Your collector car collection represents years of passion and investment. Protecting it requires understanding the different collector car insurance choices available to you.

At Central Ohio Insurance Services, Inc., we know that standard auto policies fall short for classic and specialty vehicles. The right coverage depends on your collection’s value, how you drive, and what protection gaps matter most to you.

Which Payout Method Protects Your Collection Best

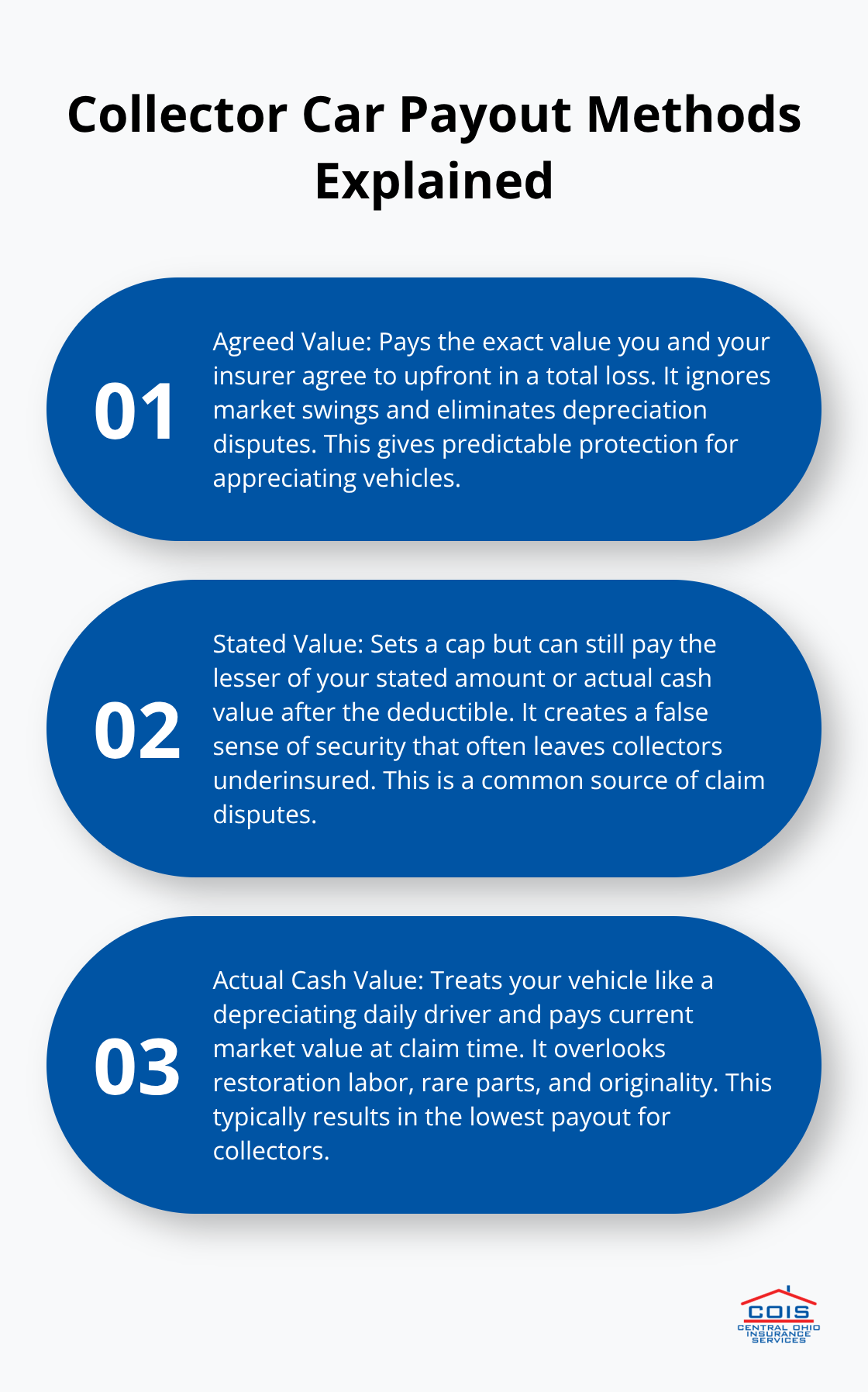

Agreed Value: The Only Real Protection

Agreed value policies stand out as the clear winner for collector car owners, and the numbers prove it. When you and your insurer agree on your vehicle’s value upfront, you receive that exact amount in a total loss claim, regardless of market fluctuations. This matters because collector cars often appreciate or hold their value in ways standard vehicles never do.

These policies eliminate depreciation and post-loss valuation disputes, meaning you avoid the depreciation trap that destroys coverage on regular vehicles. If your 1965 Mustang is worth $45,000 today, that’s what you’ll receive if it’s totaled-not some depreciated figure calculated months later. This certainty eliminates the risk of underinsurance and gives you peace of mind about protecting your investment.

Building Your Agreed Value

You should document your vehicle’s condition, modifications, and provenance to justify the agreed value. Use reputable valuation tools or professional appraisals to establish accurate figures, then update them as your collection appreciates or as you complete restorations. Clear documentation of enhancements helps justify a higher agreed value beyond baseline market price.

Why Stated Value Fails Collectors

Stated value policies create a false sense of security and should be avoided. These policies set a payout cap, but the actual claim payout can be limited to the lesser of your stated amount or actual cash value after the deductible-a bait-and-switch that leaves collectors underinsured. The difference between agreed value and stated value has cost collectors thousands in claim disputes.

Actual Cash Value: A Collector’s Nightmare

Actual cash value policies are worse still, treating your collector car like a depreciating family sedan and paying out only what the vehicle would fetch on the open market at claim time, not what it’s actually worth to you. This approach ignores the years of restoration work, rare parts sourcing, and careful preservation that define your collection.

If you’re serious about protecting your collection’s true worth, agreed value is the only choice that makes sense for vehicles you’ve invested in restoring, maintaining, and preserving. Understanding these payout methods sets the stage for evaluating other critical coverage features that protect specific aspects of your collection.

What Should Shape Your Collector Car Insurance Decision

Vehicle Value and Rarity Set Your Coverage Baseline

Your collection’s combined value and rarity determine both your premium and the coverage limits you need. A $15,000 classic truck requires different protection than a $150,000 exotic import, and insurers price policies accordingly based on agreed value amounts you establish together. Document each vehicle’s current market value using professional appraisals or reputable valuation tools-Hagerty’s valuation platform and NADA Guides provide concrete numbers that justify your agreed value figure. Higher-value vehicles and rare models often benefit from carriers specializing in collector cars, since general insurers frequently undervalue customizations and originality that drive collector car prices upward.

Mileage Patterns Determine Your Policy Fit

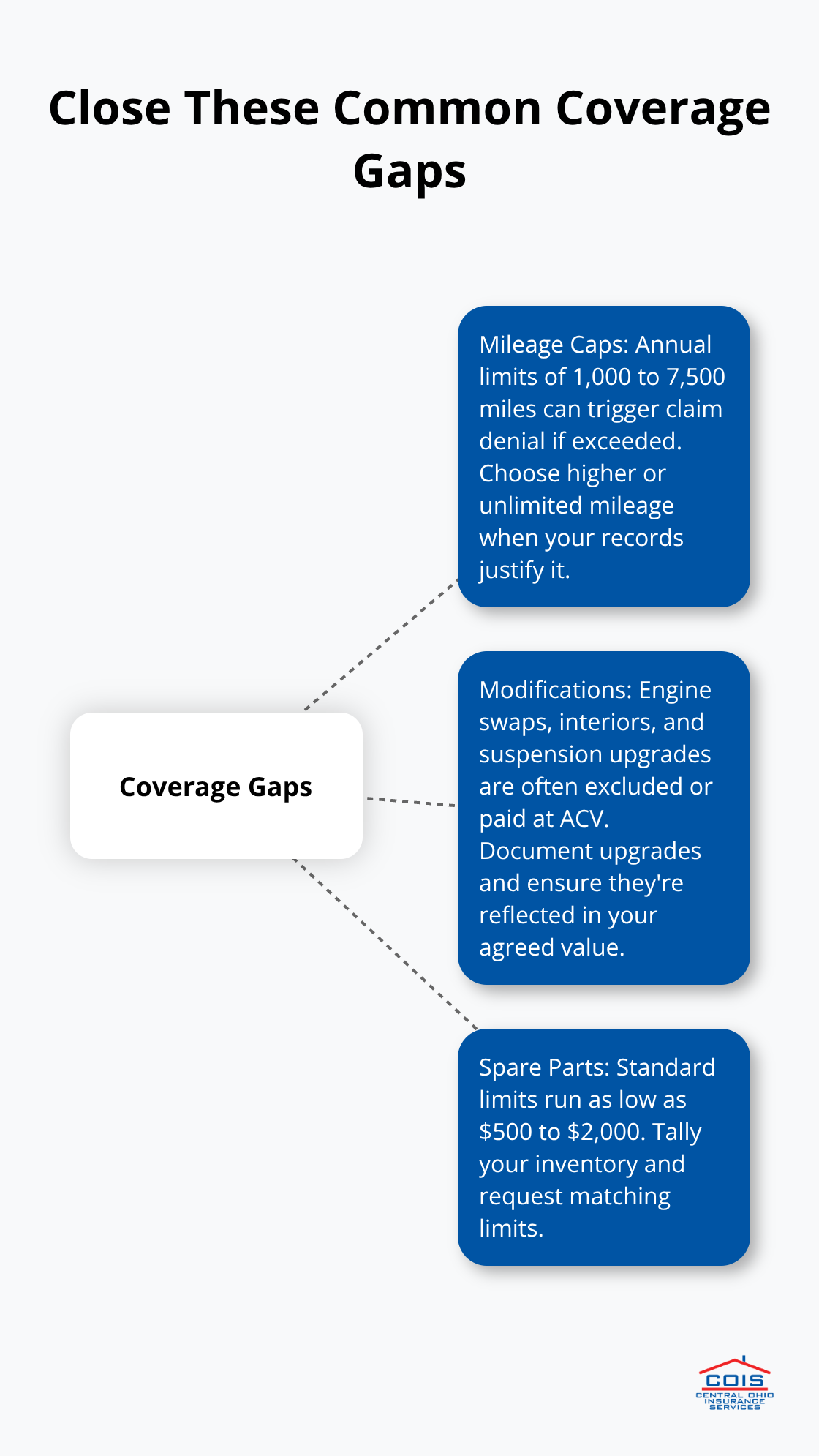

Your actual mileage patterns matter far more than casual collectors realize. Most collector car policies cap annual mileage between 1,000 and 7,500 miles yearly, though some carriers like Grundy and Chubb offer unlimited mileage options that cost more but eliminate restrictions. If you drive your collection to car shows, club events, and weekend pleasure trips regularly, you’ll exceed typical limits quickly-track your miles honestly before selecting a policy. The difference between a 5,000-mile cap and unlimited coverage can mean the difference between a claim denial and full protection when you need it most.

Storage Conditions and Security Lower Your Costs

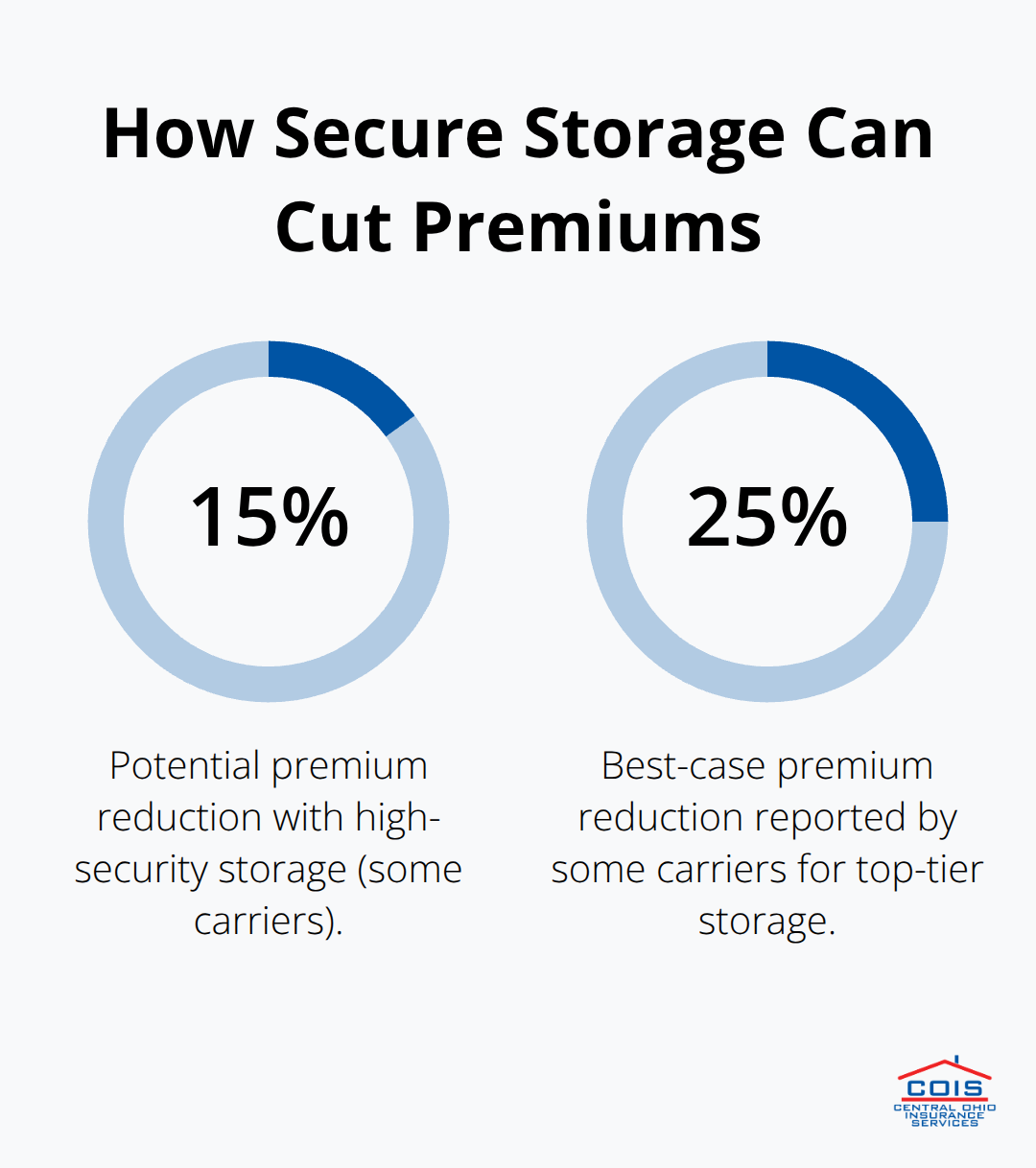

Storage conditions directly affect your rates and coverage availability since vehicles kept in locked garages cost significantly less to insure than those stored outdoors. High-security storage with alarm systems, climate control, and limited access reduces theft and weather damage risk, lowering premiums by as much as 15-25% with some carriers. Your facility’s protection level influences which insurers will even quote your collection and at what price point.

Driving History and Age Affect Your Eligibility

Your driving history and age also factor in; drivers under 25 face coverage denials or surcharges from most specialist carriers, while multiple violations or accidents can disqualify you entirely from agreed value policies. Clean records and mature drivers unlock better rates and broader coverage options across the market. These personal factors interact with your vehicle characteristics to shape which policies you can actually obtain.

With these decision factors mapped out, the next step involves understanding what coverage gaps exist in standard collector car policies and how to fill them with the right add-ons and endorsements.

Common Gaps in Collector Car Coverage

Mileage Caps Create Real Claim Risks

Most standard collector car policies cap annual mileage between 1,000 and 7,500 miles yearly, though some carriers like Grundy and Chubb offer unlimited mileage options that cost more but eliminate restrictions. This sounds reasonable until you actually drive your collection to regional car shows, club meets, and weekend cruises. Exceed your annual limit by even 500 miles and you risk claim denial entirely, not partial coverage reduction. Track your actual mileage over a full year before selecting a policy-most collectors significantly underestimate their miles once they start attending shows and events regularly, so request unlimited or higher mileage caps if your records show consistent driving.

Modifications and Customizations Face Exclusions

Modifications and customizations often face outright exclusions despite being the very reason your vehicle commands premium prices. A hot rod with a modern engine swap, custom interior, and specialty suspension may have those enhancements completely excluded from coverage or covered only at actual cash value rates that devastate their real worth. Obtain a professional appraisal that specifically documents all modifications, custom work, and upgrades with photographs and receipts, then ensure your agreed value reflects these enhancements explicitly in your policy language. Carriers like American Collectors Insurance and Hagerty acknowledge restorations more transparently than generalist insurers, so inform your insurance company about any car modifications to avoid coverage gaps or claim denials.

Spare Parts Coverage Leaves Collectors Exposed

Spare parts and accessories stored for your vehicles typically receive minimal coverage, capping reimbursement at $500 to $2,000 depending on your carrier. If you’ve invested in NOS parts, hard-to-find original components, or specialized tools for restoration work, that coverage evaporates quickly. Calculate your spare parts inventory and request coverage matching that total-American Modern offers $2,000 spare parts coverage compared to American Collectors at $500, a difference that matters if you’ve accumulated genuine original components. This action transforms vague policy language into specific protection that actually covers what you’ve built and preserved.

Final Thoughts

Agreed value coverage protects your collection far better than stated value or actual cash value policies because it guarantees you receive the exact amount you and your insurer agreed upon upfront. Stated value policies create false security by potentially paying less than your stated amount, while actual cash value treats your collector car like a standard vehicle that loses value over time. The payout method you select determines whether your collection receives real protection or leaves you financially exposed when a total loss occurs.

Matching collector car insurance choices to your specific collection requires honest assessment of your vehicles’ combined value and rarity, your actual annual mileage patterns, and your storage conditions. Document your vehicles’ current values using professional appraisals, track your mileage over several months to establish realistic patterns, and evaluate your storage facility’s security features. Then request coverage limits and mileage allowances matching those realities, not what you hope your driving will be.

Address the three coverage gaps that commonly derail collector car claims: mileage restrictions that exceed your actual driving, modifications and customizations that receive inadequate coverage or outright exclusions, and spare parts inventory that falls short of your accumulated components. Request unlimited or higher mileage caps if your records show consistent driving, obtain professional appraisals documenting all modifications with photographs and receipts, and calculate your spare parts value to request matching coverage limits. Contact Central Ohio Insurance Services, Inc. to discuss your collection’s protection needs and receive a personalized quote that matches your vehicles’ true value and how you actually drive them.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation. Artificial intelligence may have been used to generate text and images in some blog articles and may contain inacuracies.