protecting what matters most-your belongings, your finances, and your peace of mind. Getting Columbus renters insurance quotes doesn’t have to be complicated, and the coverage is far more affordable than most renters realize.

At Central Ohio Insurance Services, Inc., we help renters find the right protection without the hassle. Let’s walk through what you need to know to make the smartest choice for your situation.

Why Renters Insurance Matters in Columbus

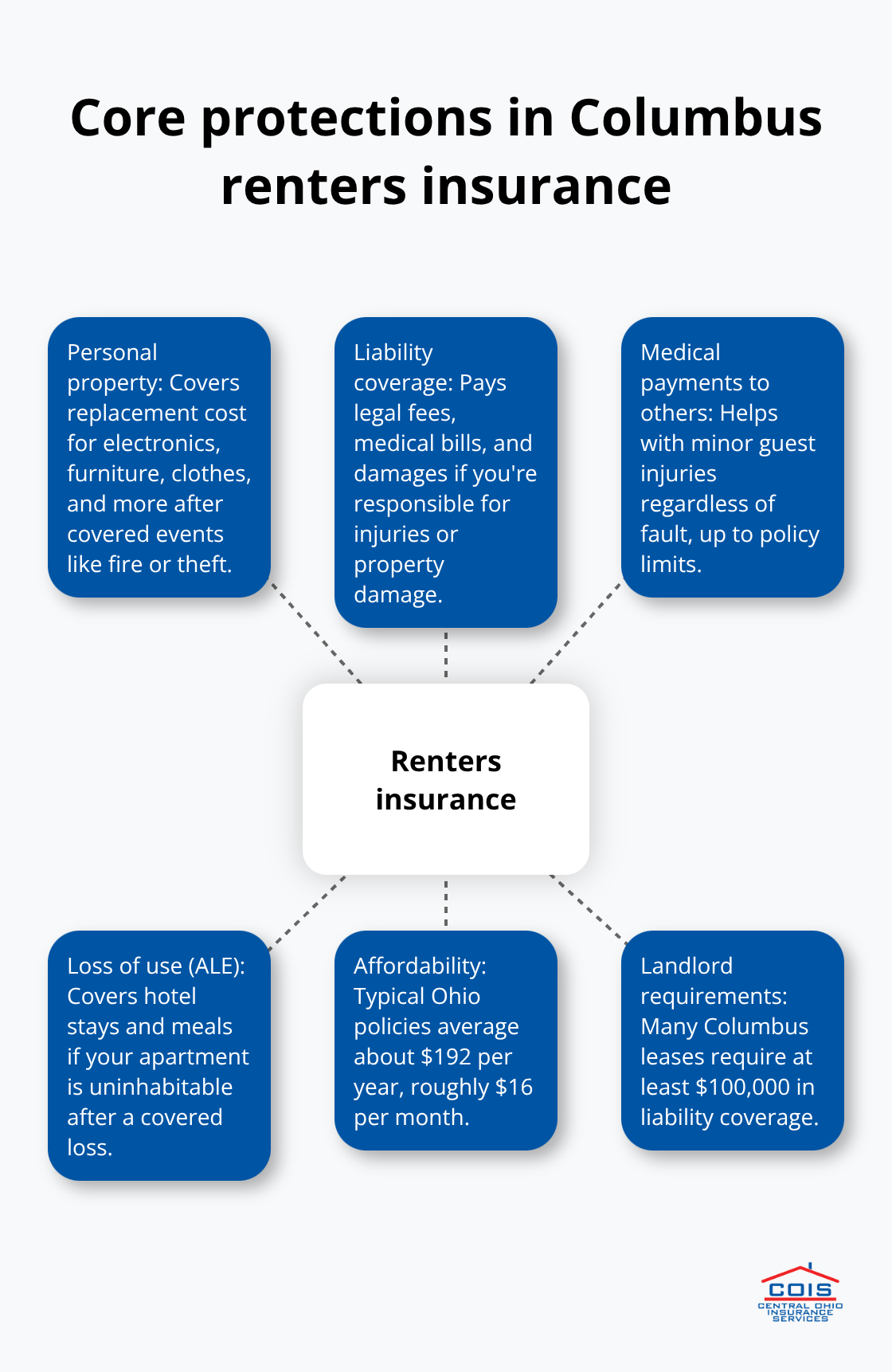

Your belongings in a Columbus rental add up faster than you think. Electronics, furniture, clothes, and personal items represent real money-often $20,000 to $50,000 worth. Standard renters insurance covers the replacement cost of these items if they’re damaged, stolen, or destroyed by a covered event like fire or theft.

The average cost of renters insurance in Ohio is $192 per year, which breaks down to about $16 per month. That’s genuinely affordable protection for everything you own. Without this coverage, you’d pay out of pocket to replace it all, which most renters simply can’t do.

Liability Coverage Protects You from Unexpected Lawsuits

Most renters overlook liability coverage, yet it’s one of the most valuable parts of your policy. If someone gets injured in your rental-a friend slips on your floor, your dog bites a visitor, or you accidentally damage a neighbor’s property-you could face a lawsuit for medical bills, legal fees, and damages. Standard renters insurance includes personal liability coverage, typically starting at $100,000, which covers these costs up to your policy limit. Many Columbus landlords actually require at least $100,000 in liability coverage as a lease condition, so you may not have a choice anyway.

Medical payments to others coverage, included in most policies, also pays for minor injuries on your property regardless of fault, up to your policy limits. This protects both you and your guests without anyone having to prove who was responsible.

Loss of Use Coverage Prevents Financial Crisis

If a fire, explosion, or other covered event makes your apartment uninhabitable, loss of use coverage pays for temporary housing and meals while repairs happen. This coverage typically equals 20 to 30 percent of your personal property limit, so with $20,000 in personal property coverage, you’d have $4,000 to $6,000 available for temporary lodging. Without it, you’d scramble to find affordable housing while your landlord handles repairs, draining your savings.

Columbus renters who’ve experienced apartment fires or water damage know this coverage prevents financial disaster during an already stressful situation. The cost to add this protection is minimal because it’s usually included automatically in most policies. Now that you understand what renters insurance covers, the next step is figuring out how much coverage you actually need and where to find the best quotes in Columbus.

How to Get Quotes That Actually Match Your Needs

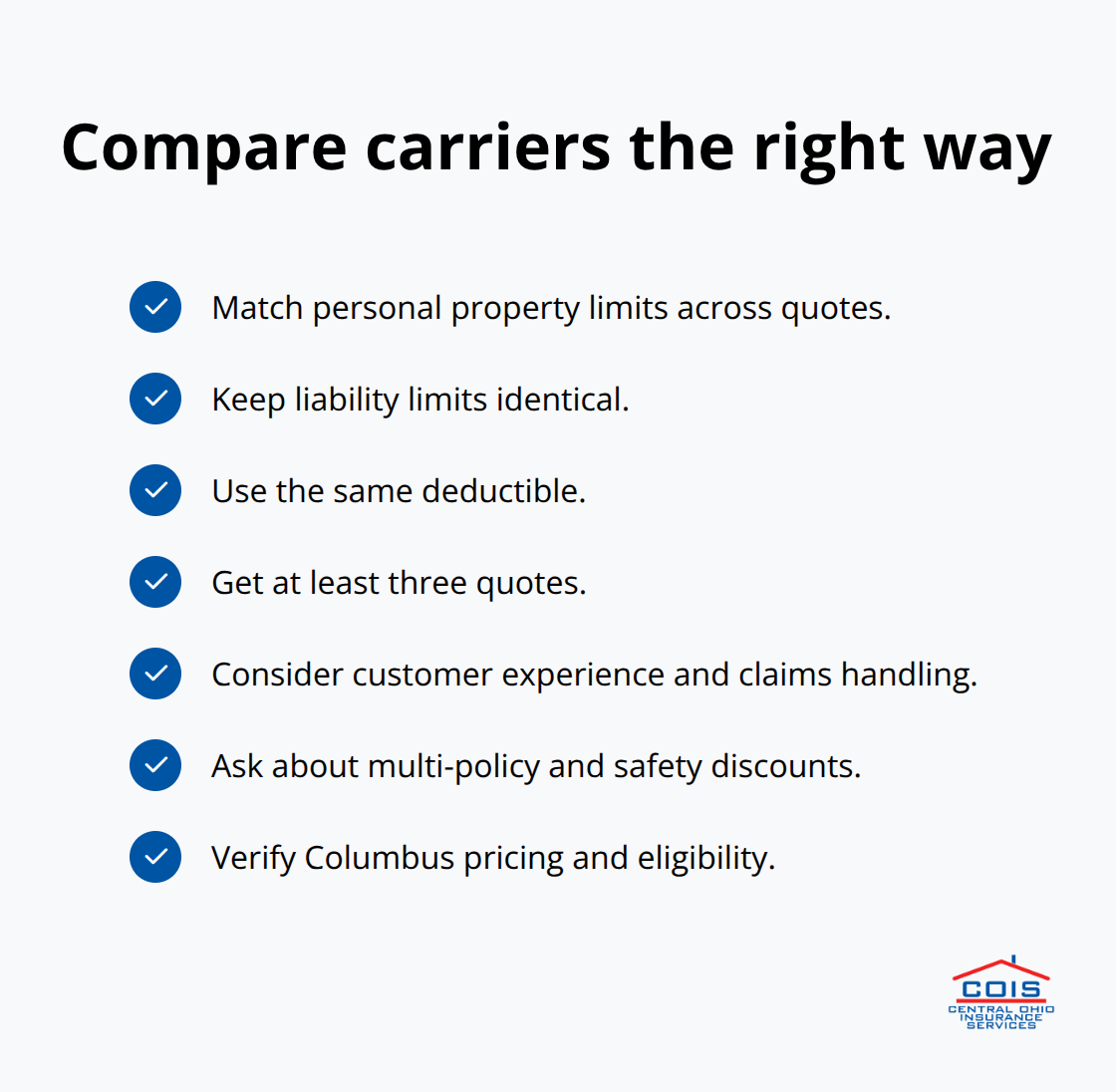

Getting renters insurance quotes in Columbus takes about 15 minutes online, but most renters waste hours comparing apples to oranges because they don’t understand what they’re looking at. The real speed comes from knowing exactly what coverage you need before you contact anyone. Walk through your apartment and estimate what your belongings are worth. Electronics, furniture, clothes, and kitchen items add up quickly-most Columbus renters need between $20,000 and $50,000 in personal property coverage. According to MoneyGeek data, a standard $20,000 personal property policy with $100,000 liability and a $500 deductible costs about $192 per year in Ohio, while Columbus specifically averages around $183 per year. If you increase that personal property limit to $50,000, expect roughly $322 per year. Taking 20 minutes to inventory your belongings before getting quotes means you’ll compare identical coverage across carriers instead of wasting time on policies that don’t fit your situation.

Your credit score matters far more than most renters realize. Someone with excellent credit pays around $127 per year while someone with poor credit pays roughly $933 for the same coverage, according to MoneyGeek. That $806 difference makes it worth checking your credit report before shopping.

Compare at Least Three Carriers Side by Side

Never get a quote from just one company. The difference between the cheapest and most expensive option in Columbus can exceed $100 per year for identical coverage. Grange offers the lowest rates in Ohio at about $110 annually for basic coverage, while Erie Insurance and State Farm consistently rank highest for customer experience and claim handling in Ohio. When you compare quotes, make sure each company quotes the same personal property limit, liability amount, and deductible-this is non-negotiable for accurate comparison.

Bundling your renters policy with auto insurance saves 10 to 25 percent according to MoneyGeek, so always ask about multi-policy discounts. Additional discounts for security systems, smoke detectors, and paying annually can reduce your premium further, though availability varies by carrier. An independent agent shops multiple carriers for every client, which means you’ll see side-by-side quotes and understand exactly what each policy includes and excludes. Working with a local agent saves you the guesswork of comparing dozens of policies on your own.

Get Your Quote Fast Without the Sales Pitch

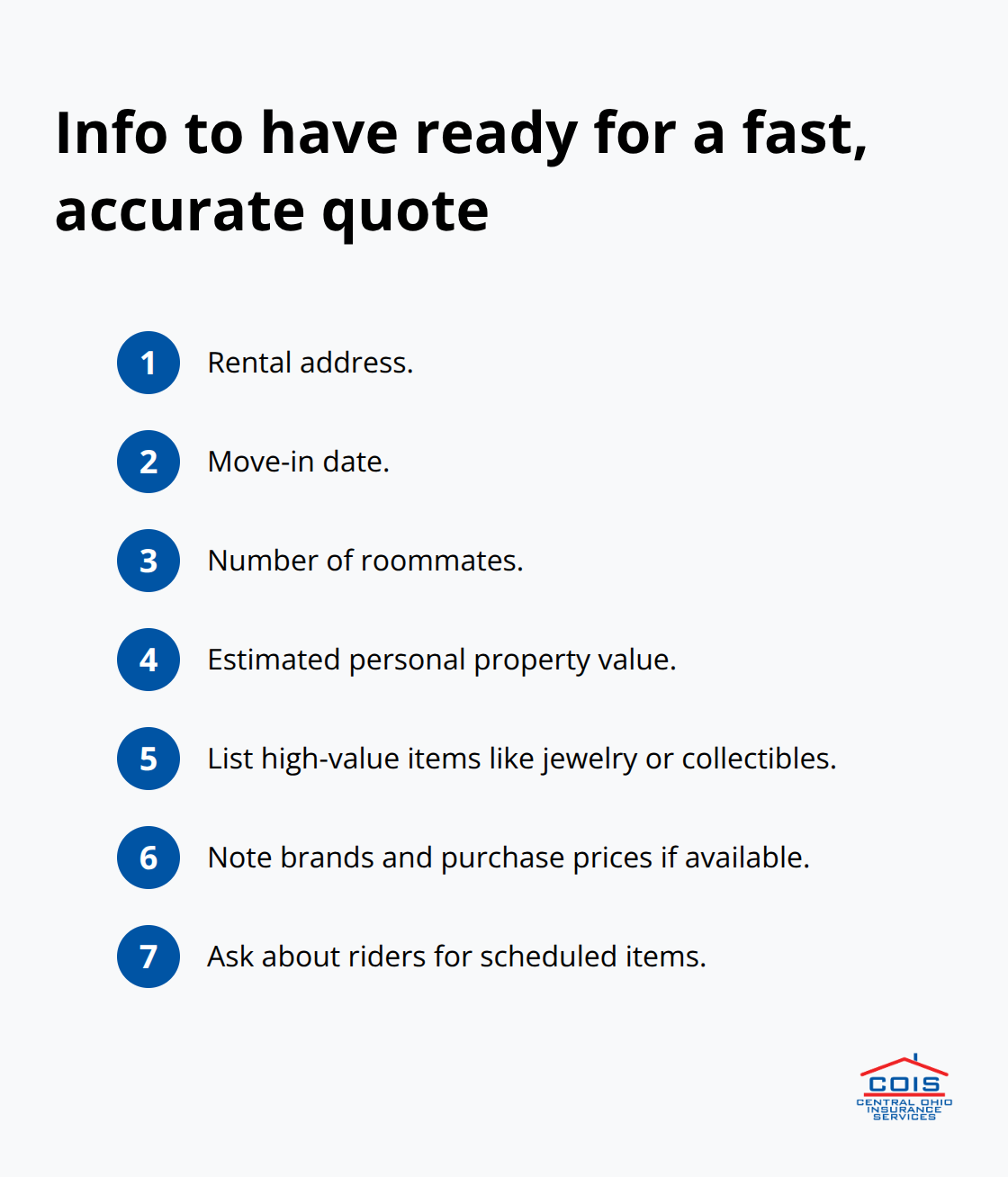

A legitimate Columbus insurance agent generates a complete renters insurance quote in under 10 minutes once you provide your basic information. You’ll need your rental address, the number of roommates, your move-in date, and your best estimate of personal property value. Most carriers process claims within two to four weeks, so don’t assume faster quotes mean faster claims-that’s a separate conversation.

When you call for a quote, ask directly whether the agent represents one company or multiple carriers. Single-company agents can’t show you competitive rates, while independent agents can present options from multiple insurers. This matters because your best rate might come from a carrier you’ve never heard of, and an agent working only for State Farm or Erie won’t tell you that. An independent agency like Central Ohio Insurance Services, Inc. shops multiple carriers to deliver competitively priced solutions with fast quotes and clear guidance.

Know What Information You’ll Need

Carriers ask for the same basic details, so prepare this information before you call. Your rental address, move-in date, number of roommates, and estimated personal property value speed up the quoting process significantly. If you have high-value items (jewelry, electronics, or collectibles), mention these upfront because they typically require riders or higher limits.

Having this information ready means you’ll get accurate quotes instead of rough estimates that change when you provide complete details.

Now that you understand how to gather quotes and what to compare, the next step is recognizing the mistakes that cost renters thousands of dollars in uncovered losses.

Common Renters Insurance Mistakes to Avoid

Underestimating What Your Belongings Actually Cost

Most Columbus renters drastically underestimate what their belongings are worth, and this mistake costs them thousands when a loss occurs. You walk through your apartment and think your furniture and electronics might total $10,000 or $15,000, but when you price replacement costs at retail, the number jumps to $30,000 or $40,000 quickly. A decent couch runs $1,500 to $3,000, a laptop costs $800 to $1,500, and a bedroom set easily exceeds $2,000. Electronics alone-your TV, computer, phone, tablet, gaming console, and kitchen appliances-often total more than $5,000 in replacement value.

Your renters insurance policy only covers what you actually insure, so if you underestimate and buy $20,000 in coverage when you own $35,000 worth of belongings, you’ll absorb the $15,000 difference out of pocket after a loss. MoneyGeek data shows that standard coverage in Ohio costs about $192 annually for $20,000 in personal property, while $50,000 in coverage runs roughly $322 per year. That extra $130 annually protects an additional $30,000 in belongings, which is genuinely inexpensive insurance against a catastrophic loss.

Walk through every room of your rental with your phone and photograph items, note brand names and approximate purchase prices, and add everything up before you call for quotes. GEICO’s personal property coverage calculator makes this process straightforward, helping you determine the right coverage amount for your belongings. This inventory prevents the heartbreak of discovering your coverage was $15,000 short when you file a claim.

Skipping Liability Coverage to Save a Few Dollars

Liability coverage gets skipped far too often because renters don’t think anyone will get hurt in their apartment, but accidents happen constantly and liability claims destroy finances fast. A visitor slips on your floor and breaks their leg, requiring surgery and months of physical therapy that costs $50,000 total. Without $100,000 in liability coverage, you’re personally responsible for the entire amount, which means wage garnishment, asset seizure, or bankruptcy.

Medical payments to others coverage, included in most policies, covers minor injuries regardless of fault, but serious claims require your liability limit to protect you. Columbus landlords frequently require $100,000 in liability coverage as a lease condition, so you probably need it anyway. Skipping this protection is false economy because the cost difference between a $50,000 liability limit and a $300,000 limit is minimal-maybe $20 to $30 annually-yet the protection difference is enormous.

Ignoring Your Policy After Major Life Changes

Many renters fail to review their policies annually after major purchases or life changes, which creates dangerous coverage gaps. You buy a new TV, laptop, and furniture, but your $20,000 personal property limit stays unchanged, leaving you underinsured again. Life events like adding a roommate, getting a dog, or starting a home-based business also change your coverage needs, but most renters never update their policies.

Set a calendar reminder on your phone to review your renters insurance every January and contact your agent whenever you make significant purchases or experience major changes in your living situation. This simple habit prevents you from discovering too late that your coverage no longer matches your actual situation.

Final Thoughts

Renters insurance protects your financial security in ways most people don’t fully appreciate until they experience a loss. A fire, theft, or water damage destroys everything you own, and without coverage, you pay thousands out of pocket to replace it all. The cost of Columbus renters insurance quotes averages around $183 per year for solid protection, yet it prevents financial catastrophe when accidents happen.

An independent agent shops multiple carriers at once, showing you competitive rates and explaining what each policy actually covers. You won’t waste hours comparing policies that don’t match, and you’ll understand exactly why one option costs more or less than another. A local agent answers your questions directly, handles your claims personally, and adjusts your coverage when your life changes-services that online quote tools simply can’t provide.

Contact Central Ohio Insurance Services, Inc. today to get your renters insurance quotes and protect what matters most. Our licensed team handles everything from initial quotes to claims support, so you’re never left figuring out policy details on your own.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.