Your classic car is more than transportation-it’s an investment that deserves protection. Classic car insurance discounts can significantly reduce what you pay while keeping your collector’s vehicle properly covered.

At Central Ohio Insurance Services, Inc., we help classic car owners find the coverage and savings that match their needs. Let’s look at the discounts available and strategies to maximize your savings.

What Makes Classic Car Insurance Different

Agreed Value Coverage Protects Your Investment

Classic car insurance operates in a completely different universe than standard auto coverage, and the difference matters far more than most owners realize. Standard auto policies are built around depreciation-your car loses value every year, and your coverage amount shrinks accordingly. Classic and collector vehicles move in the opposite direction. A 1967 Chevrolet Corvette or a restored 1955 Ford Thunderbird often appreciates in value, sometimes significantly.

Agreed value coverage transforms everything. Instead of paying out depreciated cash value after a total loss, agreed value policies pay the exact amount you and the insurer established at the policy start. If you and your carrier agree your 1972 Oldsmobile 442 is worth $35,000, that’s what you receive if it’s totaled or stolen, no arguments about market fluctuations or condition disputes.

Why Standard Policies Fail Collectors

Standard insurers price policies based on the assumption that you drive your car daily, rack up miles, and expose it to typical roadway risks. Classic car policies recognize reality: your collector vehicle sits in a climate-controlled garage most of the year, comes out for car shows and club meetings, and accumulates perhaps 2,500 to 5,000 miles annually.

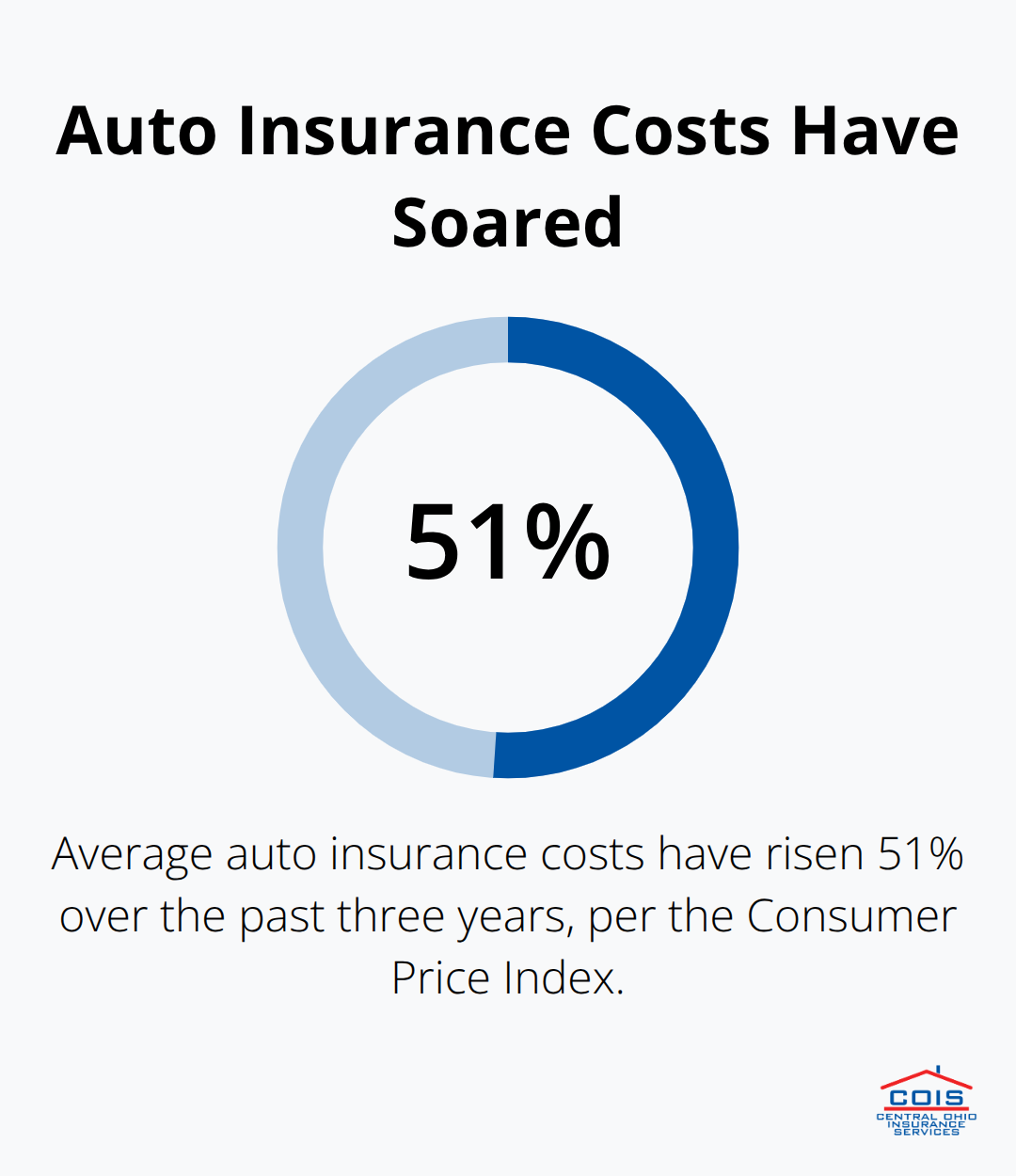

The Consumer Price Index reported that average auto insurance costs have risen 51% over the past three years, yet collectors face an unfair burden. Standard carriers refuse to acknowledge that reduced mileage and garage storage should dramatically lower premiums. This inequity makes specialized classic car insurance not just preferable-it’s essential for protecting your investment at a fair price.

Repair Flexibility and Lower Deductibles

The practical difference extends to how repairs get handled and what coverage options become available. Classic car insurers typically allow you to choose your repair shop, meaning you can work with a specialist who understands restoration work and original parts rather than being forced to a random body shop. You can often add spare parts coverage to protect valuable replacement components during restoration projects.

Deductibles run lower than standard policies-many carriers offer $250 or $500 options instead of the $1,000 minimums common on modern vehicles. This lower deductible structure reflects the reduced risk profile of collector vehicles and makes claims more manageable when they occur.

Streamlined Eligibility and Underwriting

Eligibility requirements are straightforward: your vehicle typically must be 25 model years or older, stored in a fully enclosed locked garage, and used primarily for exhibitions, club activities, and pleasure driving rather than daily commuting. Some carriers accept unique or limited-production vehicles regardless of age, including replicas.

The underwriting process reflects this specialization too. Many classic car policies don’t require an on-policy appraisal to establish value-you document your car’s worth through recent sales data, professional appraisals, and condition photos. This streamlined approach gets you covered faster and more affordably than the lengthy evaluation process standard insurers impose.

Finding the Right Coverage for Your Collector Vehicle

Multiple carriers now specialize in collector vehicles, each with different strengths and pricing structures. The next section explores the specific discounts these carriers offer and how you can stack them to maximize your savings on premiums.

Where Classic Car Owners Find Real Savings

Stack Multiple Policies for Substantial Discounts

Bundling your classic car policy with homeowners, umbrella, or life insurance typically cuts 15 to 25 percent off your total premiums across all policies. This isn’t theoretical-carriers like American Collectors Insurance and OpenRoad explicitly market multi-policy discounts as a primary savings mechanism. The math works because bundling reduces administrative overhead and increases customer lifetime value. If you insure your home, primary vehicle, and collector car with the same carrier, you receive meaningful reductions on each line. Request quotes that include your full coverage portfolio rather than asking only about the classic car policy in isolation. Many owners miss this entirely and shop policies individually, leaving hundreds of dollars annually on the table.

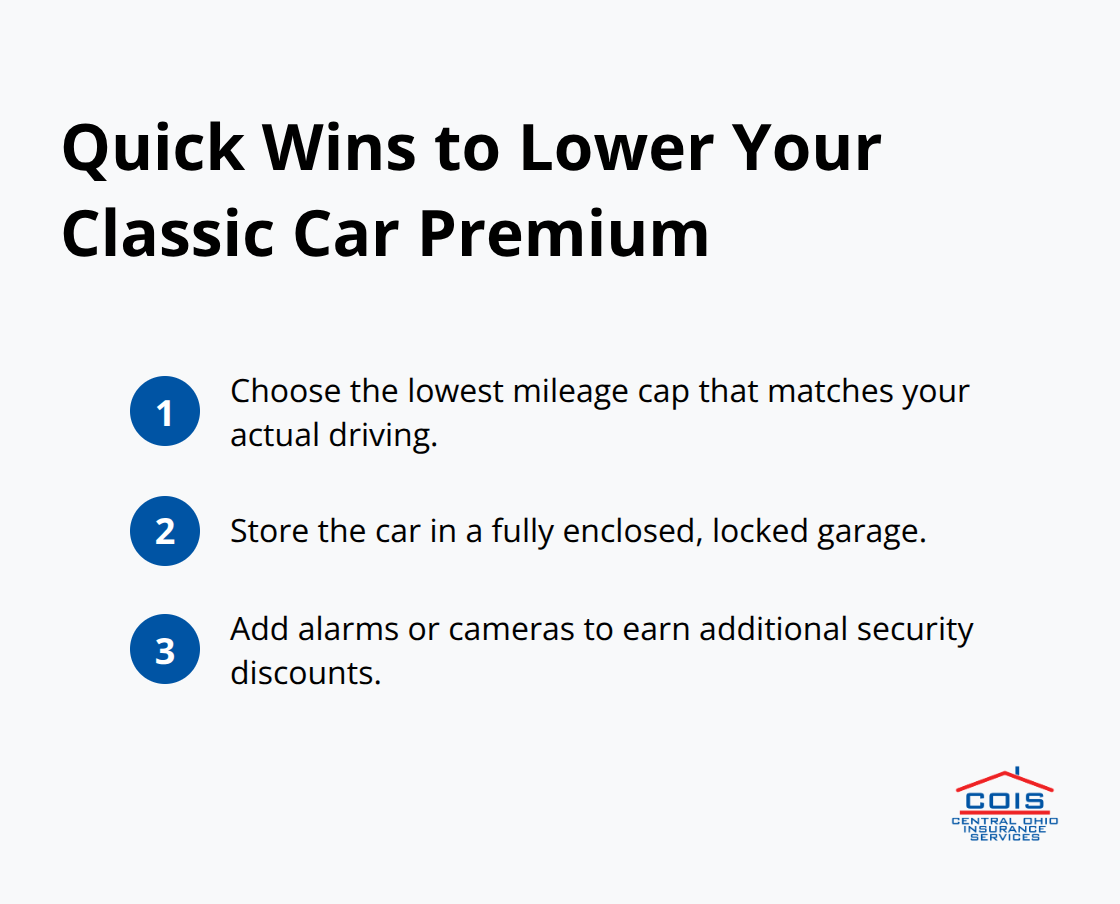

Optimize Mileage Caps and Storage Requirements

Low mileage caps and secure garage storage form the foundation of classic car insurance pricing, and understanding how to optimize both dramatically affects your rate. Most carriers cap annual mileage between 2,500 and 7,500 miles, with lower caps producing lower premiums. An honest assessment of your actual driving matters here-if you genuinely drive your 1969 Dodge Charger only 3,000 miles yearly for car shows and club events, select a 3,500-mile policy instead of accepting a 7,500-mile cap. You pay for coverage you won’t use otherwise.

Storage requirements demand a fully enclosed, locked garage, but adding security features like alarms or surveillance cameras unlocks additional discounts from most carriers. Some insurers offer 5 to 10 percent reductions for documented security upgrades.

Leverage Club Memberships and Driving Records

Car club memberships produce measurable savings. Many specialized carriers partner with established clubs and offer 5 to 15 percent discounts to members who verify their affiliation. Organizations like local Corvette clubs, Mustang clubs, or broader collector networks often have negotiated rates with multiple insurers. Verify your club’s partnerships before joining or renewing membership.

A clean driving record matters significantly too-traffic violations or at-fault accidents raise premiums substantially or create eligibility barriers entirely. The collector insurance market explicitly recognizes that serious enthusiasts maintain better driving habits than average motorists, so underwriters reward clean records with competitive pricing.

Compare Total Coverage, Not Just Advertised Percentages

When you evaluate quotes, compare total annual premiums and actual coverage details rather than focusing on advertised savings percentages, which can obscure what you’re truly getting for your money. This comparison approach reveals which carriers actually deliver the best value for your specific vehicle and driving situation. The next section walks through how to document your vehicle’s value and condition-the foundation that determines whether you receive fair compensation if a claim occurs.

How to Build a Strong Case for Fair Coverage

Professional Appraisals Establish Accurate Value

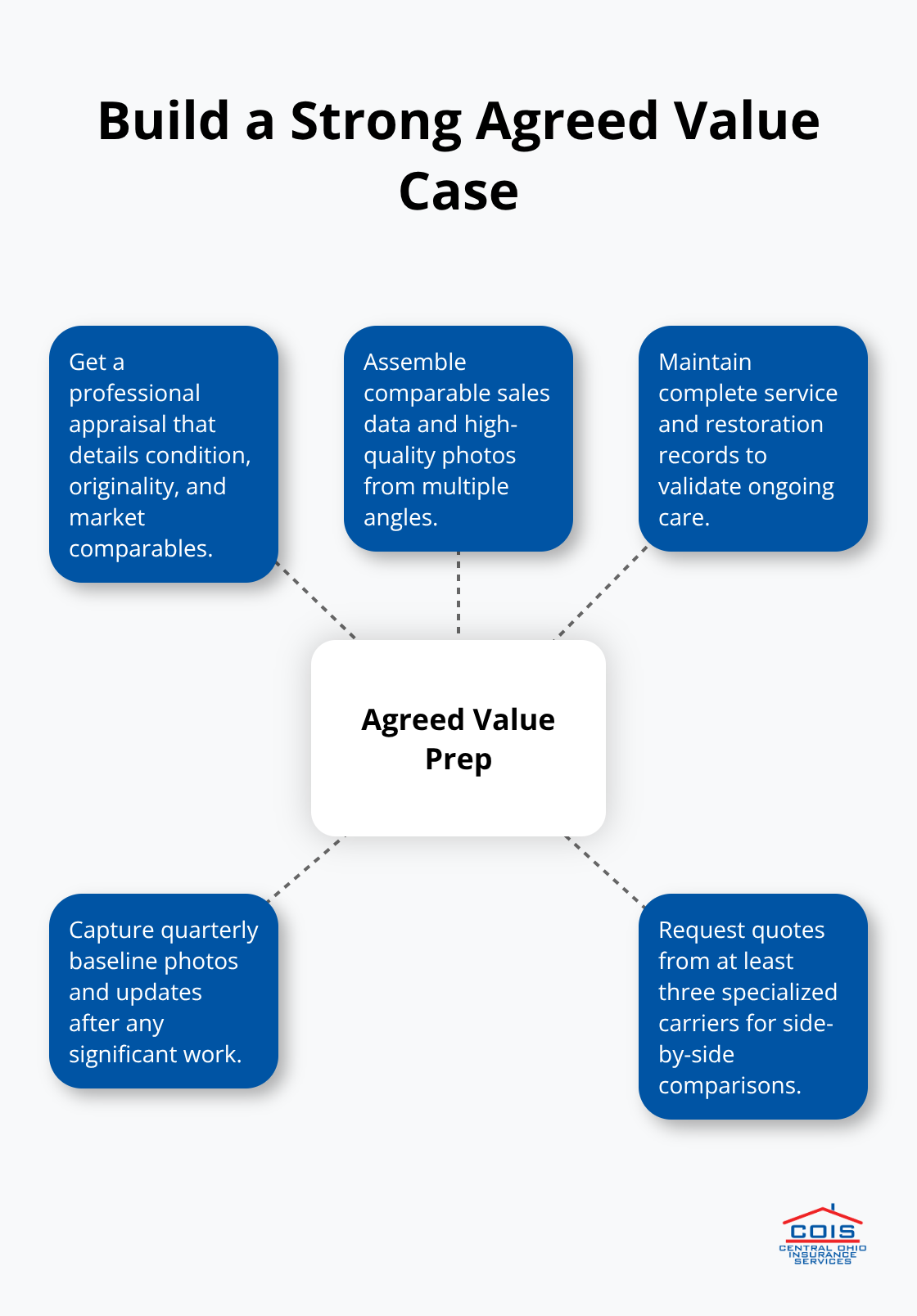

Professional appraisals form the foundation of accurate agreed value coverage, and skipping this step costs collectors thousands in undercompensation. A qualified appraiser documents your vehicle’s condition, restoration quality, original components versus reproductions, and market comparables specific to your make and model. This appraisal becomes your insurance policy’s baseline-if your 1961 Jaguar XK-E is totaled, the carrier pays based on the appraised value you established together.

Many collectors attempt to estimate value themselves using online pricing guides, but these tools lack the granular detail that distinguishes a mediocre restoration from a show-quality example. Detailed documentation prevents claim disputes.

Gather Evidence to Support Your Vehicle’s Worth

Collect recent sales data for comparable vehicles, professional photographs showing condition from multiple angles, service records demonstrating maintenance and restoration work, and any documentation of original features or rare components. Present this evidence when negotiating your agreed value with the carrier.

Undervaluing your vehicle upfront to reduce premiums creates catastrophic risk-you receive only what you agreed to, regardless of actual market value at claim time. The documentation you assemble protects your investment far more than any premium savings ever could.

Maintain Detailed Records and Visual Documentation

Maintenance discipline directly impacts your ability to maintain fair coverage and defend claims when they occur. A comprehensive maintenance log documents every service, parts replacement, and restoration work and demonstrates to carriers that you treat the vehicle as a serious asset rather than a hobby project.

Photograph your vehicle quarterly in consistent lighting to establish baseline condition, then photograph again after any significant work. This visual record prevents disputes about pre-existing damage if a claim arises.

Compare Multiple Carriers on Total Value

Request quotes from at least three specialized providers to compare the total annual premium including all discounts you qualify for, the agreed value each carrier proposes, deductible options available, and coverage details like spare parts or roadside assistance.

Price alone misleads because a carrier offering lower annual premiums might impose a higher deductible or exclude coverage elements you need. Shop multiple carriers simultaneously and present clear side-by-side analysis, helping you understand exactly what each policy covers and costs before committing.

Final Thoughts

Classic car insurance discounts work best when you approach them strategically rather than chasing the lowest advertised rate. The real savings come from understanding how agreed value coverage protects your investment, stacking multiple discounts across bundled policies, and documenting your vehicle’s condition thoroughly. A carrier offering 20 percent off means nothing if the agreed value they propose undervalues your 1972 Oldsmobile 442 by thousands of dollars.

Your next step is straightforward: gather your vehicle documentation, identify which discounts apply to your situation, and request quotes from at least three specialized carriers. Compare the total annual premium, the agreed value each proposes, and the specific coverage details rather than focusing on percentage savings alone. This comparison reveals which carrier actually delivers the best protection for your collector vehicle at a fair price.

Contact Central Ohio Insurance Services, Inc. to discuss your classic car insurance needs and discover how much you can save with the right coverage strategy. Our licensed team shops multiple carriers to find unbiased, competitively priced solutions tailored to your specific vehicle and driving habits. We handle the comparison work for you and provide hands-on support throughout the policy and claims process.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.