Your prized 1967 Chevelle isn’t like the sedan parked next to it. Standard auto insurance treats all vehicles the same way, which means your collector car gets undervalued and restricted.

At Central Ohio Insurance Services, Inc., we know that Pickerington antique car insurance needs to be different. Your collection deserves coverage built specifically for how you actually use and maintain these vehicles.

Why Antique Cars Gain Value While Regular Cars Depreciate

Your 1967 Chevelle appreciates in value while a 2015 sedan loses thousands annually. This fundamental difference shapes everything about how you need to protect your investment. Antique cars, defined as vehicles at least 45 years old according to most state classifications, operate in an entirely different economic reality than everyday vehicles. A collector car appreciates because of rarity, condition, and historical significance-factors that standard auto insurance completely ignores. Standard policies use actual cash value, which calculates depreciation based on age and wear. For your Chevelle, that means the insurer might offer $8,000 when you’ve invested $45,000 in restoration. This valuation gap exists because standard carriers assume all vehicles lose value over time. Your antique car does the opposite, especially if you maintain it properly and store it in climate-controlled conditions.

How Your Driving Patterns Differ From Everyday Drivers

You don’t commute 40 miles daily on the highway. Most antique car owners drive fewer than 2,500 miles annually, often limiting use to car shows, weekend cruises, and special events. This dramatically reduces risk compared to someone who drives 12,000 miles yearly through traffic.

Standard auto insurance prices based on typical commuter patterns, not collector usage. A policy built for daily drivers overcharges you because it assumes high exposure. Cole’s Classics in Ohio and Hill’s Automotive both serve collectors who understand that their cars require specialized handling-these shops focus on meticulous restoration and maintenance, not quick repairs for daily damage. Your vehicle sits in secure storage much of the time, further reducing theft and accident risk. Standard carriers don’t account for this reality, which means you subsidize coverage for drivers with genuinely higher risk profiles.

Maintenance and Parts Create Unique Coverage Needs

Finding parts for your 1967 Chevelle means sourcing rare components that standard repair shops can’t obtain. You might need vintage-specific expertise that commands premium labor rates. Standard auto insurance covers damage, but it won’t pay what you actually spend on authentic restoration-quality repairs. Your car might need a specialty shop like Foreign Car Specialties in Ohio, which has served vintage British cars since 1972 with full frame-off restoration capability. These shops charge differently than chain mechanics because the work demands specialized knowledge. Coverage for spare parts matters too-if you keep original components on hand for restoration projects, standard policies won’t protect them. Antique car insurance recognizes that your maintenance approach involves preservation and authenticity, not just getting the vehicle roadworthy.

These realities point to a critical gap: standard coverage simply cannot address what makes your collection valuable. The next section explores how agreed value coverage and custom protection options fill that gap.

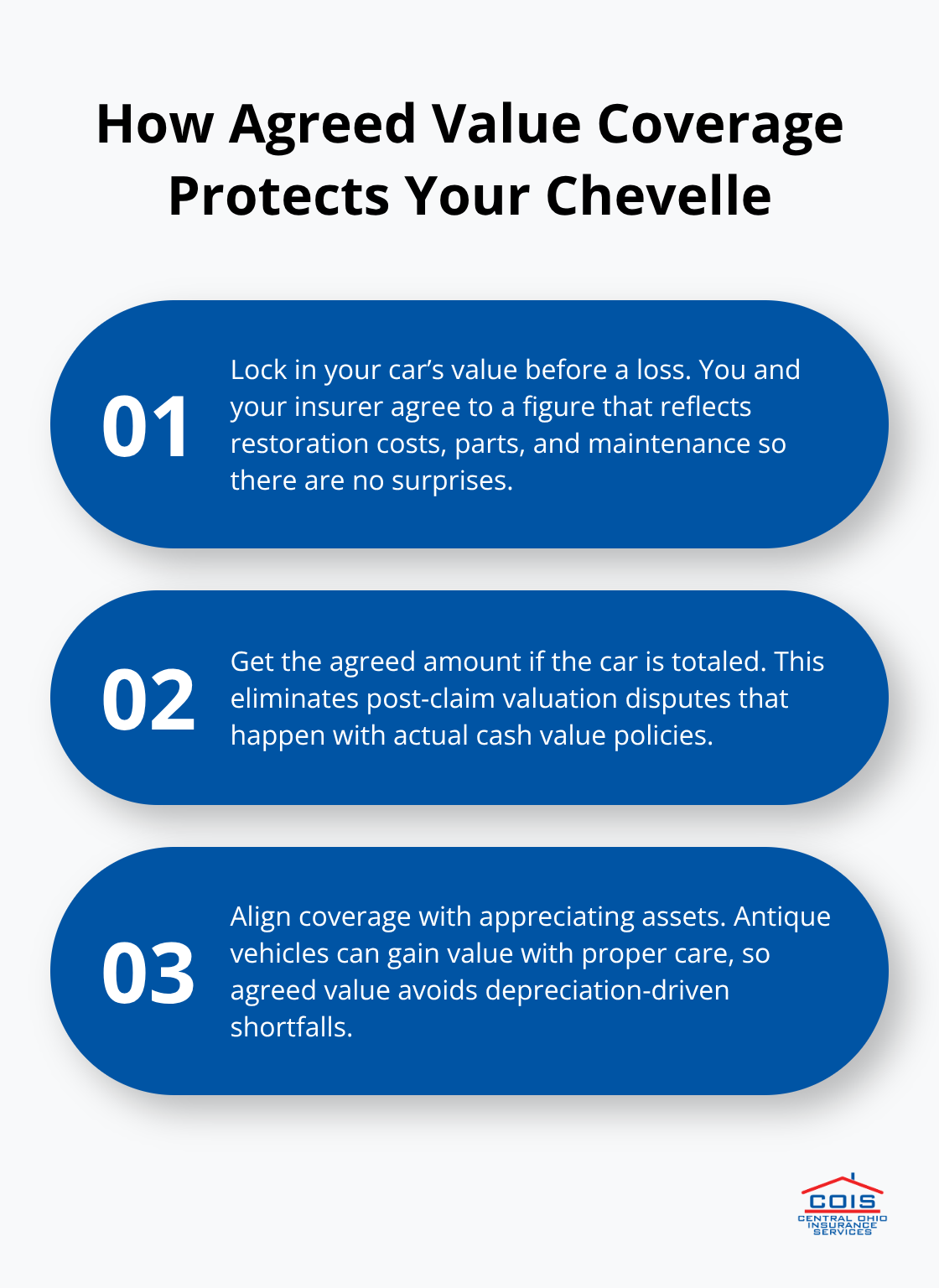

How Agreed Value Coverage Protects What You’ve Invested

Standard auto insurance uses actual cash value, which means the insurer calculates what your car is worth based on depreciation tables and market comparisons. For a 1967 Chevelle, that approach destroys your financial protection. Agreed value coverage works differently: you and your insurer decide upfront what your antique car is worth, and that’s the amount you receive if it’s totaled. American Collectors Insurance, rated 4.9 out of 5 stars by over 20,000 customers in Ohio, emphasizes that agreed value eliminates post-loss disputes about your vehicle’s value. You determine the valuation within reason, reflecting what you’ve actually invested in restoration, parts, and maintenance. If your Chevelle is worth $45,000 after a complete frame-off restoration, you agree to that figure when you purchase the policy. When a covered total loss occurs, you get that full $45,000 minus your deductible, not whatever the insurer thinks the car is worth at that moment. This approach matters because antique cars appreciate when maintained properly, yet standard valuations ignore that reality.

Premium costs for antique car insurance typically range from $200 to $600 annually according to industry data, reflecting the lower risk of limited mileage and specialized storage. Your agreement on value at policy inception means no depreciation arguments after an accident, theft, or weather damage.

Why Agreed Value Beats Actual Cash Value

Actual cash value policies calculate your payout based on what the market says your car is worth today. That number drops every year, even though your Chevelle’s value climbs with proper maintenance. Agreed value flips this dynamic: you lock in the protection amount before any loss happens. The insurer accepts your valuation (within reason) and commits to paying that amount if total loss occurs. This certainty lets you focus on your collection rather than fighting an insurance company about valuation after disaster strikes.

Protecting Rare Parts and Custom Modifications

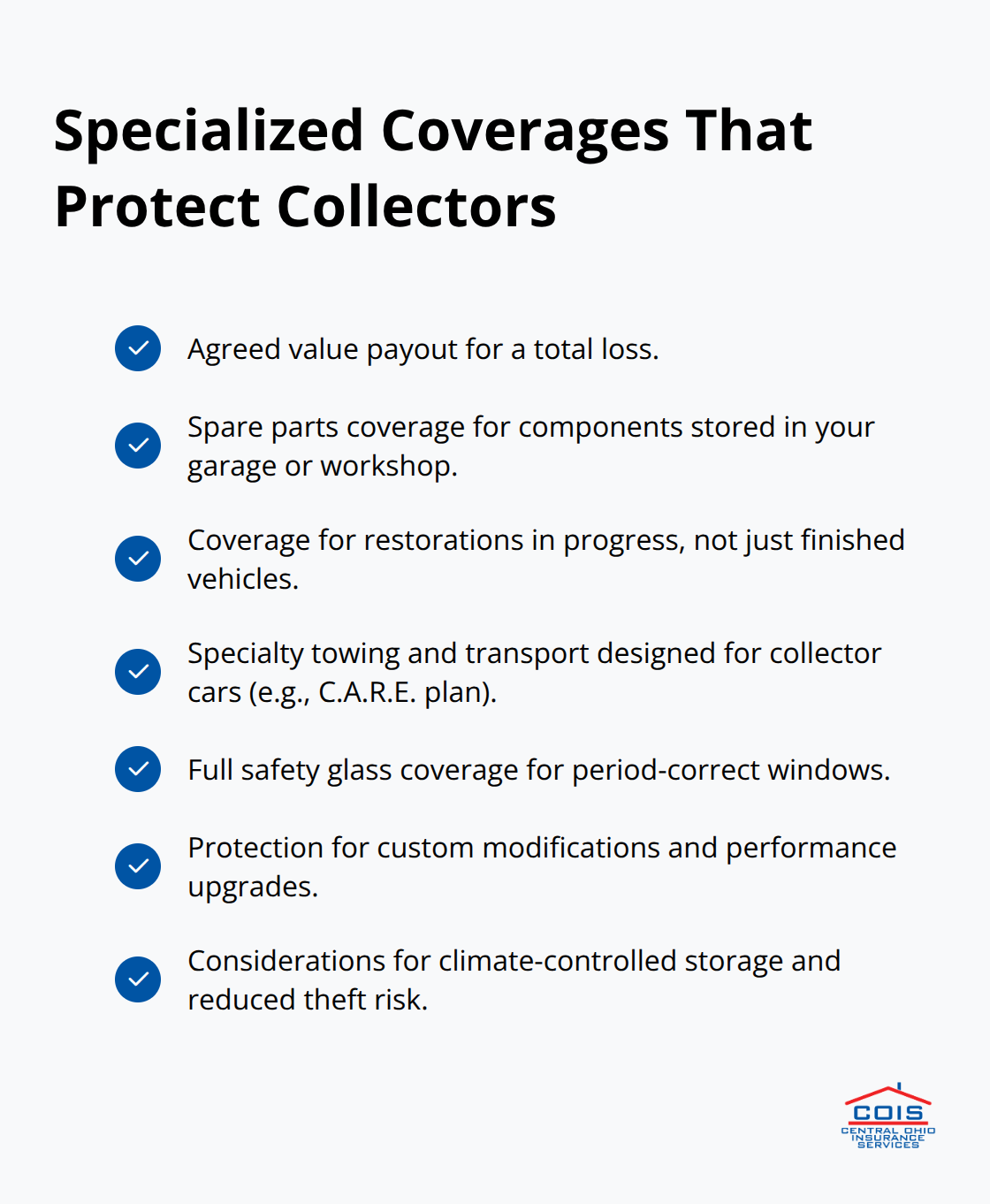

Your restoration project includes vintage components you’ve sourced over years, original parts you’re preserving, and specialized modifications that increase the car’s value. Standard auto insurance won’t cover these items because they exist outside the vehicle’s standard configuration. Antique car policies from carriers like American Modern include spare parts coverage, meaning those original components sitting in your garage or workshop receive protection. If you’re actively restoring your Chevelle, coverage remains in force throughout the restoration process, not just when the car is finished and drivable. This matters because many collectors keep vehicles under construction for months or years. Custom modifications that enhance value-whether mechanical upgrades, interior restoration work, or performance enhancements-need explicit coverage in your policy. Your agreed value should reflect these modifications since they’re part of what makes your car valuable.

Specialized Towing and Transportation Coverage

Roadside assistance for specialty vehicles differs from standard towing because your antique car needs specialized handling. Standard towers might use equipment that damages vintage paint or chrome. Policies through carriers like American Modern include the C.A.R.E. plan covering towing and transportation specifically for collector vehicles, ensuring your Chevelle reaches a shop equipped to handle it properly. Full safety glass coverage protects original or period-correct windows that cost significantly more than modern glass replacements. When you need help on the road, you want a tower who understands that your 1967 Chevelle isn’t a typical sedan-it’s a precision investment that demands careful transport.

Why Standard Carriers Misunderstand Collector Cars

Standard auto insurance policies treat your 1967 Chevelle the same way they treat a fleet of rental cars. Carriers using actual cash value models calculate payouts based on depreciation schedules that assume all vehicles lose value predictably. Your antique car appreciates when properly maintained, yet standard underwriting ignores this reality entirely. Most insurers lack underwriting specialists who understand collector vehicle economics. They apply commuter-focused risk models to cars driven 2,500 miles annually at car shows and weekend cruises. This mismatch creates three immediate problems: severe undervaluation of your investment, artificial restrictions on how you can use your vehicle, and coverage gaps that leave rare components unprotected.

Valuation Gaps That Cost You Thousands

Standard carriers don’t employ adjusters trained in vintage restoration costs or marketplace values for antique vehicles. When you file a claim, you negotiate with someone evaluating your Chevelle using the same process they’d use for a 2015 Honda Civic. The financial damage compounds quickly because the insurer’s valuation software doesn’t recognize the restoration work, rare parts, and specialized labor you’ve funded. Your Chevelle represents years of careful investment and meticulous maintenance, yet standard policies treat it as a depreciating asset. Collector cars do not follow predictable depreciation curves, and their value is often driven by provenance and market demand rather than book values. This approach works fine for everyday cars but destroys your financial protection for collector vehicles.

Usage Restrictions That Don’t Match Reality

Usage restrictions embedded in standard policies create friction for serious collectors. Many carriers impose annual mileage limits of 12,000 miles or higher, designed for drivers commuting to work five days weekly. Your collector car doesn’t fit this profile, yet you still pay rates calibrated for that usage pattern. Some standard policies explicitly restrict show car usage or prohibit towing other vehicles-restrictions that don’t match how collectors actually operate. If you participate in vintage car clubs, your driving patterns fall outside standard underwriting models. Carriers may deny claims if they discover you drove to a car show, claiming the vehicle was used outside policy parameters.

Coverage Gaps During Restoration and Storage

Standard policies won’t cover spare parts sitting in your workshop or garage, even though these original components represent significant financial value and irreplaceable inventory. Coverage for vehicles actively under construction simply doesn’t exist in standard auto policies-the moment you start a frame-off project, you lose protection. Specialty carriers like American Modern explicitly cover restorations in progress, acknowledging that collectors often keep vehicles under construction for extended periods. Your Chevelle might spend six months or two years as a restoration project before returning to show-ready condition. Standard insurance abandons you during that vulnerable period when the vehicle has no operational engine or transmission. Specialty insurers understand that collectors need protection throughout every stage of ownership-whether your car sits in climate-controlled storage, participates in shows, or undergoes active restoration work.

Final Thoughts

Your 1967 Chevelle deserves protection that reflects its actual value and how you genuinely use it. Standard auto insurance fails collectors because it applies depreciation models designed for everyday vehicles to cars that appreciate with proper maintenance. Agreed value coverage eliminates this fundamental mismatch by locking in your vehicle’s worth upfront, ensuring you receive full compensation for a total loss without post-claim valuation disputes.

Specialized carriers understand that your antique car sits in climate-controlled storage most of the year, participates in shows and weekend cruises, and requires rare parts sourced from specialized suppliers. This reality demands coverage that protects spare components, covers restorations in progress, and includes towing services equipped to handle vintage vehicles safely. Standard carriers treat your Chevelle like a depreciating asset and restrict how you drive it, while specialized policies recognize that collectors invest years and significant money into preservation.

At Central Ohio Insurance Services, Inc., we work with carriers that specialize in collector vehicles and understand what makes your collection valuable. Our team shops multiple carriers to find Pickerington antique car insurance tailored to your specific vehicles, usage patterns, and restoration projects. Contact us to discuss how specialized coverage protects your investment and gives you the peace of mind that standard policies simply cannot provide.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.