Your collectible car sits in the garage as a genuine investment, not just transportation. Standard auto insurance treats it like any other vehicle-and that’s the problem.

At Central Ohio Insurance Services, Inc., we know that collectible car insurance in Columbus works differently because your vehicle deserves different protection. Let’s show you why specialized coverage matters.

Why Standard Auto Insurance Doesn’t Protect Collectible Cars

Standard auto insurance uses actual cash value, which means the insurer pays what your car is worth on the open market minus depreciation. For a 1967 Chevrolet Corvette or a restored 1955 Thunderbird, that calculation fails completely. These vehicles appreciate over time rather than depreciate, yet a standard policy treats them like a five-year-old sedan losing value every year. If your collectible car is totaled, you receive far less than you invested, leaving you with a significant financial loss on an asset you maintained and restored carefully.

The Actual Cash Value Problem

Standard auto insurance companies apply depreciation tables to your vehicle, regardless of its rarity or condition. According to data from the collector car market, classic vehicles driven fewer than 5,000 miles annually hold or increase in value when properly maintained. Yet standard policies ignore this reality entirely. If you own a well-restored muscle car worth $45,000, a standard insurer calculates its actual cash value at $28,000 after applying depreciation factors. In a total loss, that represents a $17,000 gap between what you should receive and what you actually get. Agreed value coverage locks in your car’s true worth from day one, eliminating this depreciation trap.

Mileage and Usage Don’t Match Collector Lifestyles

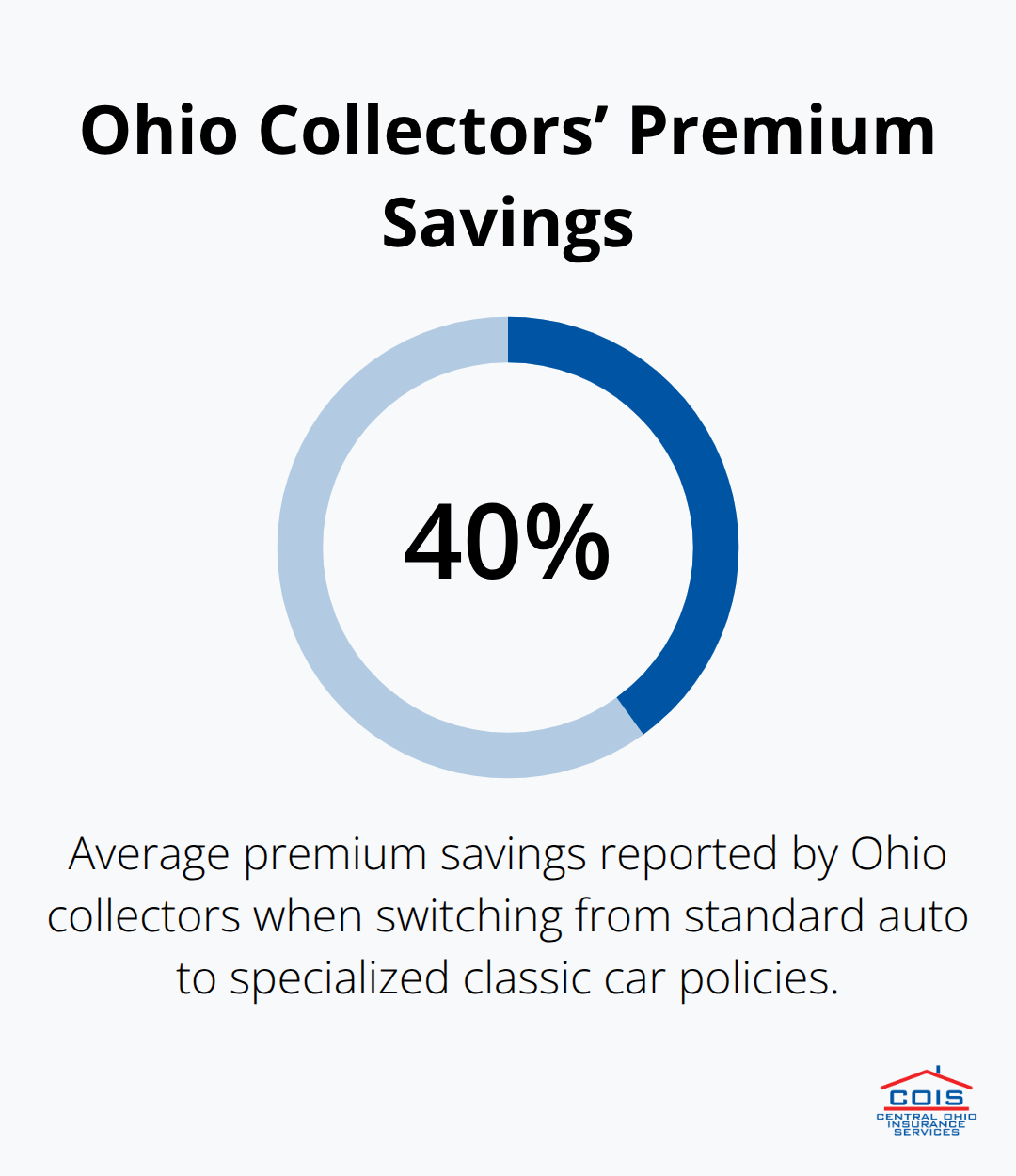

Standard auto policies expect you to drive daily. Most collectible car owners drive their vehicles far less-typically 2,000 to 5,000 miles per year for shows, rallies, and occasional pleasure driving. A standard policy often includes broad mileage allowances but applies rates designed for regular commuters. You pay for coverage that assumes daily use when your vehicle spends most of its time garaged. Specialized collectible car insurance recognizes this limited usage pattern and prices accordingly. In Ohio, collectors report saving approximately 40 percent on premiums when switching from standard auto insurance to policies designed specifically for classic vehicles. That savings reflects the actual risk profile of a carefully stored, infrequently driven investment.

High-Value and Rare Vehicles Need Specialized Attention

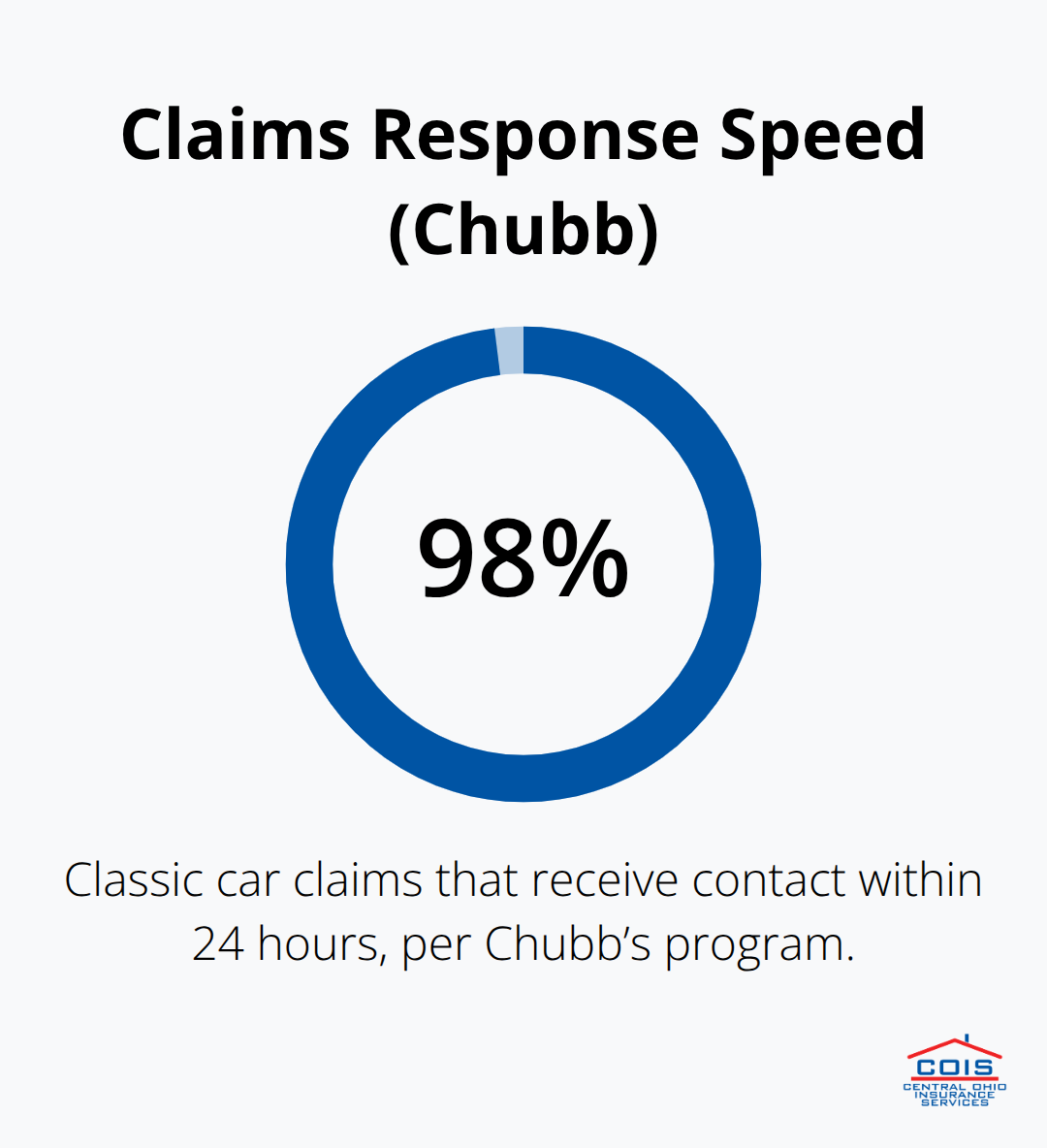

Standard insurance also fails to account for custom parts, restoration work, and originality. If your classic car includes authentic reproduction parts, a period-correct restoration, or rare original components, a standard policy won’t recognize that added value. In a claim, standard insurers often push for aftermarket replacements rather than authentic parts that preserve your vehicle’s integrity and market value. Specialized collectible car coverage prioritizes OEM and authentic parts, protecting both your investment and the vehicle’s historical significance. Chubb’s classic car insurance program guarantees that 98 percent of claims receive contact within 24 hours and emphasizes quality repairs using original or fabricated parts when originals aren’t available-a stark contrast to the one-size-fits-all approach of standard auto policies.

What Specialized Coverage Offers Instead

Agreed value coverage replaces the depreciation model entirely. You and your insurer establish your vehicle’s value upfront, based on its condition, rarity, and market position. When a total loss occurs, you receive that agreed amount minus your deductible-no depreciation calculations, no surprises. This approach protects vehicles that appreciate or hold value, making it the standard for serious collectors. Additionally, specialized policies recognize that your car spends time at shows, exhibitions, and rallies rather than commuting. Coverage extends to these events without requiring pre-authorization for non-competitive activities. The combination of agreed value protection and event coverage transforms how your investment is insured, addressing the gaps that standard policies leave wide open.

What Your Collectible Car Policy Actually Covers

Agreed Value Protection That Matches Your Investment

Agreed value coverage forms the foundation of proper collectible car protection, and it works fundamentally differently than standard insurance. You and your insurer agree on your vehicle’s worth before any loss occurs, based on its condition, rarity, market comparables, and restoration quality. That agreed amount becomes your payout in a total loss, minus only your deductible and any salvage value you retain. Chubb’s classic car program pays the full agreed value without depreciation adjustments-a critical distinction from stated value policies that may reduce payouts based on wear and tear. This means your investment receives fair compensation if disaster strikes.

Custom Parts and Restoration Work Stay Protected

Custom parts and restoration work receive explicit coverage under collectible car policies in ways standard insurance simply cannot match. If your classic truck includes a period-correct engine rebuild, custom upholstery, or authentic reproduction trim pieces, those enhancements factor into your agreed value and remain covered. When repairs become necessary, specialized policies prioritize OEM parts or high-quality fabricated originals rather than pushing cheap aftermarket replacements that damage authenticity and resale value. Chubb guarantees payment for fabricated parts when originals aren’t available, preserving your vehicle’s integrity and historical significance.

Event Coverage Without Pre-Authorization Hassles

Event coverage extends protection to car shows, rallies, auctions, and exhibitions without requiring pre-authorization for non-competitive activities. Your classic car remains fully covered whether it sits in your garage or travels to a weekend show. This flexibility matters because serious collectors participate in multiple events throughout the year, and standard policies either restrict this activity or charge extra for it. Specialized collectible car insurance treats event attendance as normal use rather than an exception requiring approval.

Roadside Assistance for Valuable Vehicles

Roadside assistance options add practical value too, covering flatbed towing, fuel delivery, battery service, and lockouts. Your collectible reaches a qualified repair facility rather than being hauled by a standard tow truck that might damage your investment. This protection proves especially valuable for older vehicles that may not start reliably or for cars being transported to distant shows and auctions. The combination of agreed value, parts protection, event coverage, and roadside support creates a comprehensive safety net that standard policies cannot provide.

As you evaluate which policy fits your collection, the next step involves understanding how to select the right coverage limits and compare options across multiple carriers-decisions that directly impact both your protection and your premium.

Selecting the Right Coverage for Your Collectible

Document Your Vehicle’s True Market Value

Determining what your collectible car actually costs to replace separates collectors who receive fair compensation from those who face devastating shortfalls. Start by documenting your vehicle’s current market value using multiple sources: auction results from Hemmings Motor News, comparable sales from Bring a Trailer, and professional appraisals from specialists familiar with your specific make and model. A 1965 Ford Mustang fastback might sell for $35,000 in base condition but $65,000 with matching numbers and original paint, yet a generic appraisal misses these distinctions entirely.

Photograph every restoration detail, original component, and custom work completed on your vehicle. Gather receipts for parts, labor, and materials spent over the years. This documentation becomes your foundation for negotiating agreed value with insurers and proves invaluable if you file a claim. Many collectors underestimate their vehicle’s worth by 20 to 30 percent, which means they also underinsure it. Chubb’s approach includes automatic coverage for new classic purchases for the first 90 days while you conduct a formal appraisal, giving you breathing room to get the valuation right without gaps in protection.

Compare Multiple Carriers and Their Specific Terms

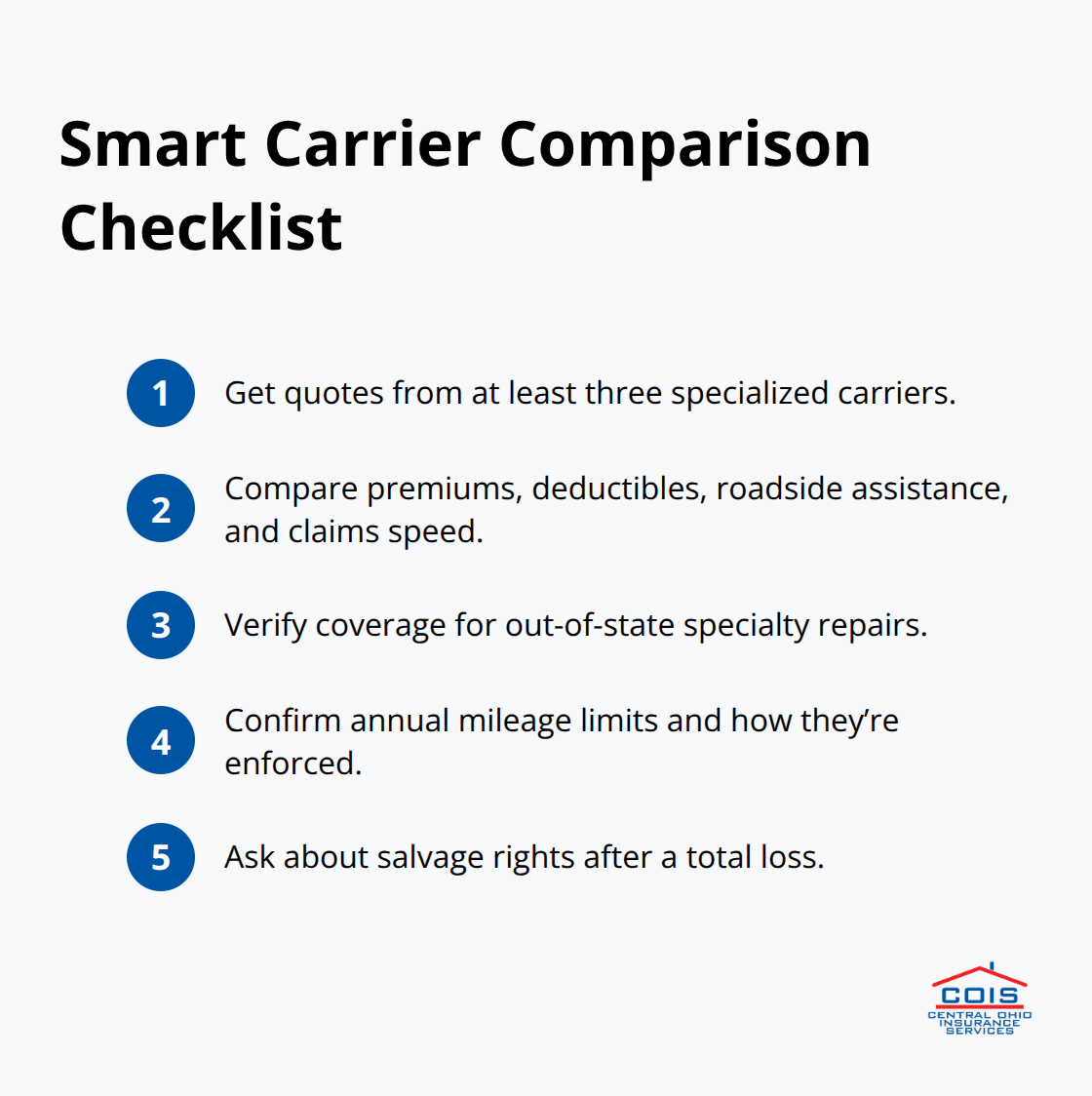

Comparing carriers matters far more than accepting the first quote you receive. Different insurers define classic vehicles differently, offer varying mileage allowances, and price based on different risk models. One carrier might require vehicles to be at least 25 years old while another accepts 20-year-old vehicles. Some impose annual mileage limits of 5,000 miles while others allow up to 7,500 without penalty.

Request quotes from at least three specialized carriers and compare not just premiums but deductible options, roadside assistance coverage, and claims handling speed. Chubb reports that 98 percent of claims receive contact within 24 hours, which matters when your investment sits damaged and vulnerable.

Ask whether the insurer covers out-of-state repairs if your vehicle needs specialized work unavailable locally. Ask specifically whether you retain salvage rights if a total loss occurs, since keeping damaged parts and components can offset your out-of-pocket costs.

Work with Agents Who Understand Collector Vehicles

An agent who understands collector vehicles proves essential because they recognize that your 1970 Chevelle with a 454 engine isn’t comparable to a standard 1970 Chevelle in terms of value or risk profile. A knowledgeable agent shops multiple carriers to find policies aligned with your actual usage and vehicle specifications rather than forcing you into one-size-fits-all options. At Central Ohio Insurance Services, Inc., our licensed team shops multiple carriers to deliver unbiased, competitively priced solutions with fast quotes and clear guidance on which coverage options match your collection’s specific needs.

Final Thoughts

Your collectible car represents years of investment, careful restoration, and genuine passion for automotive history. Standard auto insurance cannot protect that commitment because it was never designed for vehicles that appreciate rather than depreciate. Specialized collectible car insurance in Columbus addresses this gap directly by recognizing your vehicle’s true value and the limited, purposeful way you drive it.

Agreed value coverage eliminates the depreciation trap that leaves standard policyholders thousands of dollars short after a total loss, while event coverage lets you attend shows and rallies without worrying about gaps in protection. Parts coverage preserves authenticity by prioritizing OEM and fabricated originals over cheap aftermarket replacements, and roadside assistance gets your investment to qualified repair facilities rather than standard shops that may not understand vintage vehicles. These protections work together to create a safety net that actually matches how collectors use and value their cars.

Different insurers define classic vehicles differently, impose varying mileage limits, and price based on distinct risk models, which means shopping multiple carriers reveals significant differences and uncovers savings that single-quote approaches miss entirely. In Ohio, collectors switching from standard auto insurance to specialized coverage report saving approximately 40 percent on premiums-a difference that compounds year after year. Contact Central Ohio Insurance Services, Inc. to get a quote for your collectible vehicle today and discover how specialized coverage protects your investment.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.