Homeowners in Columbus often think affordable home insurance means settling for weak coverage. That’s simply not true.

At Central Ohio Insurance Services, Inc., we’ve helped hundreds of local families find policies that protect their homes without draining their budgets. This guide shows you exactly how to do it.

Finding Affordable Home Insurance in Columbus

Compare Quotes Across Multiple Carriers

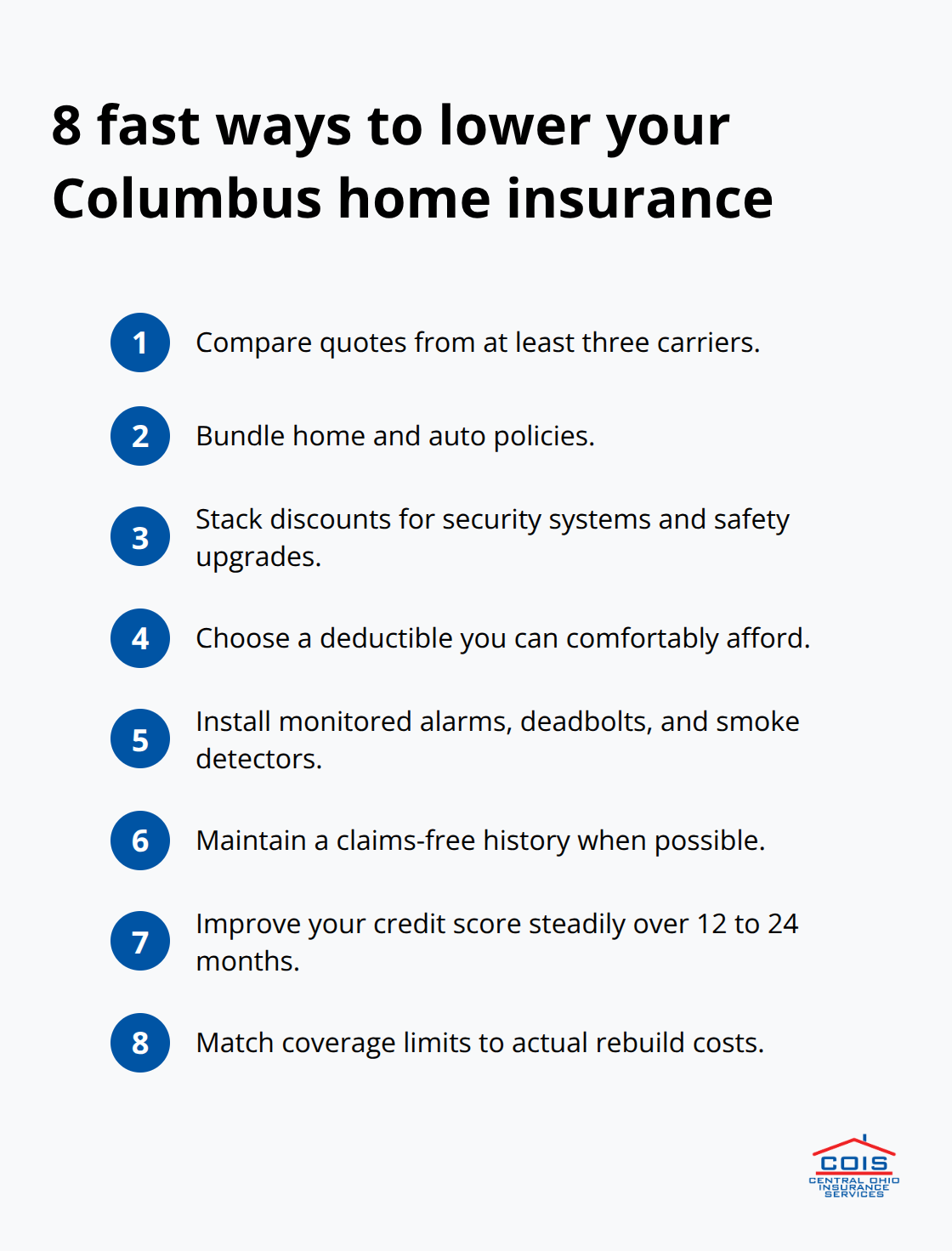

Shopping around is the single most effective way to cut your Columbus home insurance costs. Request quotes from at least three carriers to see where you actually land. Most Columbus residents stop after one quote and overpay for years. Request quotes from Cincinnati Insurance, Erie, Farmers, and Travelers to see where you actually land. Each quote takes 15 minutes online, and the savings compound over time.

Bundle Home and Auto Policies for Immediate Savings

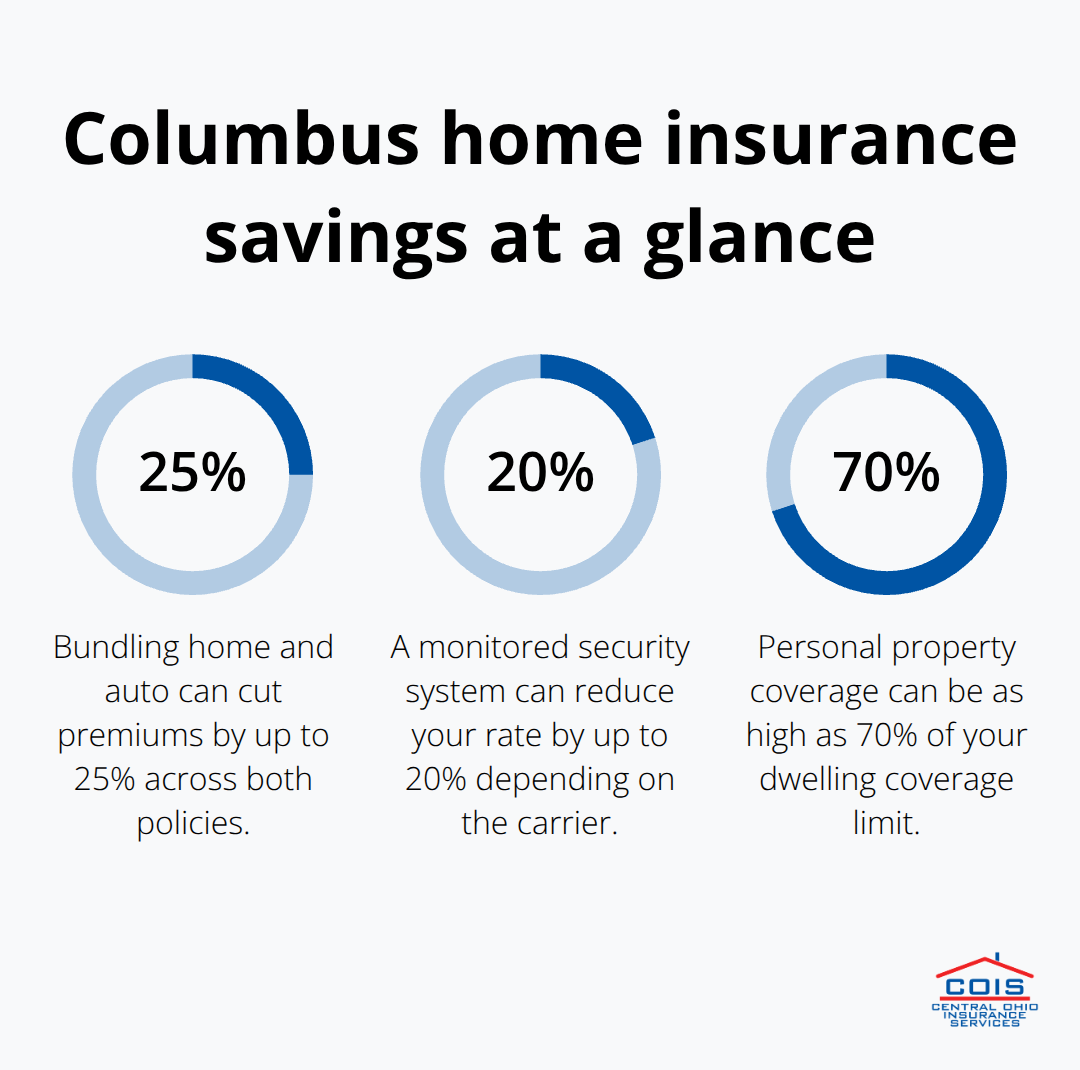

Bundling your home and auto policies cuts premiums by roughly 15% to 25% across both policies. A Columbus homeowner paying $1,100 for home insurance and $900 for auto saves $300 to $400 annually just from combining them. It’s worth checking multiple carriers even if you’ve been with another carrier for years.

Stack Discounts to Maximize Savings

Beyond bundling, request discounts for security systems (5% to 20% off), new roofs, deadbolt locks, and claims-free history. These add up fast. A monitored security system plus a claims-free discount can knock $150 to $300 off your annual premium. Most insurers offer these credits without requiring you to ask, but you must mention them when you request your quote.

Match Coverage Limits to Rebuild Costs

Coverage limits matter as much as the insurer you choose. Most Columbus homes need replacement-cost coverage between $250,000 and $400,000 depending on neighborhood and construction costs. Work backward from what it would actually cost to rebuild your home, not what it’s worth on the market. Underinsurance is costly-you’ll pay out-of-pocket for losses beyond your limit. Overinsurance wastes money on coverage you’ll never use.

As you narrow down your carrier options and lock in your coverage limits, the next step involves understanding what actually happens when you file a claim and how different deductible choices affect your monthly payments. Compare Columbus homeowners insurance quotes from top providers to discover real savings strategies that reduce your annual premiums.

How to Slash Your Columbus Home Insurance Costs

Raise Your Deductible to Cut Premiums Fast

Increasing your deductible from $500 to $2,000 cuts your annual Columbus premium by roughly $348, dropping you from about $1,812 to $1,464 according to rate data. You agree to absorb more of the loss yourself, and insurers reward that trade-off significantly. The key is selecting a deductible you can actually pay out-of-pocket without financial strain. If you keep $2,500 in emergency savings, a $2,000 deductible makes sense. If your emergency fund sits at $800, stick with $1,000. This isn’t theory-it’s about matching your financial reality to your policy structure.

Install Security Features and Safety Upgrades

A monitored security system drops your rate by 5% to 20% depending on the carrier, and that discount stacks with others. Deadbolt locks, smoke detectors, and a newer roof each qualify for separate credits. A Columbus homeowner with a monitored system, deadbolts, and a claims-free history can knock $200 to $300 off the annual premium without touching coverage limits. Install the system before you request quotes so the discount applies immediately.

Improve your credit score for substantial savings

Your credit score carries outsized weight in Columbus home insurance pricing. Improving your credit score typically takes 12 to 24 months of on-time payments and lower credit utilization. The effort pays off fast once your score climbs-each 50-point jump can lower your premium by $200 to $400.

If your credit is poor, don’t skip shopping. Ohio Mutual tends to offer more competitive rates for lower credit scores than many national carriers, so comparison quotes remain essential. As you lock in these cost-reduction strategies, understanding what your policy actually covers becomes equally important to protecting your investment.

What Your Columbus Home Insurance Actually Covers

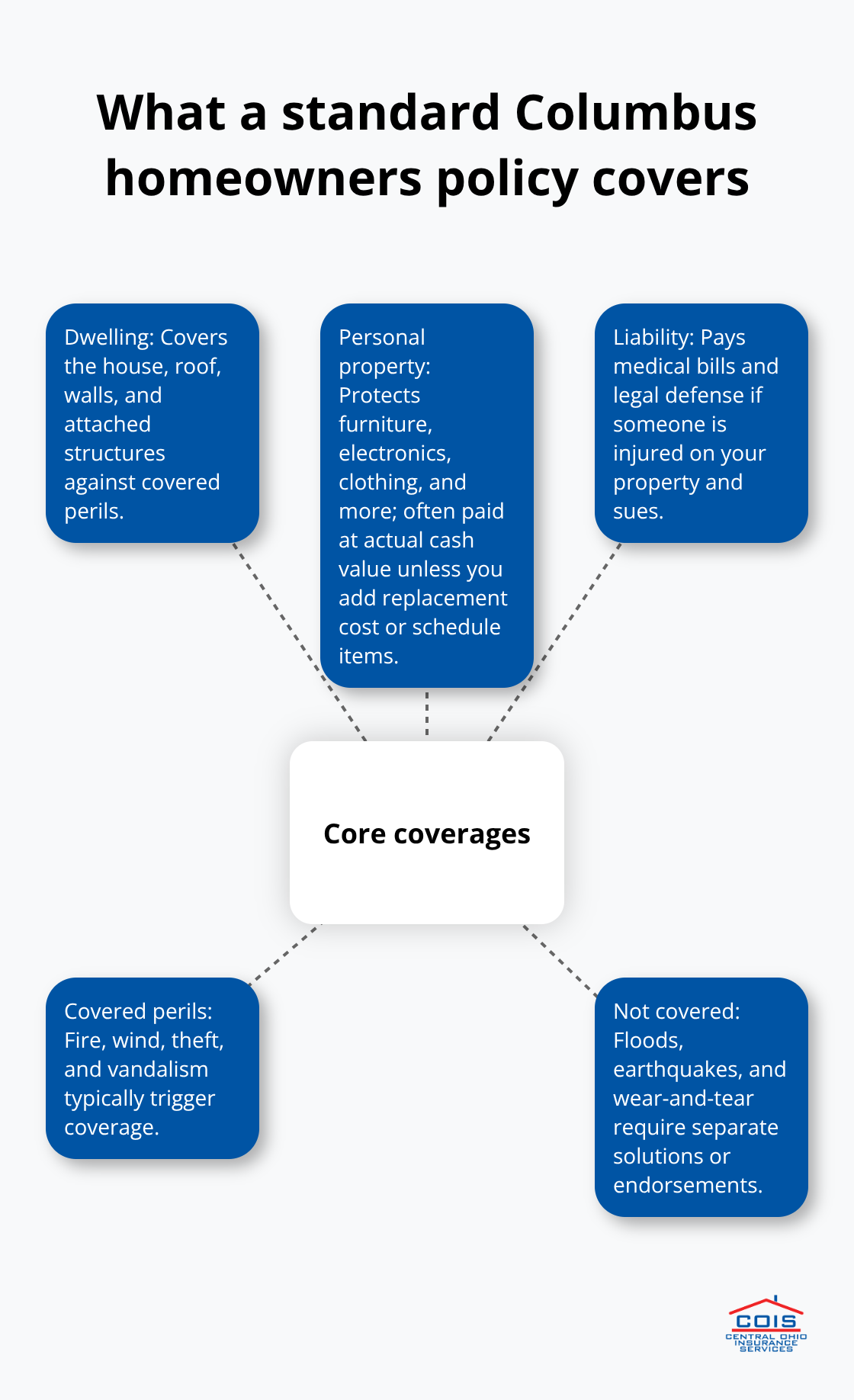

A standard homeowners policy in Columbus covers three core areas: your dwelling structure, your personal belongings inside it, and your liability if someone gets hurt on your property. Most Columbus homeowners understand the dwelling part-that’s the house itself, the roof, walls, and attached structures. What trips people up is understanding exactly what triggers coverage and what doesn’t. Your policy covers damage from fire, wind, theft, and vandalism. It does not cover floods, earthquakes, or wear-and-tear from age.

That distinction matters enormously when you decide whether you actually have adequate protection for your Columbus home.

Your Dwelling Coverage Must Match Rebuild Costs, Not Market Value

This is where most Columbus homeowners make their first mistake. They insure their home based on what it would sell for, not what it would cost to rebuild. A home worth $350,000 on the market might cost $425,000 to rebuild because construction labor and materials in Columbus run higher than the average home’s resale value. According to MoneyGeek data, a 2,000-square-foot frame home in Columbus with standard coverage typically costs about $2,027 annually. That assumes a $250,000 dwelling limit, but your actual rebuild cost determines whether that limit is enough. Work with a contractor or use online rebuild calculators to get a realistic number, then select your dwelling coverage to match it. Underinsurance leaves you paying thousands out-of-pocket after a total loss. Overinsurance wastes premium dollars on coverage you’ll never need.

Personal Property Coverage Protects What’s Inside Your Home

Your personal property coverage limit typically runs 50% to 70% of your dwelling coverage. If your dwelling limit is $300,000, your belongings are usually covered up to $150,000 to $210,000. This covers furniture, electronics, clothing, and other items you own. The catch is that most policies pay actual cash value, not replacement cost, meaning older items get depreciated. A five-year-old television worth $400 on the market might pay out $200 in actual cash value if it burns in a fire. If you own high-value items-jewelry, art, collectibles, or expensive electronics-request scheduled personal property coverage. This endorsement lists specific items with agreed-upon values, and the insurer pays replacement cost without depreciation. In Columbus, adding scheduled personal property runs $75 to $150 annually depending on item values, but it protects what matters most to you.

Liability Coverage Protects Your Financial Future If Someone Is Injured

Liability coverage pays for medical bills and legal defense if someone gets hurt on your property and sues you. Standard Columbus policies typically offer $100,000 to $300,000 in liability coverage. If a neighbor’s child falls on your icy driveway in January and breaks their arm, your liability coverage pays their medical bills and any settlement. Most Columbus homeowners underestimate how quickly medical costs and legal fees escalate. A serious injury can easily exceed $300,000 in damages. Try reviewing your liability limit alongside your home value and net worth. If you have significant assets, consider an umbrella policy that adds $1,000,000 in additional liability coverage for $150 to $300 annually. That extra layer protects your savings and future income if a lawsuit goes beyond your homeowners policy limit.

Final Thoughts

Finding affordable home insurance in Columbus requires three concrete actions: comparing quotes across multiple carriers, stacking discounts strategically, and matching your coverage limits to actual rebuild costs rather than market value. We at Central Ohio Insurance Services, Inc. watch Columbus homeowners leave hundreds of dollars on the table each year simply by not shopping around or understanding what their policies actually cover. The strategies in this guide work because they address the real drivers of your premium-raising your deductible from $500 to $2,000 saves roughly $348 annually, bundling home and auto cuts costs by 15% to 25%, and installing a monitored security system qualifies for 5% to 20% off.

Affordability without adequate coverage defeats the purpose entirely. A $1,000 annual premium means nothing if you’re underinsured and face a $50,000 out-of-pocket loss after a fire. Your dwelling coverage must match what it actually costs to rebuild your home, not what it would sell for on the market. Your liability limit should reflect your assets and net worth, and your personal property coverage should protect the items that matter most through scheduled coverage for high-value belongings.

Contact a licensed agent who can shop multiple carriers on your behalf, present quotes side-by-side, and explain exactly what each policy covers. We at Central Ohio Insurance Services, Inc. handle this process for Columbus homeowners every day-our team compares rates from top carriers, identifies discounts you qualify for, and ensures your coverage aligns with your actual needs and budget. Reach out to Central Ohio Insurance Services, Inc. today for a fast, no-obligation quote and discover how much you can save on affordable home insurance in Columbus.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.